Inflation expectations are crashing, so what? It doesn't matter

There more inflation expectations nonsense from the New York Fed and economists yet again. Let's review.

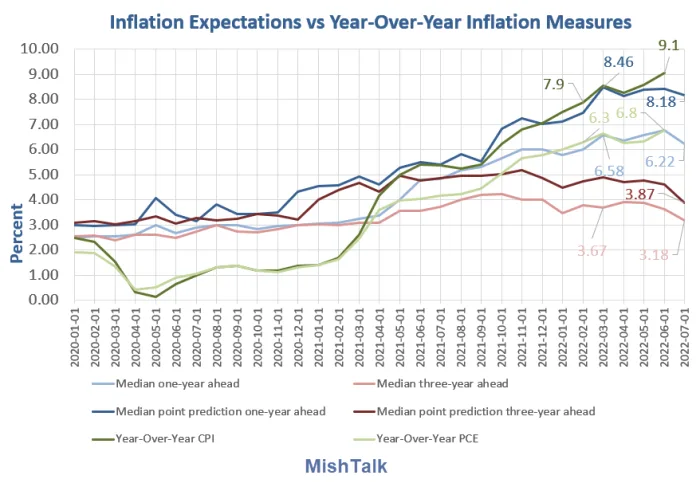

New York Fed consumer expectations survey

Please consider the New York Fed's Consumer Expectations Survey.

Median one- and three-year-ahead inflation expectations both declined sharply in July, from 6.8 percent and 3.6 percent in June to 6.2 percent and 3.2 percent, respectively. Both decreases were broad-based across income groups, but largest among respondents with annual household incomes under $50,000 and respondents with no more than a high school education. Median five-year ahead inflation expectations, which have been elicited in the monthly SCE core survey on an ad-hoc basis since the beginning of this year, also declined to 2.3 percent from 2.8 percent in June. Expectations about year-ahead price increases for gas and food fell sharply. Home price growth expectations and year-ahead spending growth expectations continued to pull back from recent series highs. Households’ income growth expectations improved.

For starters bragging about a decline to 6.22% on median one-year look ahead projections isn't much to be bragging about.

Even three years from now 3.88% and 3.18% are well above the Fed's target. The direction simply reflects falling gasoline prices right now.

So what? Inflation expectations are nonsense

Inflation expectations are a ridiculous concept. Two independent Fed research papers accurately make that conclusion.

Please consider Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) by the Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board.

The paper also blasted belief in the Phillips Curve. Here are a few direct quotes. The last bullet point is the most important one.

- The direct evidence for an expected inflation channel was never very strong.

- It is an irony of history that, when Phelps and Friedman sought to justify their proposed theoretical specifications, they were faced with the uncomfortable fact that empirical Phillips curves appeared to be remarkably stable.

- These techniques are similar in spirit to those employed in the 1990s to estimate new-Keynesian models; hence, they suffer from the same sorts of problems—discussed below—that attend empirical estimates of those models.

- Friedman’s derivation of the expectations-augmented Phillips curve implies that the real product wage should be strongly countercyclical (recall that in this model firms are always assumed to be on their labor demand curves). In particular, Friedman states as a matter of fact that “. . . selling prices of products typically respond to an unanticipated rise in demand faster than prices of factors of production,” which would in turn imply the empirical prediction that the price Phillips curve is steeper than the wage Phillips curve. However, in U.S. data this prediction is completely at odds with the evidence.

- Most standard tests of the new-Keynesian Phillips curve suffer from such severe potential misspecification issues or such profound weak identification problems as to provide no evidence one way or the other regarding the importance of expectations (much the same statement applies to empirical tests that use survey measures of expected inflation).

- What little we know about firms’ price-setting behavior suggests that many tend to respond to cost increases only when they actually show up and are visible to their customers, rather than in a preemptive fashion.

