High yield bonds bounced 2.07% against Treasuries

Highlights:

Market Recap: The Dow rallied 512 points or 2% yesterday on the back of Federal Reserve Chairman Jerome Powell's comments that the Fed would support the economy. The S&P 500 closed back above 2800. The Russell 3000 index gained 2.22% and closed back above its 200 day moving average. The US 10 year yield rose 5 basis points to close at 2.12%.

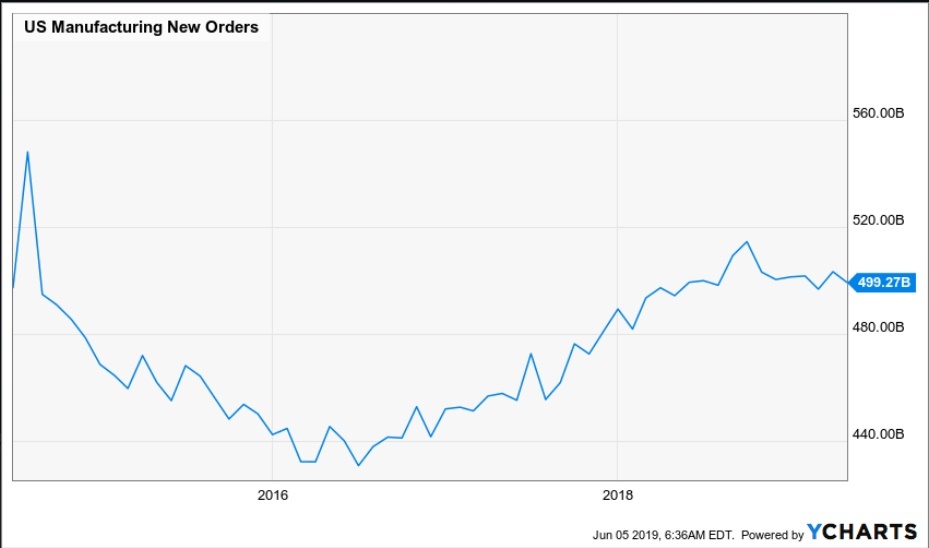

Economic Data: US Factory Orders are at a current level of 499.27B, down from 503.30B last month. This represents a monthly annualized growth rate of -9.59%, compared to a long-term average annualized growth rate of 3.30%.

