Housing down stocks up

Friday, Wall Street trading, saw strong gains to generate a good bounce after the previous sharp fall.

A significant driver were the comments of a Federal Reserve official to the effect that a lower 25 point rate hike, may now be appropriate. Certainly, the fundamental economic data is all pointing to a sharp weakening. One which could get away from the Fed. However, there is rarely full agreement, and the sway of the Chairman at any meeting of the FOMC, is always significant.

Running a little against market sentiment at the moment, I continue to forecast another two 50 point rate hikes. The market seems to now be setting itself up to be surprised by such a hike. Which means prices may be vulnerable around the next FOMC.

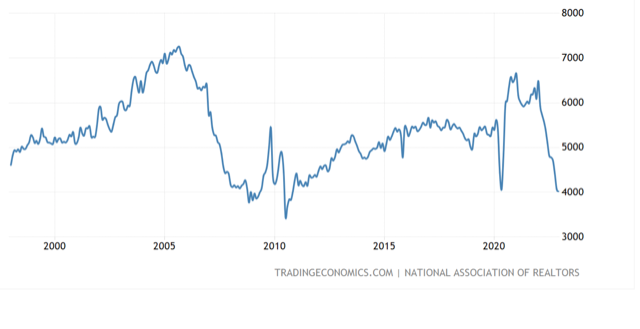

The big economic news on the day was the US Existing Home Sales data.

This saw a sharp drop to extremely concerning levels. Since 2021, I have been warning the US is already in its second great 'property bubble' that no one wants to talk about? Markets have chosen to look away from what was happening in housing, largely because it just feels too uncomfortable for all those big investment banks. Hence, commentaries have tended to be steered away from this area of the economy.

US Existing Home Sales are now lower than during the Covid lock-down period.

In fact, Existing Home Sales are now at full blown Global Financial Crisis levels, and back down to levels otherwise not seen since the 1980s.

This is as bad as it gets. It comes on top of a services sector that is already in contraction and a manufacturing sector that is clearly continuing to wind down. The US economy is literally in dire straits, and to quote “The Big Short” movie, "everyone is walking around like they are in an Enya video”.

The stock market is mistakenly fixated on the outlook for US rates as the be all and end all in deterring the trajectory of the market.

The core forces of the real economy and their impact on future earnings are being perilously neglected. When big tech lays off record numbers of workers, their stocks rally on the basis of the reduction in overheads. Ignoring the reasoning in back of those layoffs? The future is not so bright.

The end twist to all this is the harsh risk of a further 50 point rate hike at the next FOMC. Even at 25 points, it still means, rates, consumer, business and mortgage strain will continue to climb.

With the economy already in dire straits, with rates still going up, and the significant lag time of the full impact of the rate hikes still to be seen, we are moving from a question of a recession or not, to far more frighteningly, a question of whether the US will experience Recession, or indeed Depression?

At the very least, a severe Recession appears likely.

This is what we have been forecasting for over 12 months now. That US economic growth would be flat and dipping in and out of recession for several years.

This week sees Q4 GDP for the USA, that is likely to register a slowing from the 3.2% growth of Q3 to about 2.7%.

The global investment world is catching up with the reality of on the ground USA, and is why we are seeing simultaneous declines in stocks, property and the dollar.

Author

Clifford Bennett

Independent Analyst

With over 35 years of economic and market trading experience, Clifford Bennett (aka Big Call Bennett) is an internationally renowned predictor of the global financial markets, earning titles such as the “World’s most a