Gold monthly: Losing momentum

Gold has sold off this week following the de-escalation in the global trade war. Meanwhile, ETF and central bank gold buying is easing. Is gold losing its momentum?

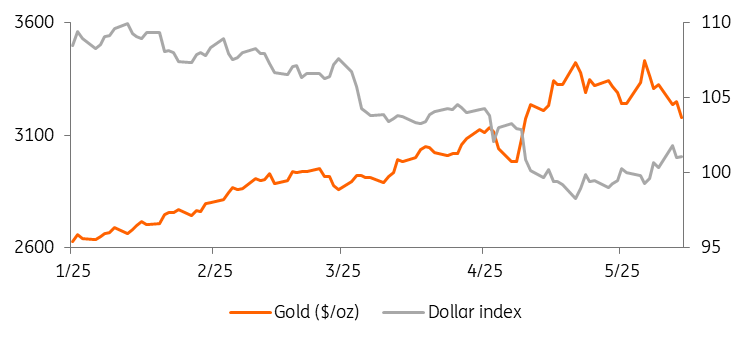

Gold tumbles on US-China trade truce

Source: Refinitiv, ING Research

Gold prices have dropped more than 3% so far this week to their lowest in more than a month, as improved risk sentiment is reducing gold’s haven appeal. But despite this week’s sell-off, gold is still up by more than 20% this year, after peaking at a record $3,500/oz in April, with the global trade war, geopolitical risks and central bank buying the key drivers for the precious metal’s rally.

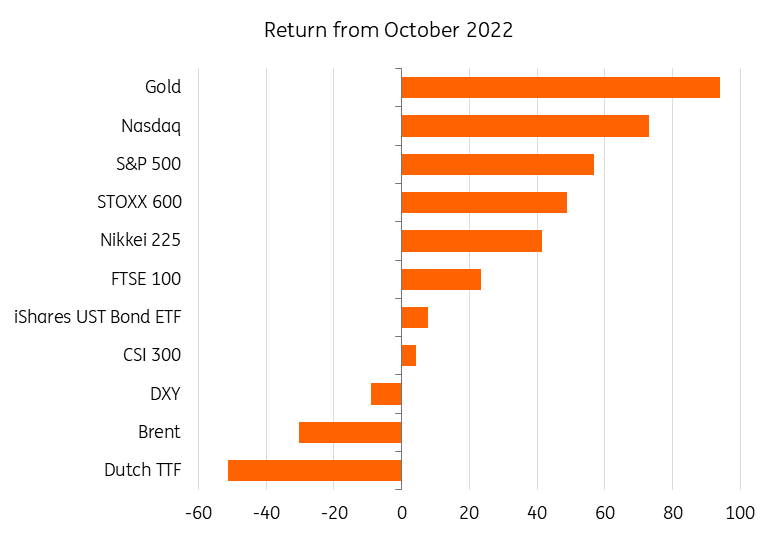

Gold is still outperforming

Source: Macrobond, ING Research

Trade optimism hurts safe haven demand

US President Donald Trump’s unpredictable trade policy has been the key driver for gold so far in 2025.

On Monday, the US and China agreed to temporarily reduce tariffs on each other’s goods, with the US slashing duties on Chinese products to 30% from 145% for a 90-day period, while Beijing reduced its levy on most goods to 10%. As part of the tariff truce, China also suspended a ban on exports of items with both military and civil applications to 28 US companies, as well as a trade and investment ban against 17 US companies.

This de-escalation in the global trade war is hurting demand for havens like gold.

Monday marked a substantial cooling of trade tensions between the US and China. However, questions remain for markets as to what the end game will be, as the measure will be operational for 90 days, and what the eventual level of tariffs will be.

US Secretary of the Treasury Scott Bessent later said it is “implausible” that reciprocal tariffs on China go below 10%, but the 2 April level – set by the President at 34% – “would be a ceiling”, while Trump said tariffs could go higher again if the two countries fail to reach an agreement.

Meanwhile, US inflation figures for April were softer-than-expected, suggesting only a limited impact from Trump’s tariffs so far. This has calmed recession fears and led to a scaling back of expectations for aggressive rate cuts by the Federal Reserve. Traders now see at least two rate reductions this year, with the first likely in September. Higher rates tend to be negative for non-interest-bearing gold.

Still, the US-China talks are only just beginning, and there remains plenty of uncertainty with a three-month negotiation period ahead of us.

With trade uncertainty remaining, the downside for gold could be limited. And if trade negotiations turn sour, that will push gold prices higher once again.

ETF buying is cooling off

Meanwhile, ETF buying – another key driver this year – has been cooling off since late April. If these outflows continue, this could add further headwinds to gold. Investor holdings in gold ETFs generally rise when gold prices rise, and vice versa.

