Gold builds a floor as China crashes the memory party and Korea’s leverage trade unwinds

Gold market daily: Higher rates today are building the foundations for higher Gold tomorrow

Gold has been punished over the past few months by a monetary tightening cycle that has not even fully arrived.

The metal’s retreat from January’s record highs followed one of the sharpest reversals in Federal Reserve expectations in years. Markets went from pricing two or three rate cuts to leaning toward a possible rate hike in 2026 as the Middle East energy shock pushed inflation expectations, Treasury yields and the U.S. dollar higher.

That combination landed on bullion like a three-legged stool falling down a staircase.

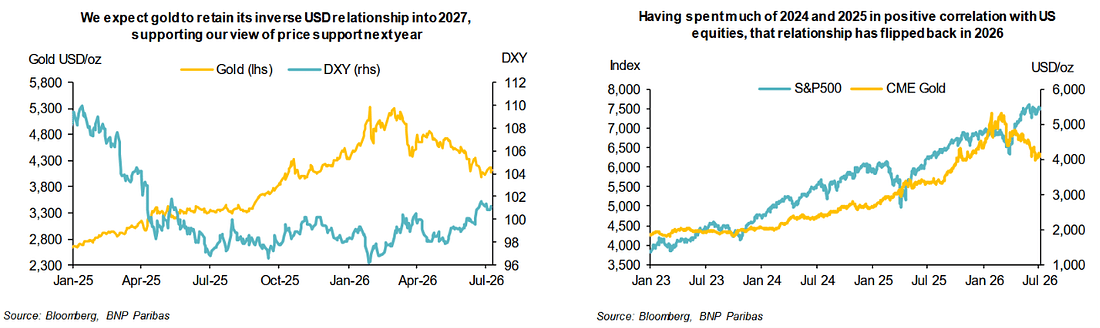

Gold dropped from roughly $5,400/oz in early March to around $4,030/oz by mid-June before finding its feet near $4,200/oz. BNP Paribas has consequently lowered its near-term forecasts, but the investment bank remains bullish on the broader trajectory from current levels.

The distinction matters. This is not a broken gold story. It is a strong long-term structure being forced through a hostile short-term interest-rate window.

The market has recently focused less on inflation itself and more on what inflation might force the Federal Reserve to do. Higher energy prices would normally add fuel to gold through rising inflation expectations and concerns about purchasing power. This time, the first reaction has been different. Oil fed expectations of tighter monetary policy, higher yields and a stronger dollar, turning what might once have been bullish inflation into a monetary headwind.

Gold has therefore been trading in response to central bank policy rather than the inflation shock.

That pressure may persist while investors continue debating whether the Fed will tighten again. But BNP argues that monetary policy is only one layer of the market, not the entire geological map. Once the rate repricing loses momentum, the structural supports beneath bullion should become easier to see.

The dollar is central to that view. BNP expects gold’s traditional inverse relationship with the greenback to reassert itself as the U.S. currency gradually weakens into 2027. Gold does not need the dollar to collapse. It only needs the current rate advantage to stop widening and the monetary tide to begin drifting the other way.

The stronger part of the bull case, however, sits in the physical market.

Chinese investors purchased a record 210.7 tonnes of bars and coins in the first quarter, while China’s gold imports rose 76% from a year earlier through May. Weak domestic property markets, low interest rates and persistent demand for hard assets continue redirecting household capital toward bullion.

That buying has become the keel beneath the gold market.

Western ETF investors have been sailing in the opposite direction, reducing global holdings by 78 tonnes year to date as investors took profits following January’s surge. But BNP’s conclusion is that Asian physical demand has more than absorbed those outflows. The paper market has been lightening its load while the physical market has been quietly stacking the cargo.

That is why the correction should not automatically be mistaken for the end of the cycle. Higher rates can cap gold in the near term, especially while the dollar is firm and Treasury yields remain elevated. Yet the same inflation shock forcing yields higher also reinforces the longer-term case for owning an asset outside the traditional monetary system.

Gold is currently paying the bill for tighter policy. The bull case is that it will eventually collect the insurance payout.

AI daily: China is pulling up a chair at the memory chip Oligopoly

The memory trade has been priced like a private dinner for three.

