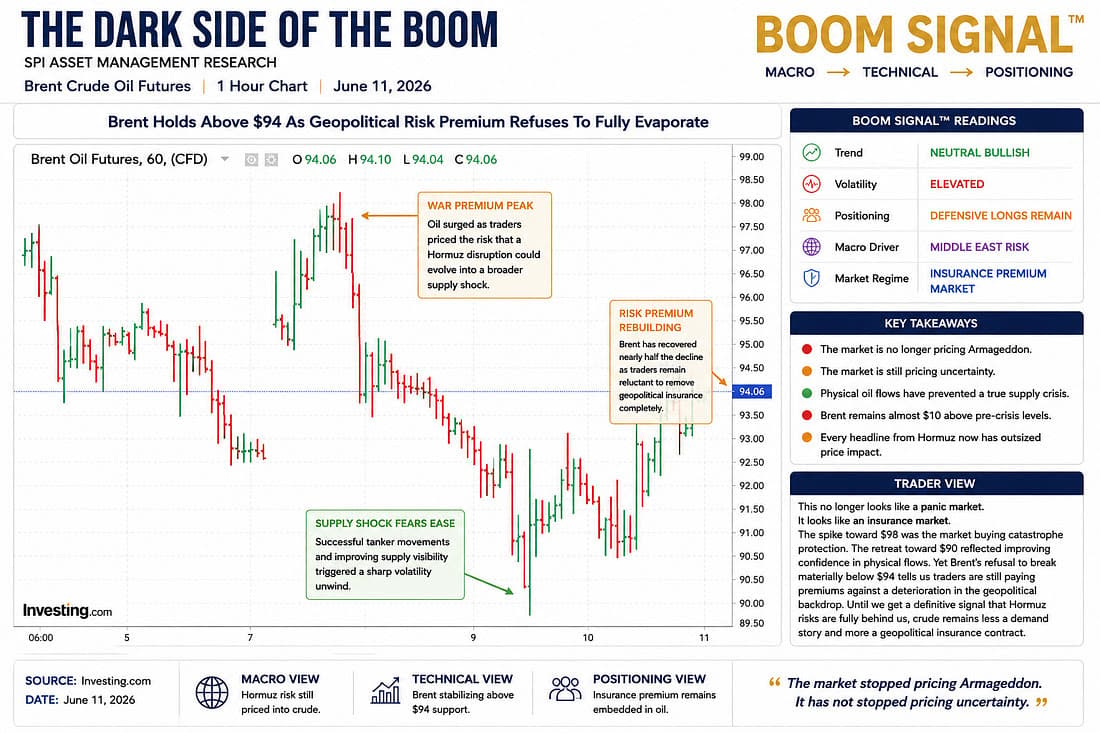

Oil is trading shadows on a radar screen

- Brent in the mid-$90s is not pricing in a full Hormuz shutdown. It is pricing a dangerous, impaired chokepoint where barrels are still escaping.

- Dark tanker movements on the Omani side are the key reason crude has not exploded. The market cares more about ships moving than headlines shouting.

- US support operations may reduce the immediate supply shock, but they also risk forcing Iran to prove it still has control over the Strait.

- The physical market is now the signal. Tanker flows, AIS gaps, insurance, freight, Brent Dubai, time spreads, and Asian arrivals matter most.

- My base case is still a short affair, but if the barrel flow stops, crude can reprice violently because the market is still carrying a fat tail under the inventory surface.

Trading shadows on a radar screen

The oil market is no longer trading a clean barrel count. It is trading shadows on a radar screen, tankers running dark, missiles in the air, diplomacy wearing a flak jacket, and every macro desk trying to decide whether the Strait of Hormuz is merely impaired or about to become the fuse that relights the inflation trade.

Brent near $95 and WTI near $91 say traders are worried, but not terrified. That is the tell. If Hormuz were truly shut, Brent crude would not be politely leaning against the mid $90s. It would be kicking the door off the hinges. The market is not calm because the risk has disappeared. It is calm because barrels are still leaking through the cracks.