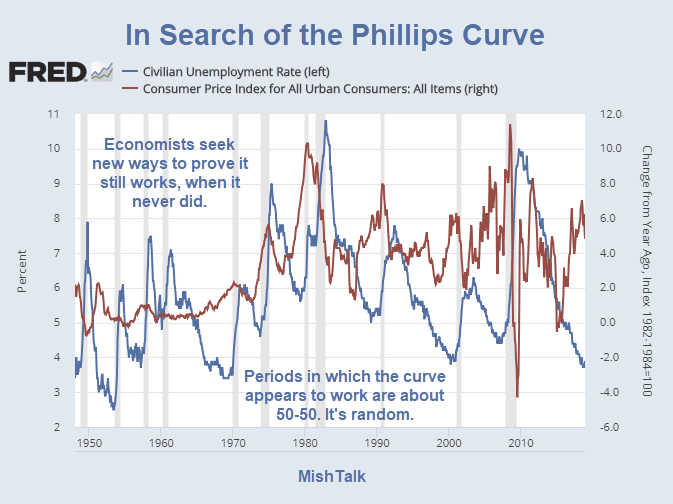

In search of the phillips curve

Unemployment vs CPI chart from St. Louis Fed, annotations by Mish

Fed studies debunk the Phillips curve

- Fed Study Shows Phillips Curve Is Useless

- Yet Another Fed Study Concludes Phillips Curve is Nonsense.

Both studies were done by Fed staffers.

Yet, Fed Chairs Janet Yellen and Jerome Powell did not believe the Fed's own study.

in March of 2017, Janet Yellen commented the "Phillips Curve is Alive“.

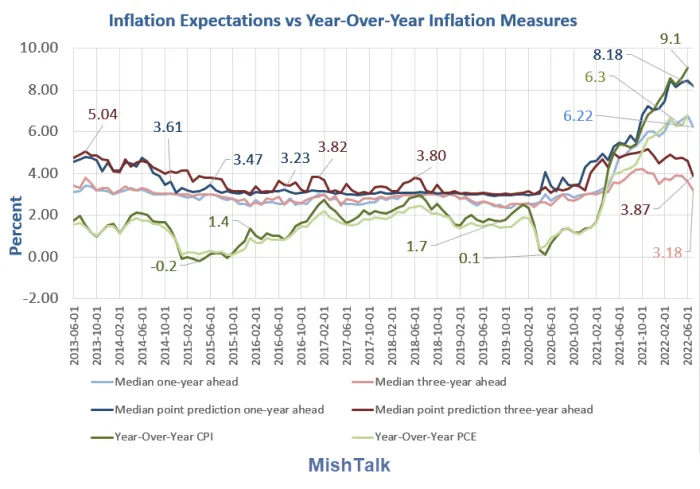

If inflation expectations mattered

If inflation expectations mattered, the above chart would not exist.

Let that sink in.

From 2013 to 2021 inflation expectations averaged well over three percent. Even with the Fed pumping hard with QE, the Fed could not get measured inflation over two percent!

How pathetic is that?

It's not really lack of inflation of course, but rather how senseless economists view it.

Factoring in home prices and asset bubbles there was massive inflation, just not where clueless economists wanted it.

Second Fed study concluded inflations expectations theory is nonsense

Also consider A Fed Economist Concludes the Widely Believed Inflations Expectations Theory is Nonsense.

Here are some excerpts from the actual study:

The direct evidence for an expected inflation channel was never very strong. Most empirical tests concerned themselves with the proposition that there was no permanent Phillips curve tradeoff, in the sense that the coefficients on lagged inflation in an inflation equation summed to one.

In addition, most standard tests of the new-Keynesian Phillips curve suffer from such severe potential misspecification issues or such profound weak identification problems as to provide no evidence one way or the other regarding the importance of expectations (much the same statement applies to empirical tests that use survey measures of expected inflation).

What little we know about firms’ price-setting behavior suggests that many tend to respond to cost increases only when they actually show up and are visible to their customers, rather than in a preemptive fashion.

It is far, far better and much safer to have a firm anchor in nonsense than to put out on the troubled seas of thought. John Kenneth Galbraith (1958).

Few things are harder to put up with than the annoyance of a good example. Mark Twain, The Tragedy of Pudd’nhead Wilson (1894)

One should not need a study to prove the obvious. And it's obvious that inflation expectation theory is nonsensical.

The reason has to do with the way inflation is calculated.

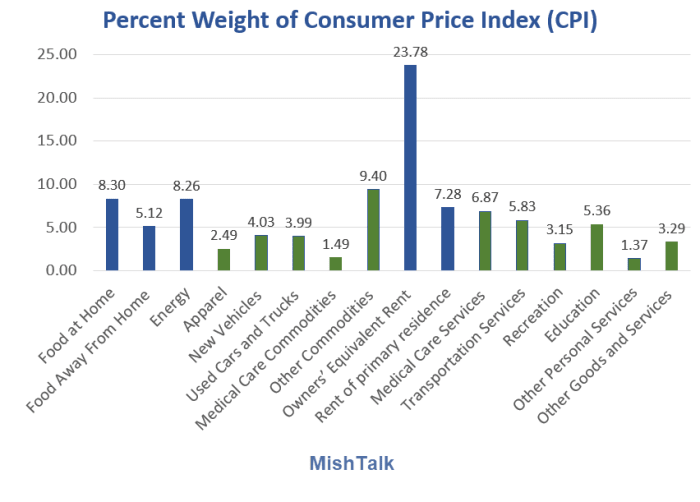

What can the Fed do about the price of food, medicine, gasoline, or rent?