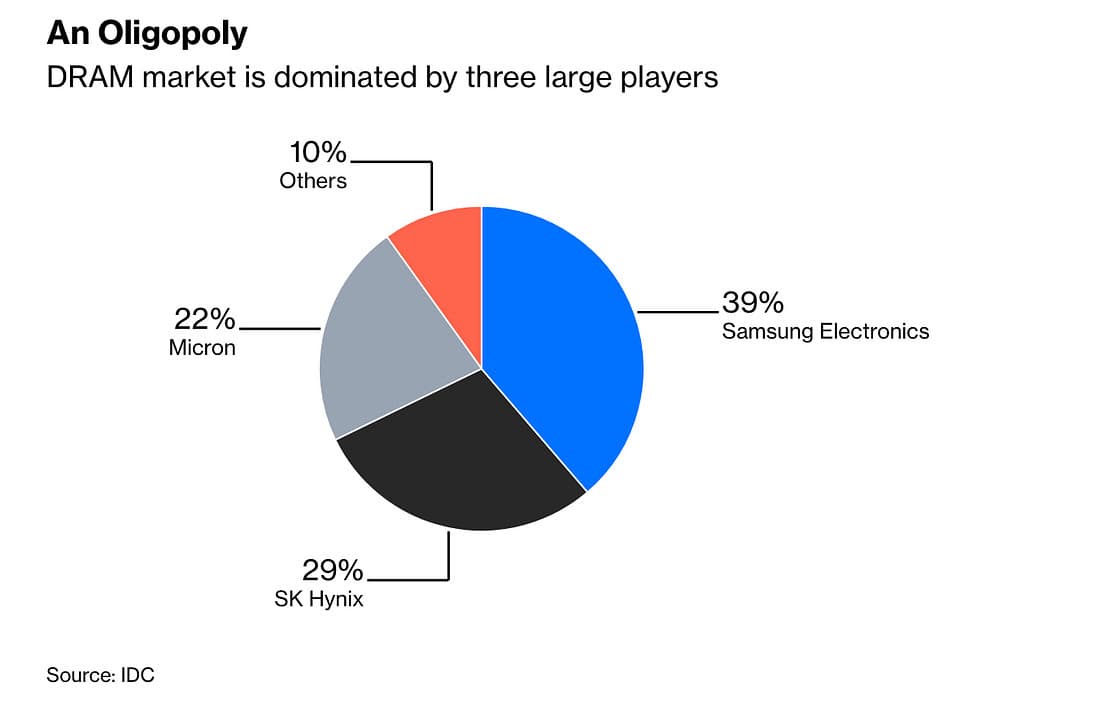

Samsung Electronics, SK Hynix and Micron control roughly 90% of the global DRAM market, while also owning the high-bandwidth memory chips feeding Nvidia’s AI engines. It is the kind of market structure investors dream about: three disciplined producers, booming demand, tight supply and nobody reckless enough to flood the room with unwanted capacity.

That arrangement has helped turn the AI memory boom into a profit feast. But China has now arrived at the door carrying a cheque for nearly $10 billion.

