Great Graphic: Growth in Federal Spending

The US policy mix is changing. The trajectory of fiscal policy is toward more stimulus, while the trajectory of monetary policy is toward less. That policy mix, expanding fiscal policy and less accommodative monetary policy is typically associated with an appreciating currency.

There are two big examples of this. The first is the Reagan-Volcker policy mix in the early 1980s that helped fuel the first dollar sustained dollar rally since the end of Bretton Woods. In September 1987, the major central banks agreed to drive it lower, and they did.

The other example of this policy mix is when the Berlin Wall fell. The German government financed the leveraged buyout of East Germany on favorable terms. The Bundesbank responded with tighter policy. This policy mixed fueled an overshoot of the German mark, not just against the dollar, but against the European currencies. This sparked a European currency crisis that led to the widening of the narrow ERM bands, and ultimately the monetary union.

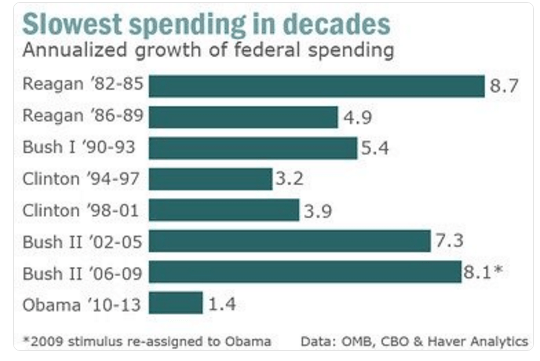

This Great Graphic (h/t Seth MacFarlane) shows the annualized growth of federal spending. It covers the 1982-2013 period. Contrary to what may be conventional wisdom, fiscal spending in the 2010-2013 period was the weakest. However, what is not captured is the most recent increase in federal spending. It rose 1% in 2014 and 3.1% in 2015. This fiscal year, spending is projected to rise 3.0%.

Even when the chart is updated, federal spending still rose the less under Obama's watch than any of the previous four presidents. Federal spending growth has bottomed, and that is before the next president takes the helm. As is often the case, a change in the direction of policy does always align with the start of a new Administration. For example, the deregulation and increased defense spending that is attributed to Reagan began under Carter, with deregulation of the airlines and the stepped up defense spending following the Soviet invasion of Afghanistan. Both main candidates advocated more public investment. To be sure, an increase in spending is not the same as increasing the deficit. The US deficit had fallen from 10.1% of GDP in 2009 to 2.6% in 2015. This year it is expected to be 3.1%.

Author

Marc Chandler

Marc to Market

Experience Marc Chandler's first job out of school was with a newswire and he covered currency futures and Eurodollar and Tbill futures.