Gold is no longer trading like a safe haven – It is trading like collateral damage

Collateral damage

I have been fielding a steady stream of questions from both short-term traders and longer-term gold holders after the latest meltdown cut through the 200-day moving average and then turned into something closer to an avalanche. The metal was already wobbling, but once the 200 DMA gave way, the floorboards came loose. Stops got hit, momentum signals deteriorated, systematic buyers stepped back, and what should have been the market’s safety blanket started trading like an asset on the liquidation menu.

Goldman Sachs

That is the part people are struggling with. Gold had every excuse to rally. Geopolitical tension is alive. Volatility is elevated. Equity leadership is cracking. Oil is still a macro threat. The Fed debate is unstable. The dollar debasement argument has not disappeared. And yet gold keeps selling off.

That tells you the market is not trading the brochure. It is trading the plumbing.

Gold is no longer trading like a safe haven. It is trading like collateral damage.

The first thing to understand is that this is not necessarily the long-term gold thesis being taken behind the woodshed. It is the short-term market structure taking control of the tape. When liquidity gets tight, investors do not always sell what they want to sell. They sell what they can sell. Gold is deep, liquid, widely owned, and for many portfolios still sitting on large accumulated gains. That makes it a natural source of cash when risk books need to be cleaned up in a hurry.

So the question is not simply, why is gold not rallying on geopolitical risk? The better question is, who still needs to reduce risk, where are the stops, and how much gold is sitting in portfolios as ready-made funding?

