Inflation is hard to tame in eastern and Southern Africa

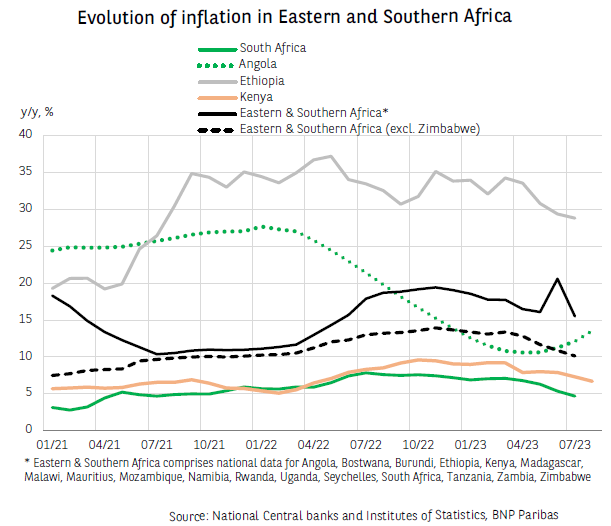

In recent months, the African continent has been hit hard by inflationary pressures. In Eastern and Southern Africa, inflation peaked at 19.4% yearon- year in November 2022. It has since begun a slow and difficult deceleration: in July 2023, regional inflation fell to 15.5%, after peaking again at 20.6% in June. Nevertheless, this average masks major national disparities.

In South Africa, inflation slowed to 4.7% in July. Since June, it has been meeting the 3-6% target set by the Central Bank (SARB), which was able to maintain its key rate at 8.25% at the end of July. This is the first pause after 10 consecutive rate hikes since November 2021. The SARB has lowered its average inflation forecast for 2023 to 6%. However, upside risks remain due to the increased intensity of rolling blackouts in August and rising fuel prices.

In Kenya, inflation has also been meeting the target set by the Central Bank (2.5-7.5%) since July, with the Monetary Policy Committee having raised the key rate by 100 basis points to 10.5% in June. Despite the new Finance Bill, which has notably increased VAT from 8% to 16% on petroleum products since July, the Central Bank of Kenya believes that inflationary pressures will continue to ease over the coming months. This prompted a pause in the monetary tightening cycle at the beginning of August.

In Ethiopia, since the armistice ending the armed conflict in Tigray in November 2022, inflation has begun a slow decline, falling back below the 30% threshold since June. The Central Bank of Ethiopia recently announced a series of measures aimed at bringing inflation down to 20% within a year. These include capping annual growth in bank loans and reducing government borrowing capacity.

Inflation in Angola has followed a reverse trend. The rise in oil prices at the start of 2022 allowed the Kwanza to appreciate considerably and helped to reduce inflation. However, since June 2023, the rapid depreciation of the Kwanza and the partial abolition of petrol subsidies have once again fuelled inflationary pressures. After reaching a seven-year low in April, inflation rose again, reaching 13.5% in August.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.