India’s 10 year yield inching towards 6% as surge in CPI dims chances of rate cut

US initial weekly jobless claims fell below 1mn for the first time since March 21, coming in at 963k. Continuing claims also came in lower at 15.5mn against expectations of 15.9mn. Recovery in labor markets could reduce the impetus behind getting the second stimulus through and could make a case for making it smaller in size and more targeted instead. US yields rose post the data. US 10y yield climbed back above 0.70 for the first time since June. The US Dollar strengthened against majors.

India July CPI came in higher than expected at 6.93% against expectations of 6.25%. We may see some further paying in OIS and selling in bonds as markets would price out expectations of more accommodation from RBI. However, the higher print was primarily on account of higher food prices and with normal monsoons and a good Kharif harvest we may see inflation cool off in H2FY21. The RBI may announce an OMO or a special OMO (Operation Twist) to address nervousness in the bond market.

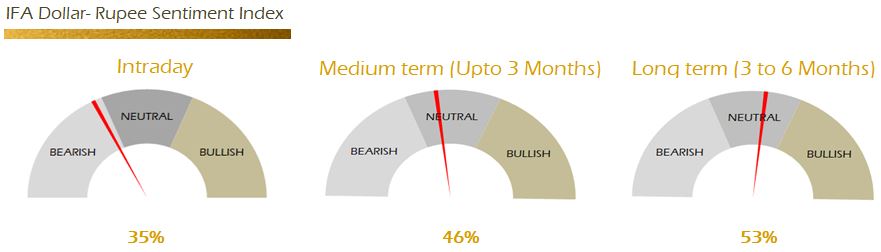

The Rupee continues to trade a very tight range. Nationalized banks continue to absorb inflows. We are likely to see an open around 74.85 and a range of 74.70-75.00 intraday. Nifty is likely to trade with a positive bias. We may see the next resistance around 11550 levels.

US July retail sales data is due today (exp 1.9% MoM)

Strategy: Exporters are advised to cover through Risk reversal strategy. Importers are advised to hold with a stop loss of 75.35. The 3M range for USDINR is 73.60 – 75.90 and the 6M range is 73.00 – 77.00.

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.