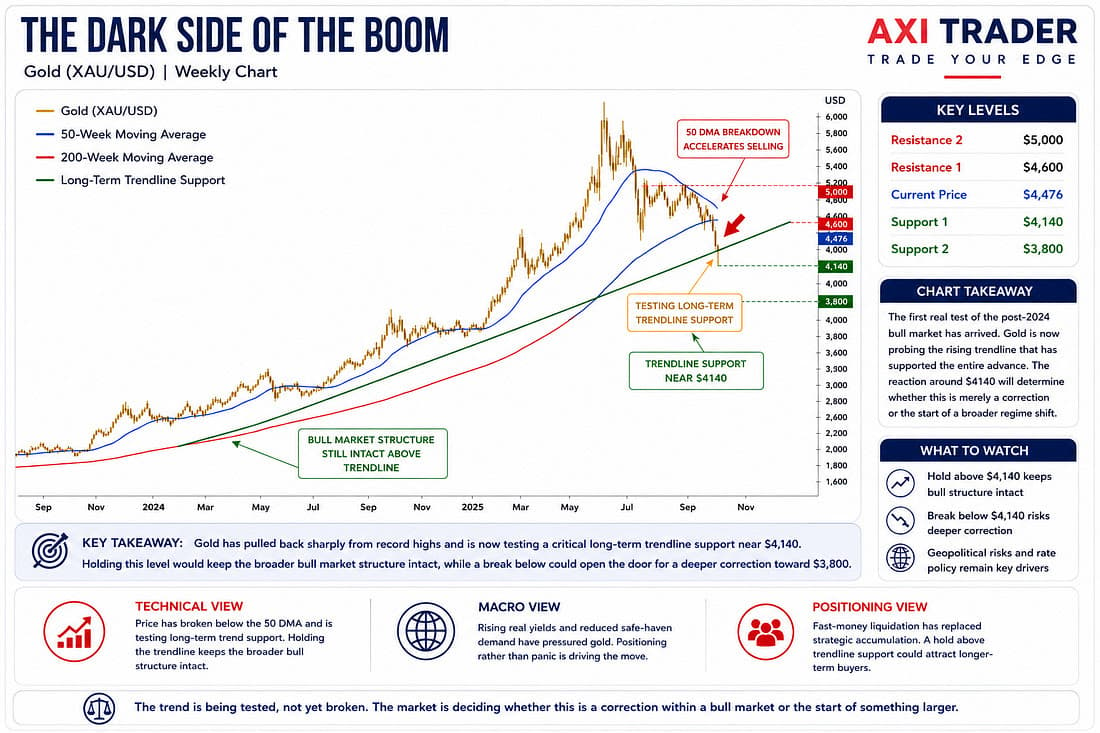

The 200 DMA mattered because it was not just another line on a chart. It was the dividing line between gold as a strategic holding and gold as a tactical trade. Above it, longer-term investors could still tell themselves the trend was intact. Below it, the conversation changes. The market stops debating fiscal deficits, central bank reserves, dollar debasement and monetary history. It starts by asking where the next stop-loss cluster is.

That is when gold moves from a macro asset to a fast-money instrument.

The implication is blunt. Once the 200 DMA breaks, conviction holders become nervous holders, tactical longs become trapped longs, and dip buyers start demanding proof instead of just a story. The tape no longer rewards elegant macro arguments. It rewards liquidity, timing and discipline.

A quick hat tip before we get into the weeds. A number of the chart ideas below were sparked by The Market Ear, the Oracle of Charts, whose work remains one of the best daily dashboards for cutting through the noise. The interpretation, trader framing and collateral damage thesis are mine, but several of the visual prompts deserve proper credit.

The momentum setup is now ugly. The 21-day moving average is rapidly approaching the 200-day moving average, and while that is a slower signal, a bearish cross would hardly be comforting. The bull market began with the opposite setup, a golden cross. Now the market is flirting with the mirror image at exactly the wrong time, when confidence is thin, and rallies are being treated as exits rather than fresh entry points.

Gold is oversold, but oversold is not the same as safe. RSI around 26.9 tells you the metal is stretched and may be due for a tactical bounce. But an oversold bounce is not a repaired market. It is just the rubber band snapping back after being pulled too far.

That is a trader’s distinction, and it matters. A bounce can come quickly from here, especially if shorts press too hard or front-end volatility starts to unwind. But unless that bounce comes with softer real yields, a weaker dollar, better ETF demand, or a reclaim of the 200 DMA, it risks becoming just another relief rally into supply.

In other words, gold can bounce because it is tired. It cannot trend again until it proves buyers are back.

The bigger problem is that gold has reconnected with its old enemies: US real yields and the dollar.

During the central bank-driven gold rally of 2022 to 2024, the historical negative correlation between US real rates and gold weakened badly. Central bank buying was powerful enough to bend the old rule book. Gold could rally even when the textbook said it should struggle because official-sector demand was strategic, persistent, and less price-sensitive.

But that phase now looks different. As non-central bank investors regain influence over the tape, the old macro gravity is returning. Gold’s negative relationship with US real rates and the dollar has strengthened again, and that is a major shift. It means the market is no longer giving gold a free pass on higher real yields or firmer dollar funding conditions.

Joni Teves at UBS doesn’t see a recovery any time soon, as the old relationship with real rates reasserts itself: Gold’s negative relationship with US real rates and the dollar has become stronger of late. Meanwhile, gold has been moving with a strong positive correlation with equities and a strong negative relationship with oil. For now, it is difficult to see what could break gold out of the recent range. While it is encouraging to see speculative positions remain quite muted, there is also little evidence of an appetite to materially rebuild exposure at the moment.

This is where the pushback against the dollar debasement trade really bites. The long-term thesis has not disappeared. But markets do not always trade the ten-year essay. Sometimes they trade the next funding squeeze, the next real yield move, the next margin call and the next portfolio manager who needs to reduce gross exposure before the close.

The market is asking a colder question now: if real yields are not falling, if dollars are still in demand, and if liquidity is being pulled toward cash, why should gold command a premium today?

This is also where the correlation story gets uncomfortable. Gold has recently been moving with a strong positive correlation to equities and a strong negative relationship with oil. That is close to the opposite of what many investors want from it. Instead of acting as a clean hedge against equity stress or an obvious beneficiary of geopolitical risk, gold is trading like part of the same risk-beta-reduction complex.