The latest escalation has teeth. US forces launched fresh strikes against Iranian surveillance, communications and air defence sites after Washington accused Tehran of dragging its feet on a deal and after the downing of a US Apache helicopter over the Strait. Iran responded by declaring the waterway closed to all vessels, warning that ships attempting to cross would be treated as targets. Tehran also claimed strikes against US-linked facilities in Bahrain and Kuwait, while Kuwait closed its airspace and Iranian state media pointed to a missile attack on an air base in Jordan. This is not background noise. This is the market hearing heavy furniture being dragged across the ceiling.

Yet the tape says the artery is damaged, not severed.

That is where the tanker evidence matters more than the speeches. The Strait has become a midnight goat track for supertankers, with vessels hugging the Omani coastline, some running dark, some switching off AIS and GPS signals, and some moving under US air cover. Around 15 ships a day are reportedly getting in and out through that Omani route, many of them oil tankers. That is far below the roughly 135 ships a day before the conflict, so nobody should mistake this for normality. But it is not zero. In crude, zero is the monster.

That is why oil has not exploded. Public tracking can understate real flows because the most important ships are often the ones trying hardest not to be seen. AIS gaps, dark transits, route changes and actual arrivals into Asia now matter more than another press conference. The tanker tape is the truth serum. The speeches are the smoke machine.

President Trump’s claim that a secret US mission helped move more than 200 commercial vessels and more than 100 million barrels through the Strait should be handled carefully because this is wartime messaging as much as logistics. But the broader point fits the market. If more oil has been moving than feared, it explains why Brent has not blown through $100 despite strikes, airspace closures and direct threats against shipping.

The risk is that success creates its own problem. If Washington has found a way to keep barrels moving through the Omani side, Iran’s strongest oil card starts to leak. That gives the US more room to push harder, but it also raises the odds Tehran feels forced to prove it still controls the chokepoint. The secret mission may have bought the market oxygen, but oxygen around a spark is not exactly comforting.

The physical balance still matters. The disruption has constrained access to a huge amount of normal Gulf flow, with roughly 12 million barrels a day tied to the chokepoint. Yet Iraq, Kuwait and the UAE are still believed to be moving around 3 million barrels a day through the Strait. Kuwait stock draws near the end of May, suggesting more loading activity than the visible market initially assumed. Every barrel that gets out delays the inventory depletion clock and keeps summer tightness from going feral.

But leakage is not safety. It is only time bought at a higher insurance premium.

Diplomacy is still in the room, but it is no longer sitting at the head of the table. Pakistan and Qatar have been trying to bridge the gap, while President Trump has been pressing for a deal to extend the April ceasefire, reopen the Strait and restart nuclear talks. But when bombs become part of the negotiation table, the market hears the message clearly. This is diplomacy with a naval escort and a live fire premium.

My base case remains that this stays a short affair rather than becoming a full energy war spiral. President Trump has one eye firmly on the oil screen. Controlled pressure is politically usable. A disorderly oil shock is a midterm election GOP nightmare. Once crude starts pushing significantly higher, the olive branch usually comes back fast because oil is never just oil. It is gasoline, inflation expectations, bond yields, the Fed path, consumer confidence and risk appetite all wired into the same fuse box.

For traders, the guide is physical evidence, not political volume. Watch tanker flows, AIS gaps, insurance, freight, Brent Dubai spreads, time spreads, refinery margins, Kuwait, Iraq and UAE loadings, and whether barrels are actually arriving in Asia. The next $10 in crude will not come from a podium. It will come from one missing convoy, one closed lane, one accident in the blind corner, or one tanker that fails to arrive.

Oil is trading a damaged artery with a military bypass. As long as barrels move, crude trades insurance rather than Armageddon. If the flow stops, crude trades panic. The secret mission may have kept the artery open, but it may also have moved the market from supply relief to escalation risk. Hormuz is not fully closed, but it is no longer open in any normal sense. It is the world’s most expensive blind corner, and every trader is now listening for brakes in the dark.

Here, JPM suggests that Bloomberg's data shows muted transits, as it can't maintain an accurate read of actual crossings because AIS transponders are turned off during crossings.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)