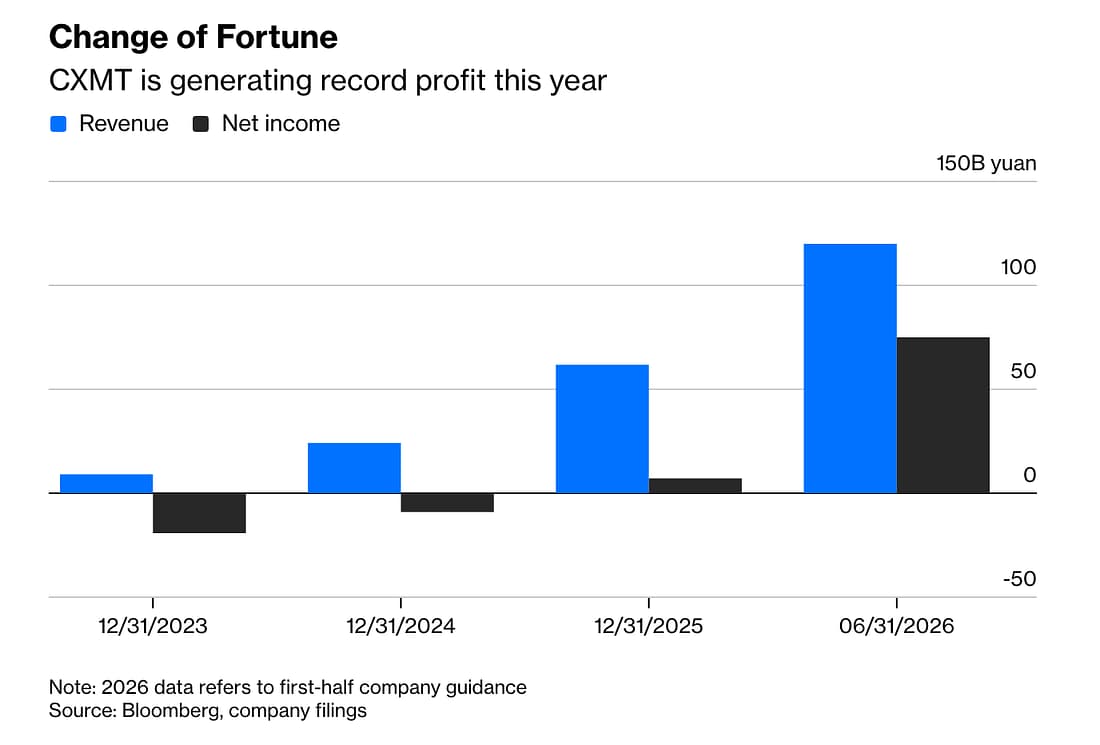

ChangXin Memory Technologies, better known as CXMT, is preparing a $9.8 billion Shanghai listing, giving China’s only serious DRAM challenger the firepower to expand production and begin leaning against an oligopoly that has grown comfortable collecting scarcity rents.

CXMT is not yet ready to storm the HBM castle. Its advanced-memory programme has reportedly reached the engineering stage, but building those chips commercially, with reliable yields and at meaningful scale, remains a much steeper climb. For now, Samsung, SK Hynix and Micron still control the most lucrative part of the AI memory chain.

But the first crack rarely appears through the front gate.

The more immediate threat is conventional DRAM, where CXMT can already mass-produce DDR5 chips. Its older and larger manufacturing nodes leave margins below those of the established producers, but China’s semiconductor playbook has never depended on winning the first round through profitability. It wins by building capacity, lowering prices and staying at the table longer than competitors expect.

Its market share has already doubled to roughly 8% over the past year. The company expects as much as 120 billion yuan in first-half revenue and 75 billion yuan in net income, a remarkable reversal for a business that was still bleeding red ink in mid-2025.

The IPO now gives CXMT enough dry powder to turn momentum into machinery. Production capacity is reportedly set to rise by around two-thirds by 2028, which is where the memory supercycle story starts hearing footsteps behind it.

HBM gets the champagne and headlines, but commodity DRAM still pays a large part of the bill at Samsung, SK Hynix and Micron. More importantly, conventional memory pricing has done much of the heavy lifting behind this year’s record profits. HBM is generally sold through longer-term agreements, keeping prices relatively stable. Standard DRAM trades closer to the market’s pulse, and shortages have sent prices sharply higher.

CXMT does not need to beat the big three in HBM to spoil the party. It only needs to loosen the conventional-memory shortage, reduce pricing power and give major customers another supplier to play against the incumbents.

Apple’s reported negotiations to buy chips from CXMT show how quickly that bargaining table could change. A fourth supplier does not need to become the market leader. It only needs to offer customers another chair, another quotation and another reason not to sign whatever contract is placed in front of them.

That is the danger for memory bulls. The current earnings boom rests on two pillars: AI demand and disciplined supply. Demand may remain strong, but discipline becomes harder to maintain when a state-backed competitor is raising billions to build through the cycle.

The big three are still eating well. But CXMT is walking into the kitchen, ordering more ovens and preparing to serve the next course at a lower price.