That matters enormously. If equities sell off and gold does too, the metal is not doing its portfolio job. If oil rises amid geopolitical tensions and gold still cannot rally, then the market is not treating gold as a clean inflation or crisis hedge. It is treating it as a liquid asset trapped inside the broader deleveraging cycle.

That is the collateral damage framework. Gold is not being judged by the macro brochure. It is being judged by its correlation map. And right now that map is telling you the metal is behaving less like insurance and more like a funding asset.

The implication for traders is clear. Do not assume geopolitical risk with oil involved equals gold upside. In a textbook world, yes, geopolitical stress lifts gold. In this tape, if geopolitical stress triggers another equity drawdown, margin pressure, or a broader volatility shock, gold can still be sold because it is liquid, profitable, and easy to raise cash against.

That is the difference between theory and the tape.

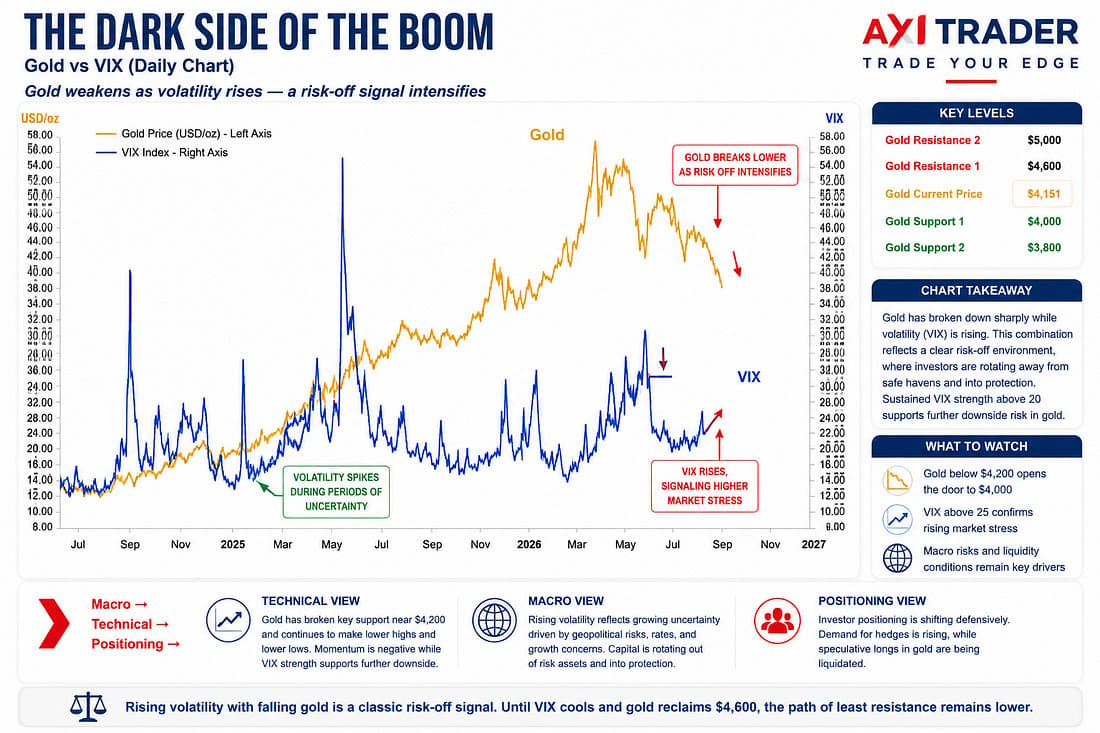

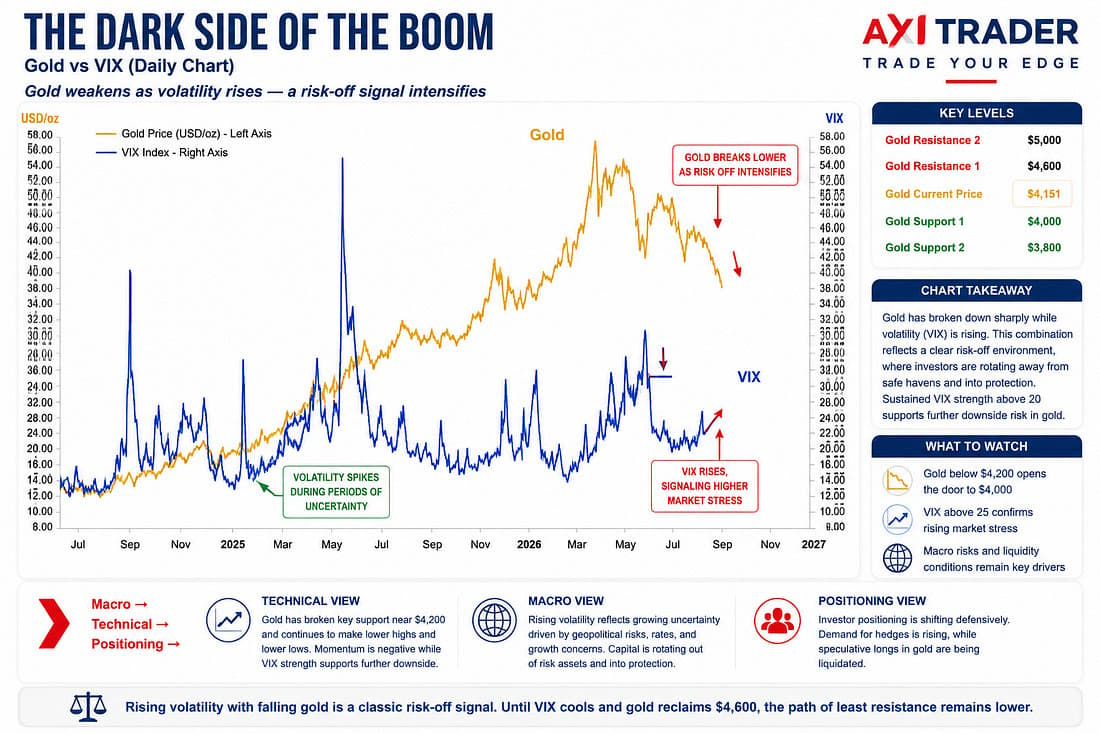

This is why the safe haven label needs to be handled with care. Gold is not a universal hedge. It is a hedge under certain conditions, and those conditions matter. Over recent months, some of the sharpest VIX spikes have coincided with aggressive selling in gold. That is the tell. When volatility rises because investors are de risking, gold can get dragged into the same liquidation machine as everything else.

In that environment, gold is not the fire shelter. It is the asset being sold to pay for the fire damage.

That does not destroy its long-term role. It does not erase central bank demand. It does not cancel the fiscal concern. But it does mean that in a liquidity shock, gold can behave less like insurance and more like an ATM.

The options market is now saying the same thing as spot. Gold normally trades with upside skew: gold up, gold volatility up; gold down, gold volatility down. That is the classic gold pattern. Investors usually pay for upside convexity because gold has that crisis bid embedded in its DNA.

But this latest selloff has seen volatility catch a strong bid on the downside. UBS notes that realized volatility remains well below implied volatility, suggesting front-end vol could unwind sharply if gold stabilizes or rallies. But the more important point is the shift in skew.

The 1-month risk reversal now favours puts by around 3.5 volatility points, compared with roughly flat a month ago and only about 0.5 vols in favour of puts last week. That is a serious repricing of downside protection. In plain English, traders are not just selling gold. They are paying up for insurance against more downside.

That is confidence cracking in the options market.

The implication is that the market has moved from disappointment to protection mode. When skew moves that fast, it tells you the street is no longer just debating whether gold is cheap. It is asking how much worse the liquidation could get if the next level gives way.