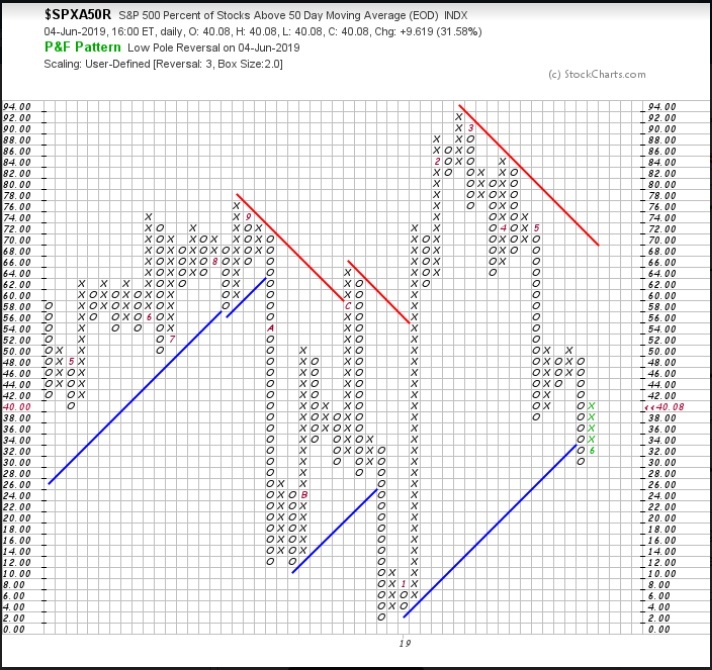

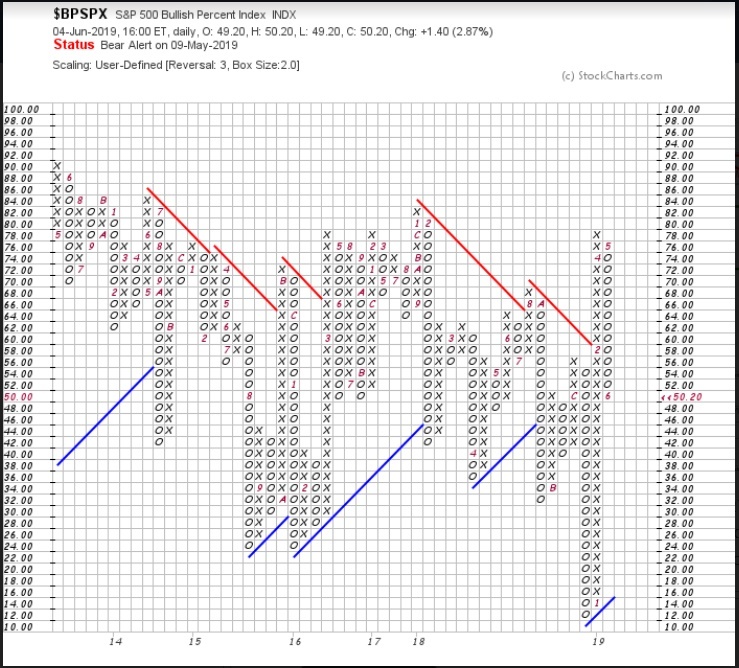

Market Internals: The percentage of stocks in the S&P 500 above their 50 day moving average bounced significantly yesterday, getting rid of oversold conditions. The point and figure chart reversed back into a column of X’s and is suggestive of continued upward movement in this index. The percentage of stocks in the S&P 500 above their 200 day moving average also moved back into a column of X’s. This particular measure of internal strength and weakness never got oversold in the recent declines. The bullish percent index of the S&P 500 remains in a column of O’s and is not oversold, even after yesterday’s bounce.

Lumber: Lumber bounced 4.77% against gold. Momentum is positively diverging and could suggest a retest of the old lows (to the upside) which could now act as new resistance.

Semiconductors: Semiconductors rose 1.89% against the S&P 500 yesterday and 4.10% on an absolute basis. If semiconductors continue to lead to the upside, the oversold rally that started yesterday could have more room to run.

Value: The value factor (VLUE) gained 2.92% and was the strongest performing factor yesterday. The value factor ETF remains in a negative trend and value remains one of the weakest relative factors over the last year.

High Yield: High yield bonds bounced 2.07% against Treasuries, rallying off support. Spreads have widened over the past several weeks up until yesterday. For this rally to take markets back to all-time highs, we will need to see leadership in high yield bonds and a tightening of spreads.

Futures Summary:

News from Bloomberg:

President Trump said there's always a chance of war with Iran. He told U.K. TV he'd rather talk to President Rouhani, but military action is possible if the country takes steps to get nuclear weapons. On the subject of weapons, he said he's seriously considering a ban on gun silencers, though he doesn't love the idea. Today he attends commemorations for the invasion that helped end World War II, before heading to Ireland. Follow along with our Trump Update.

The president said he's not bluffing about slapping tariffs on Mexican goods, according to a tweet he sent in response to Senator Chuck Schumer's comment that he won't follow through on the proposal. "He gave Mexico bad advice, no bluff!" Still, Republican Kevin Cramer predicted the Senate would have enough votes to override a presidential veto of any measure to stop the tariffs taking effect June 10.

The U.S. and China are heading for a stand-off over rare earths. The U.S. pledged unprecedented action to maintain supplies if the trade war prompts China or Russia to stop exports. Wilbur Ross said modern life would be impossible without them. China's Xi is meeting Vladimir Putin in Moscow today. The next U.S.-China contact comes this weekend when Steven Mnuchin and PBOC chief Yi Gang attend a G-20 meeting in Japan.

Wall Street brokers face the biggest overhaul in the rules governing their behavior in years. SEC commissioners will vote today to eradicate conflicts of interest, though critics say it's not enough. The new standards require broker-dealers to act in the best interest of customers and disclose pertinent relationships. But opponents want to impose a fiduciary duty to put clients' interests first.

U.S. stock-index futures rose with equities in Asia and Europe on the Fed's dovish signals and as Salesforce's upbeat forecast buoyed software companies. Treasuries and the dollar were steady. Gold jumped and the yen fell. The euro rallied as options show traders are most bullish on the currency since January 2018. Oil slid, while most industrial metals climbed.

Author

Clint Sorenson, CFA, CMT

WealthShield