Inflation tracker – July 2024, contrasting trends

In the United States, consumer price inflation is slowing, in line with the cooling of the labour market. After three months of more restrained growth, the CPI index fell in June, month-on-month, for the first time in two years. The core index rose very moderately (+0.1% m/m, the smallest increase since May 2020). Other important signs of disinflation: alternative measures continue to fall, and in particular the trimmed mean PCE index published by the Federal Reserve in Dallas, which is now well anchored below 3% (see page 7). The rebound in producer prices, which is still limited at this stage, is nonetheless worth watching and could limit the fall in consumer price inflation. Year-on-year, producer prices rose back above 2% in the second quarter (2.7% y/y in June).

In the Eurozone, significant inflation divergences are once again emerging between member countries. This is mainly due to very unfavourable base effects on energy for some countries, especially Belgium which, with headline and energy inflation at 5.4% and 25.6% respectively in June, is seeing the biggest rise in prices. By contrast, inflation is still below 1% in Finland (0.5%) and Italy (0.9%). At 2.5%, inflation in Germany and France is on a par with the Eurozone average, which has fallen slightly (-0.1 p.p.) compared with May. Household inflation expectations continue to decline, but as in the UK, they remain above the current level of inflation, contrary to forecasters' expectations, which are lower.

In the UK, inflation remained stable at 2% in June. Deflation in energy prices is still very significant, and is expected to continue for several months yet, due to the further decline in the price cap level for gas and electricity price in July. Core inflation remains driven by services (5.7%). After a slight deceleration the previous month, rent prices rose by 7.2² y/y, the largest increase since October 1993. Moreover, although household inflation expectations have been falling steadily for over a year, the decline is more limited than headline inflation.

In Japan, the rise in wages is not, for the time being, altering the dynamics of inflation, which is struggling to strengthen in the services sector. It is true that inflation in this sector rebounded by 0.3 percentage points to 1.8% y/y in June, but it has fallen back compared with the start of the year, dragging down core inflation (excluding fresh food and energy), which halved between August 2023 (4.3% y/y) and June 2024 (2.1%). That said, the measure most closely followed by the Bank of Japan, the CPI excluding fresh food, rose from 2.6% in May to 2.7% in June. Although it only represents 7.8% of the price index, energy inflation contributed 0.6 points to total inflation in June and was once again gaining ground, against the backdrop of the recent withdrawal of government subsidies.

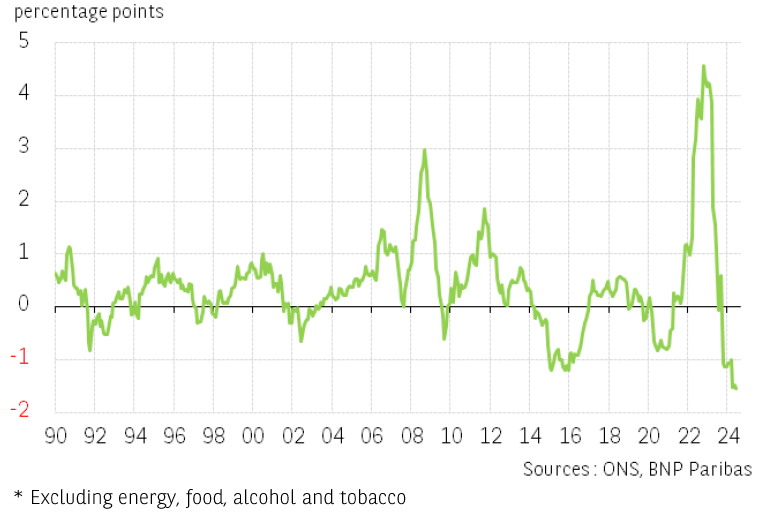

Chart of the month: Inflationary momentum still unsatisfactory in the UK

Headline inflation in the UK continued to fall very slightly in June, from 1.99% to 1.98%. While headline inflation is now lower in the UK than in the Eurozone and the US, core inflation remains higher, at 3.5% in June. The gap between the headline and core measures, which had widened sharply in previous years with the surge in energy prices, has since narrowed considerably. It even became more and more negative as the months went by, reaching a level in June that was unprecedented in almost 35 years, and which should become even more pronounced in July due to the further decline in the cap level for gas and electricity prices. The sharp fall in inflation is still confined to a small number of CPI components. Less than a third of the components of the consumer price index are up by 2% y/y or less, and conversely, more than a third are above 6% y/y, including medical devices and equipment (+6.4% y/y), cultural and recreational services (+6.5% y/y) and insurance contracts (+9.5% y/y). Will the current momentum be enough for the Bank of England (BoE) to cut the Bank Rate for the first time in August? That remains our scenario. However, the continuing strong growth in services prices and wages makes the BoE's position still very uncomfortable and could ultimately lead it to delay the start of the monetary easing cycle.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.