Tech supply chain daily: South Korea’s leveraged ETFs arrived just in time to catch the AI avalanche

South Korea’s retail traders bought tickets for the AI express just as the train began reversing out of the station.

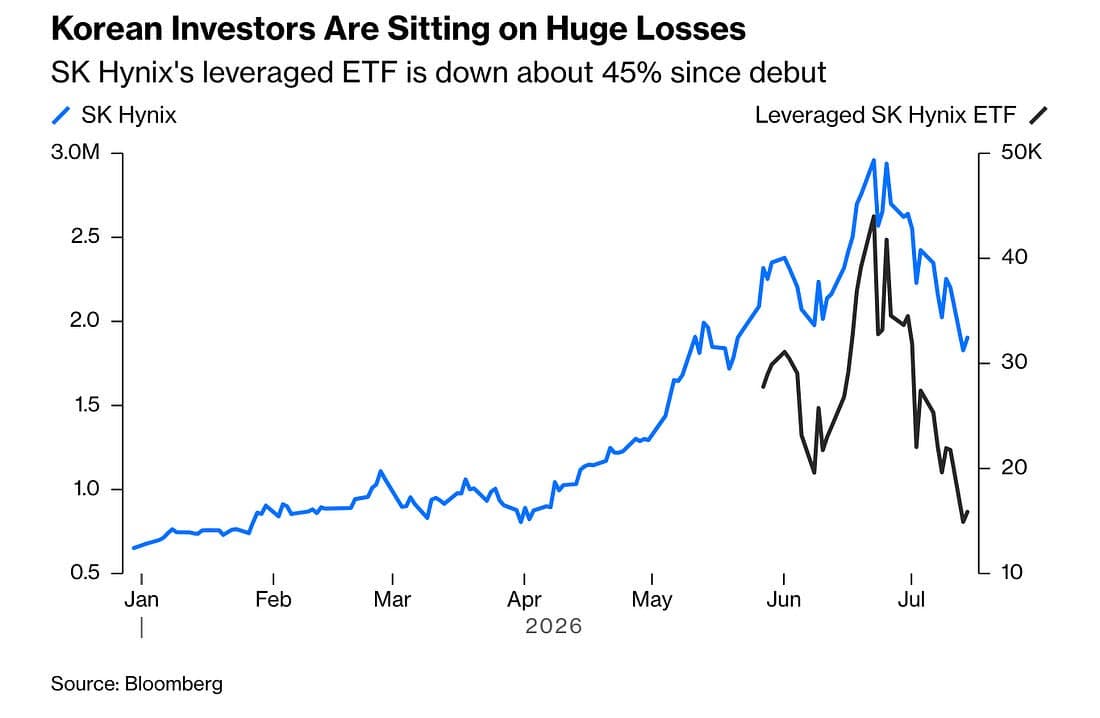

In late May, Seoul opened the gates to single-stock leveraged ETFs tied to SK Hynix and Samsung Electronics, giving local investors a shiny new way to double down on the country’s semiconductor champions. Demand arrived like dry grass meeting a match. Within a month, 16 products tracking the two chipmakers had attracted roughly $9.1 billion.

The problem was not the destination. It was the departure time.

By the time these products reached the platform, the Korean chip trade was already crowded, extended and carrying more momentum luggage than the market could comfortably lift. SK Hynix had become one of the clearest expressions of the AI memory boom, while South Korea had developed into one of the hottest equity markets on the planet. Brokerage deposits were swelling, retail participation was surging and investors were leaning across the table looking for more risk.

The regulator handed them a larger glass just as the punch bowl was being removed.

Since its launch, the largest SK Hynix-leveraged ETF has fallen more than 40%. That loss cannot be explained by the decline in the underlying shares alone. Leveraged ETFs are built to deliver a multiple of the stock’s daily return, not twice the return over weeks or months. When the market moves cleanly in one direction, the machinery can work beautifully. When prices begin bucking like a horse in a thunderstorm, daily rebalancing and volatility drag start eating through capital.

That is the trap. Investors are not merely betting on where the stock finishes. They are betting on the path it takes to get there.

