Income and spending steady as inflation cools

Summary

Today's personal income and spending report is a policymaker's dream. Consumer income remains strong, spending is more modest and most importantly core PCE inflation notched its smallest annual gain in more than three years.

At last, a more measured consumer

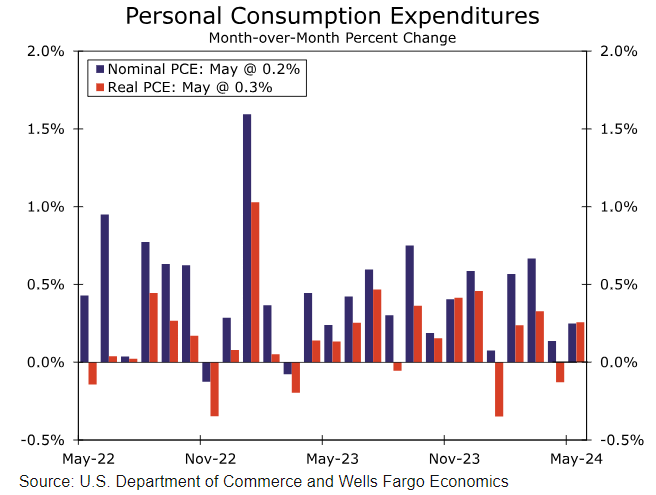

For anyone hoping to see a more reserved consumer and a taming of inflation, there was a lot to like in today's personal income and spending report for May. The staying power of the consumer remained intact. Personal spending rose 0.2% after a downwardly revised increase of just 0.1% in April (chart). After accounting for what was actually a scant decline in the PCE deflator and some fortunate rounding, real spending rose 0.3%.

The challenge for the Fed in this cycle has been getting the consumer to respond to a higher interest rate environment. Pandemic era savings and an increase in consumer credit extended the usual "long and variable" lags of monetary policy. But that period of extra liquidity and cheap credit is now largely behind us. That is evident in the slowing trend we have seen in personal spending. Critically though, personal income remained quite strong, rising 0.5% in the month which is a welcome development given that income growth has once again become the primary source of purchasing power for households. The saving rate came in at 3.9%. That is still low by historical standards, but it is the highest since January.

Improved prospects for a September rate cut

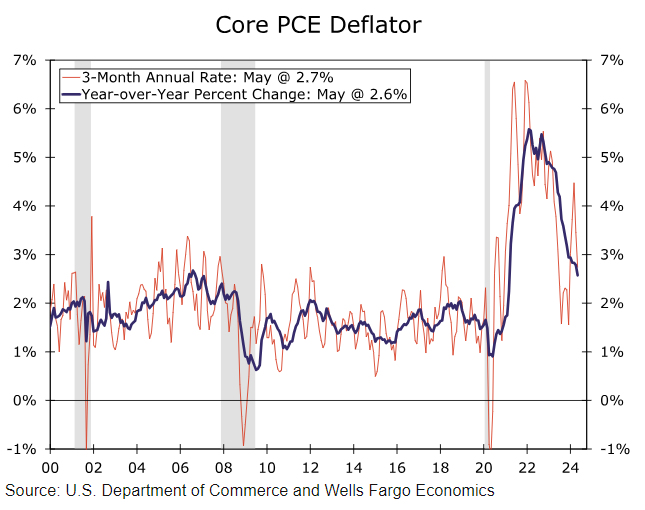

The PCE deflator was essentially flat (technically it fell 0.008%), putting the year-over-year rate at 2.6%. The core PCE deflator added a modest 0.1% in the month putting the annual rate for core inflation also at 2.6% (chart). On an unrounded basis, core PCE was up just 0.08%, the smallest rise since November 2020. Both gauges are above the Fed's 2.0% target, but core inflation is now showing the softest year-over-year inflation in more than three years, and headline is only a tenth away from its softest pace. It is another step in the right direction in terms of the fight against inflation.

Additionally, services inflation less housing, AKA supercore inflation, is coming to heel as well. For the first time this year, the 3-month annualized growth rate for supercore is below the year-over-year rate.

We see inflation pressures continuing to subside as the year progresses. It will be a close call between one or two 25 bps rate cuts, and the Committee seems evenly split between the two outcomes. Today's inflation numbers are another step in the right direction in terms of the fight against inflation and further the prospect that the FOMC could reduce the Fed fund rate as early as its September meeting.

Author

Wells Fargo Research Team

Wells Fargo