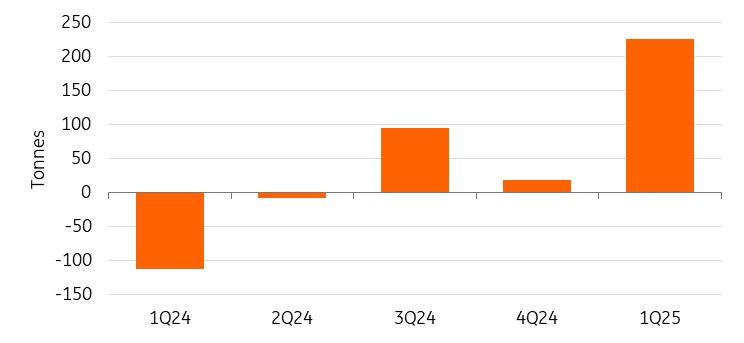

Still, the first quarter of the year saw a sharp revival in ETF inflows – marking the strongest quarter since 1Q22 – which was pivotal to gold’s rally.

1Q ETF inflows were pivotal to Gold’s rally

Source: World Gold Council, ING Research

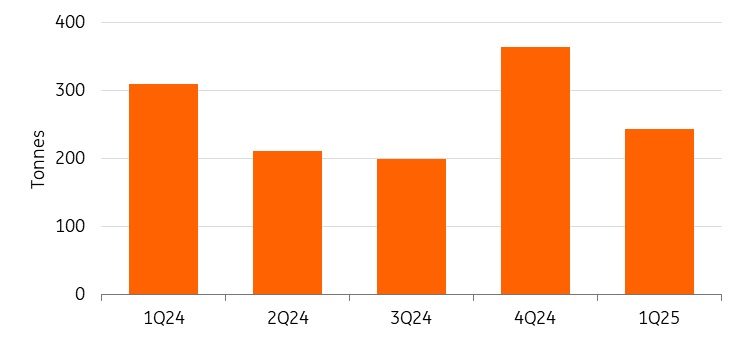

Central banks buying is easing

Gold’s rally in 2024 was driven by central bank buying, but this has started to ease too. Although central banks are still buying gold, the pace of purchases has slowed as prices hit record highs. In the first quarter, central banks bought 244 tonnes of gold. This was down 33% from the previous quarter.

Central banks bought less Gold in 1Q

Source: World Gold Council, ING Research

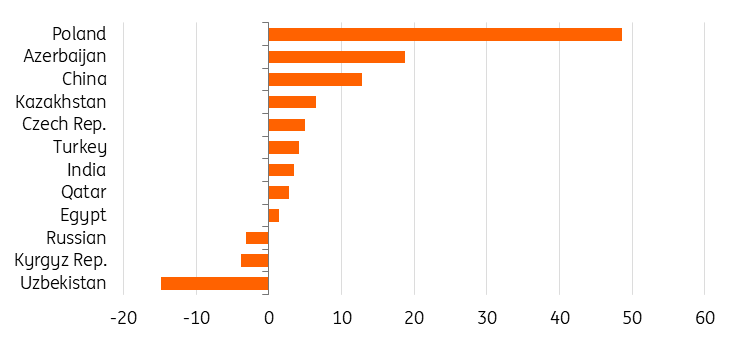

Year-to-date central bank purchases by country (tonnes)

Source: World Gold Council, ING Research

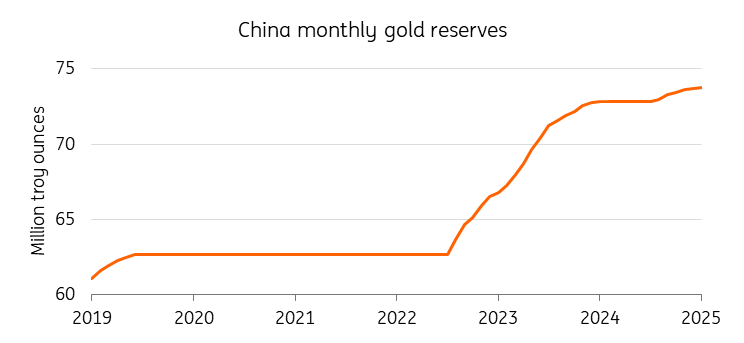

China is also buying less gold. In April, China’s central bank expanded its gold reserves for the sixth consecutive month, however by less than in previous months. Reported gold reserves in China rose by 2.2 tonnes in April, lifting the total to 2,295 tonnes, or 6.8% of overall reserve assets. So far in 2025, China has announced an increase of 14.9 tonnes in its official gold holdings.

China kept buying Gold in April but at a slower pace

Despite the slowdown, central banks are likely to continue to add gold to their reserves given the still-uncertain economic environment and the drive to diversify away from the US dollar. In the past six months, volumes have climbed by about 30 tonnes.

The pace of annual purchases by central banks has doubled since the outbreak of the Russia-Ukraine war in 2022, from about 500 metric tonnes a year to more than 1,000. Central banks’ appetite for gold is also driven by concerns from countries about Russian-style sanctions on their foreign assets in the wake of decisions made by the US and Europe to freeze Russian assets, as well as shifting strategies on currency reserves.

Last year, central banks bought a combined 1,045 tonnes, accounting for about a fifth of overall demand. Poland, India and Turkey were the largest buyers in 2024, according to the World Gold Council.

Consolidation mode

In the short term, gold is likely to consolidate at the current levels as trade and geopolitical tensions cool, at least for now, driving reallocation away from haven assets. We see gold prices averaging $3,250/oz in the second quarter. We expect an average of $3,128/oz in 2025.

Read the original analysis: Gold Monthly: Losing momentum

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.