CPI Weights from BLS chart by Mish

On March 20, I asked What Can the Fed Do About the Price of Food, Medicine, Gasoline, or Rent?

What the Fed can and cannot do

- The Fed cannot directly influence the price of anything because it cannot produce either goods or services.

- The Fed can reduce or increase demand where demand is elastic by raising or lowering the cost of money.

Elastic vs inelastic demand

- Elastic items total only 19.59%.

- Inelastic items total a whopping 80.41%.

This is why inflation Expectations theory the Fed abides by is total nonsense.

People will not rent two homes if they perceive prices will rise. Nor will people stop paying rent and wait for declines in they believe prices will fall.

The same applies to buying food, gas etc.

Stupidity well anchored: Absurdity of inflation expectations in graphic form

I discussed the silliness of inflations expectations theory in Stupidity Well Anchored: Absurdity of Inflation Expectations in Graphic Form

Inflation expectations Q&A

Q: If consumers think the price of food will drop, will they stop eating out?

Q: If consumers think the price of food will drop, will they stop eating at home?

Q: If consumers think the price of natural gas will drop, will they stop heating their homes and stop cooking to wait for the event.

Q: If consumers think the price of gas will drop, will they stop driving or not fill up their car if it is running on empty?

Q: If consumers think the price of gas will rise, can they do anything about it other than fill up their tank more frequently?

Q: If consumers think the price of rent will drop, will they hold off renting until that happens?

Q: If consumers think the price of rent will rise, will they rent two apartments to take advantage?

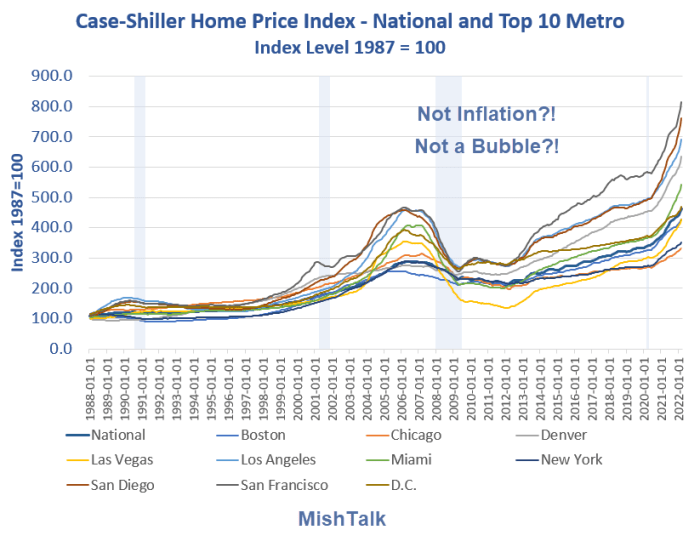

Asset irony

People will rush to buy stocks in a bubble if they think prices will rise. They will hold off buying stocks if they expect prices will go down.

People will buy houses to rent or fix up if they think home prices will rise. They will hold off housing speculation if they expect prices will drop.

The very things where expectations do matter are the very things the Fed ignores.

Demand destruction will occur in the small subset of elastic items plus housing and stocks.

Except as related to recreation and eating out, rate hikes will not impact food, energy, or shelter, the overwhelming majority of the CPI.

Stupidity still well anchored

Here we are with Powell, Barkin and other Fed presidents putting a spotlight on expectations, having ignored the third massive stock market bubble in just over 20 years.

Meanwhile, "there can be little doubt that poor people…are the chief sufferers of inflation."

Here's the deal in a nutshell: The Fed actively promotes inflation while pretending to be inflation fighters. Yet, people listen to these clueless jackasses as if they know what they are doing.

It's a good thing inflation expectations are not self-fulfilling because expectations became unglued in April.

Now they are crashing. It did not matter in April and it does not matter now.

It seems crazy that economists cannot see the obvious, even when its pointed out repeatedly.

The reason is as noted above: "It is far, far better and much safer to have a firm anchor in nonsense than to put out on the troubled seas of thought. John Kenneth Galbraith (1958)."

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc