Growing risk appetite fuelled by positive China data hitting USD once more [Video]

![Growing risk appetite fuelled by positive China data hitting USD once more [Video]](https://editorial.fxstreet.com/images/Markets/Currencies/Majors/NZDUSD/kiwi-dollar-62496010_XtraLarge.jpg)

Market Overview

Renewed positive risk appetite is hitting the dollar early this week. Positive newsflow of COVID vaccinations from AstraZeneca and Pfizer have helped to boost sentiment. The dollar is still perceived as a safe haven and as such is coming under pressure once more. This mood has been bolstered overnight, with the announcement of key Chinese data, with retail sales coming in ahead of expectation and back positive for the first time since the pandemic struck. The sharp appreciation of the Chinese yuan is certainly a signal of renewing risk and pressure on the dollar. Although Treasury yields are broadly steady in front of the two-day FOMC meeting, there is a perception that the Fed will confirm the lower for longer mantra for interest rates. This would lay further groundwork for a path of broad dollar weakening in the coming months. A dollar weakening is impacting across major forex pairs today, whilst gold and silver are also feeling the benefit. UK unemployment data for July broadly comes in ahead of expectations even though unemployment has ticked up to 4.1%, although this will worsen in the coming months as the furlough scheme is wound down. Sterling has been supported by this data.

Wall Street found support to climb higher last night, with the S&P 500 +1.3% at 3383. US futures are also gaining ground again today, with the E-mini S&Ps +0.3% today. This has generated a mixed session in Asia, with the Nikkei -0.5% but Shanghai Composite +0.2%. European markets look mildly higher with FTSE futures +0.1% and DAX futures +0.5%. In forex, we see a weaker USD across the major pairs, with the outperformance of AUD and NZD along with a relatively less strong JPY reflecting the improving appetite for risk. In commodities, a weaker dollar is supportive for gold (+$7 or +0.3%), with silver +0.7%. Oil has been starting to show signs of consolidation this week, with a key meeting of OPEC+ on Thursday.

There are several major announcements to be aware of on the economic calendar today. The German ZEW Economic Sentiment at 1000BST is expected to slip slightly to +69.8 in September (down from the record high of 71.5 in August). However, it is also worth watching out for the current conditions component which is expected to improve to -72.0 (from -81.3 last month). The New York Fed Manufacturing index is expected to improve to +6.0 in September (after dropping back to +3.7 in August). The US Industrial Production is expected to improve by +1.0% in the month of August (after growing by +3.0% in July) whilst Capacity Utilization is expected to improve to 71.4% (from 70.6% in July).

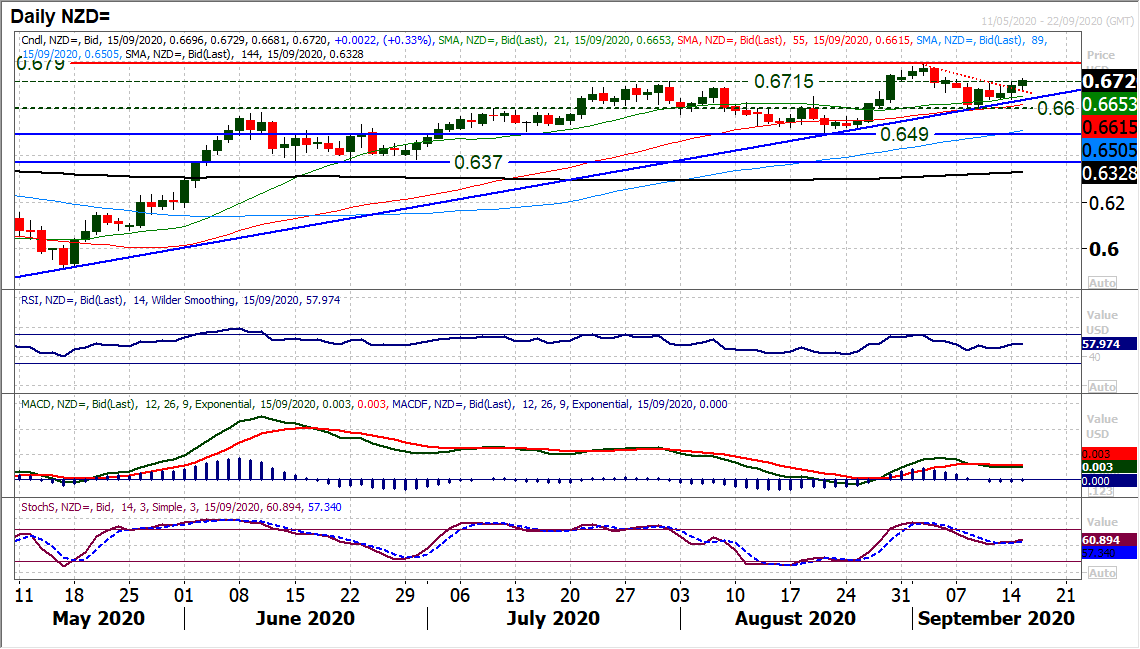

Chart of the Day – NZD/USD

The Kiwi looks increasingly as though a key shift in sentiment and relative performance has been seen. A couple of weeks ago we discussed the bullish breakout and the move to buying into weakness in the 0.6600/0.6715 support band. A correction went deeper into the band of support than we had been looking for, but the support around 0.6600 held firm, along with a six month uptrend and the bulls now look ready to take off again. Yesterday’s decisive positive candle has broken eight day downtrend, whilst improving momentum indicators come with upside potential. Early signs are positive again today with an initial move above 0.6715. A close back above 0.6715 would put the bulls back in the driving seat for another test of the key long term resistance at 0.6790. Above 0.6790 would then open 0.6940/0.6970. There is good near term support now around 0.6640 (building from lows of the past three sessions), also around the basis of support of the six month uptrend. Support at 0.6600 is increasingly key now as the next key higher low.

Brent Crude Oil

The downside move on the oil price may be continuing, but there is a notable reduction in the selling pressure over the past couple of sessions. Are there just signs of recovery potential forming? Another negative close on Brent Crude is now the ninth in the past ten sessions. Furthermore, there have now been ten lower daily highs in a row now. So this needs to change. Yesterday’s high of $40.10 will be the first barrier that needs to be broken. Interestingly, support at $39.30 was formed early last week, but this low has not been broken in the past four sessions. The key resistance that the bulls need to overcome is at $43.10 (the old July support), but if the market can begin to develop some positive candles, at least a basis of new support can begin to develop. A decisive close under $39.30 would though resume the downside and open $37.00 again.

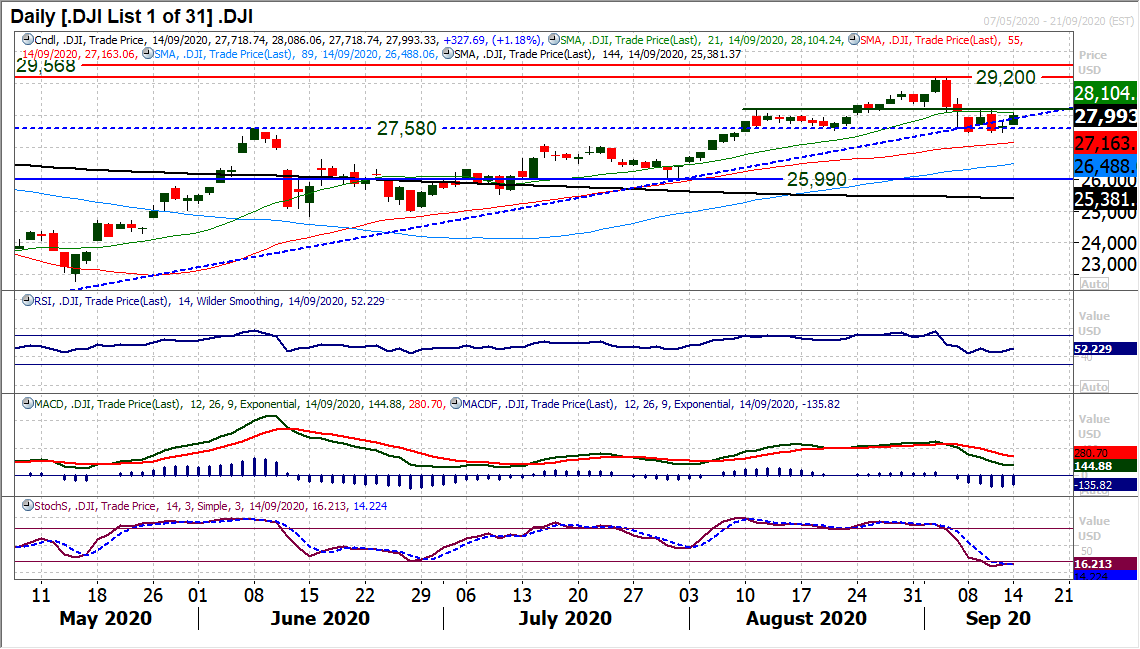

Dow Jones Industrial Average

A second consecutive positive close for the Dow has steadied the ship slightly. The threat of a potential five week top pattern is still there (a close below 27,465 would complete it) but the corrective momentum appears to have eased somewhat. The bulls will now be looking to close above last week’s high of 28,206 to suggest that improving momentum is now building. Daily Stochastics and RSI bottoming are encouraging. The hourly chart shows 27,830 as initial support, but the broader importance of the support band 27,465/27,580 is ever growing. We still favour buying into this weakness, but this would change below 27,465. A close above 28,206 would re-open the recent high of 29,200 with initial resistance at 28,540.

Other assets insights

EUR/USD Analysis: read now

GBP/USD Analysis: read now

USD/JPY Analysis: read now

GOLD Analysis: read now

Author

Richard Perry

Independent Analyst