For short-term traders, that means two things. First, chasing shorts after an oversold break can be dangerous because implied vol is already rich and downside hedging has moved a long way. Second, buying the dip blindly is just as dangerous because the options market is telling you that fear has not yet cleared.

This is not a clean bottoming pattern. It is a market trying to find out where forced selling ends and real demand begins.

Then there is the competition for capital. Gold’s biggest problem may not be inflation, rates or geopolitics. It may be that investors have found a shinier toy. AI-linked equities, semiconductor trades, leveraged ETFs, and high-beta growth have been sucking up oxygen. Even after the tech wobble, capital is still conditioned to chase the next growth engine rather than hide in a metal that suddenly cannot defend its own trend line.

That is why this move feels so bearish. Gold is not falling because the macro backdrop is obviously hostile. It is falling despite having every reason to rise.

When an asset cannot rally on good news, you need to respect the message. The market may not be saying the long-term gold thesis is dead. But it is saying the current holder base is tired, the fast money is in control, and fresh buyers are not yet willing to step in with conviction.

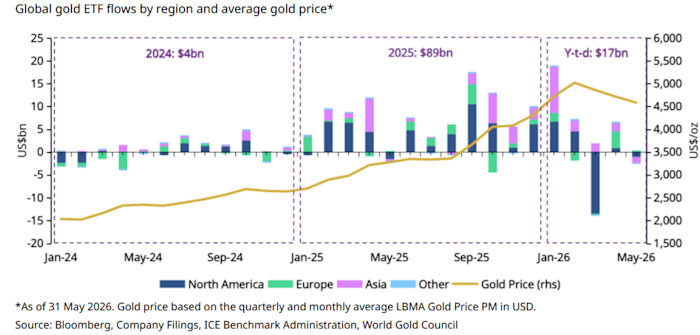

ETF demand has lost its shine. Speculative positions are muted, which is both good and bad. The good news is that gold is not sitting on a giant speculative long that still needs to be completely flushed. The bad news is that muted positioning also suggests there is little evidence that investors want to materially rebuild exposure right now.

That is the real problem. The market is not overloaded with gold bulls. It is simply not interested enough to defend the tape.

For longer-term holders, that is uncomfortable but not fatal. It means the long term case needs time and better price action to reassert itself. For short-term traders, it means discipline matters more than conviction. Catching a falling knife below the 200 DMA is not a strategy. It is a coin toss unless the risk is defined before the trade is placed.

Gold can bounce from here. In fact, the oversold setup, stretched momentum, and heavy downside hedging all create the possibility of a sharp relief rally if the selling pressure exhausts itself. If sentiment stabilizes, systematic buyers could re-enter the market faster than expected. Goldman has flagged that kind of re-engagement risk before, and gold is the type of market where confidence can disappear quickly and return almost as quickly.

But the trigger has to be visible. A softer real yield impulse. A weaker dollar. A reclaim of the 200 DMA. Stabilization in ETF flows. A volatility reset. A sign that rallies are being bought rather than sold.

Until then, every bounce risks running into the same wall: trapped longs looking to reduce, fast money looking to fade, and portfolio managers still treating gold as a source of cash.

So when can Gold rally?

Gold can rally when it stops behaving like collateral damage. It needs to decouple from equity stress, stop trading like an ATM during volatility spikes, and rebuild the safe-haven premium that has been leaking out of the market. It does not need the perfect macro backdrop. It already has plenty of macro reasons to work. What it needs now is proof that the selling is done and that the buyer base is willing to defend the trend again.

The trader view is simple. Respect the technicals. Respect the options market. Respect the renewed real yield and dollar sensitivity. And above all, respect the fact that a market with every reason to rally but still falling is sending a message.

Gold is not broken as a long-term asset.

But right now, it is broken as a hedge.

And in this tape, that is enough to keep the fast money in charge.

For now, gold is being treated less like insurance and more like collateral damage.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.