A 2x ETF may look like a stock with a turbocharger bolted onto the bonnet, but beneath the hood it behaves more like an options strategy that is constantly resetting itself. In choppy markets, the fund is mechanically forced to add exposure after rallies and cut it after declines. It ends up buying higher, selling lower and paying a toll every time the market changes lanes.

Korean investors were taught how these instruments worked and required to complete a short examination before buying them. But completing an exam is not the same as understanding what happens when leverage, concentration and volatility are locked inside the same room.

The market structure makes the problem more dangerous. Even before the new ETFs arrived, trading in SK Hynix and Samsung accounted for roughly 31% of Korean equity turnover. By early July, the two stocks and their associated leveraged products represented close to 73%. That is no longer a side bet sitting quietly in the casino. It is a crowd jumping on the same floorboards.

The products may therefore be amplifying the very price swings hurting their owners. Falling chip shares force leveraged funds to reduce exposure, which adds further selling pressure, which creates more losses and another round of rebalancing. The tail begins wagging the semiconductor dog.

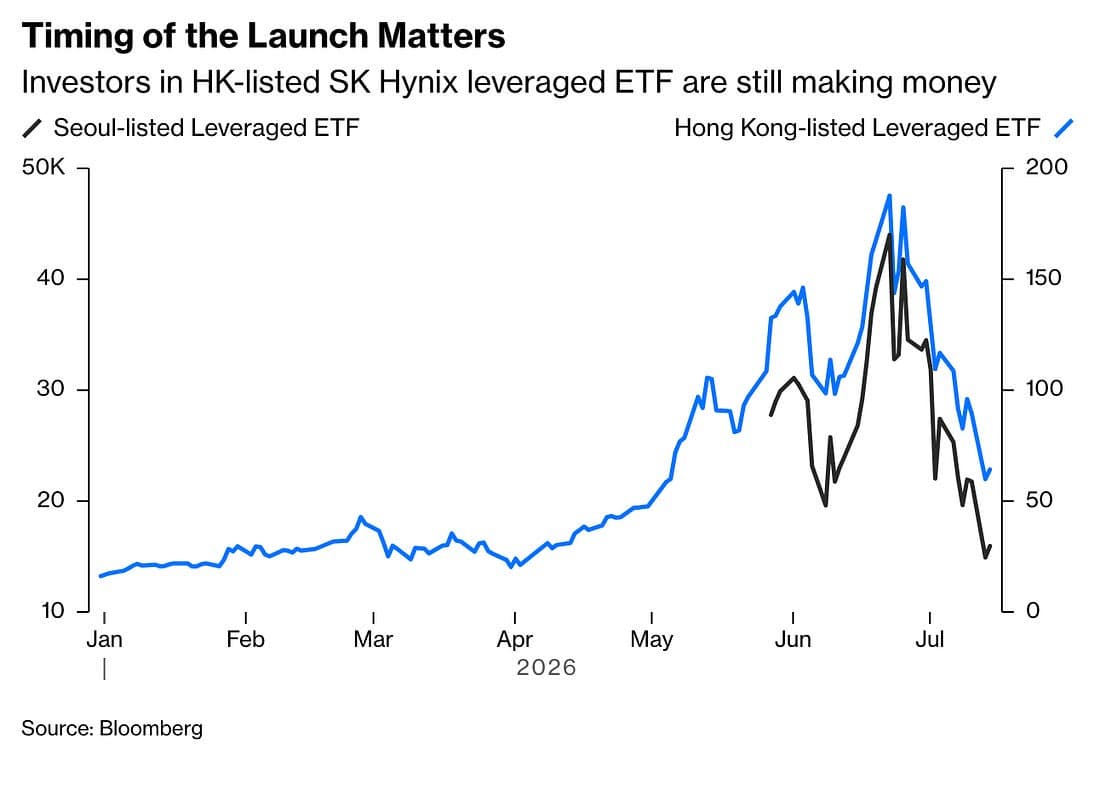

Hong Kong-listed investors tell the other side of the story. A leveraged SK Hynix product launched there last October remains sharply higher because it caught the climb before the mountain became crowded. South Korea’s products arrived near the summit and offered retail traders a faster route down.

Leverage did not create the semiconductor correction. But it gave the market a steeper staircase, removed the handrail and invited everyone to run.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.