Gold as a hedge against monetary policy failure

Historically, gold has been a very dynamic asset— it has been a medium of exchange, a safe haven, a store of wealth, and has performed well in both inflationary and deflationary environments. Over the past couple of years, I believe gold has been purchased as a hedge against monetary policy failure. It has been thirteen years since the Global Financial Crisis, and global central bankers are using the same exact tools today that they did in 2008, but to no avail. Quantitative Easing (QE), ZIRP (zero interest rate policy), and in some cases NIRP (negative interest rate policy) have proven to be ineffective tools in stimulating the economy. Since 2017-18, gold’s performance has proven to be a hedge against the failures of central bankers around the globe.

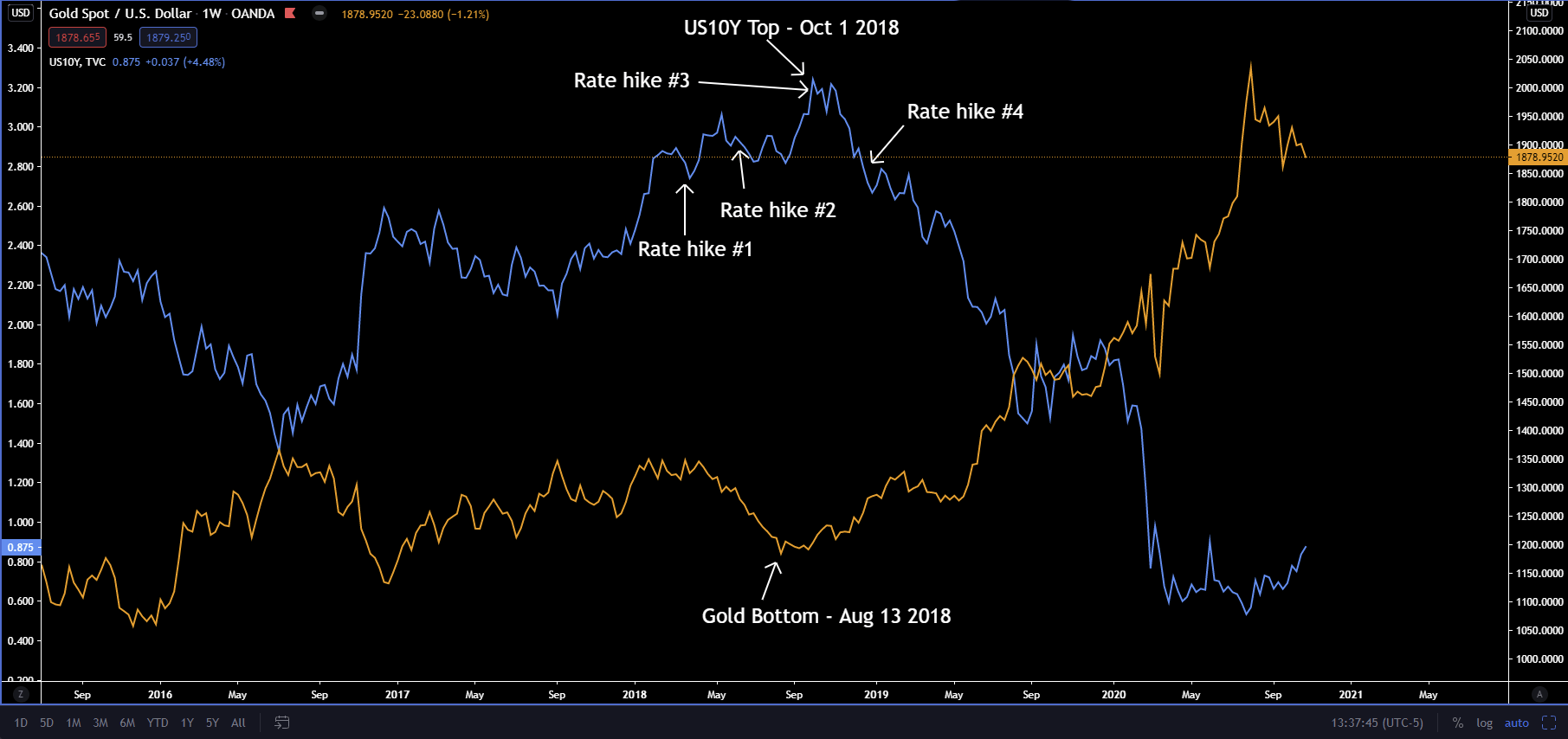

The last time we had any type of inflation hysteria was back in 2017-18. It was believed that the various rounds of QE over the years was finally stimulating the economy. Unemployment was near 4% for the entirety of 2017 and then dropped below 4% by the middle of 2018. The Fed considered this data to represent a “tight” labor market. Simultaneously, the labor force participation rate was quite low, indicating that the low unemployment rate was misleading. A “tight” labor market entails a low unemployment rate AND a high participation rate, but that wasn’t the case and hasn’t been since prior to the GFC. But, the Fed didn’t see it that way, which promoted them to raise interest rates four times in 2018, as they believed runaway inflation was on the horizon due to the “tightness” of the labor market. The market did not respond well to this, as the S&P 500 sold off 20% in Q4 of 2018. The Fed immediately put the brakes on any further rate hikes.

Let’s take a look (below) at what gold and the U.S. 10-year yield were doing around this time. If you look at the 10-year yield (blue line), you can see that it rose from about the middle of 2017 to the middle of 2018. This was the inflation hysteria period, when all the QE and low unemployment was going to lead to inflation. This inflation hysteria lasted a little over a year, which is not a long time considering QE had been utilized for several years prior. If you look at gold (orange line), it traded sideways during 2017, then fell off about 12% from March to August of 2018, before bottoming out. In other words, gold was NOT bought as a hedge against inflation. The bottom of gold was August 13, 2018— the top of the 10-year yield was October 1, 2018. The last two rate hikes by the Fed (in 2018) was September 27th and December 20th. The 10-year yield peaked just 4 days after the Fed raised the federal funds rate and started falling almost 3 months prior to the Fed’s last rate hike of the year. The bond market stopped trusting the inflation story as the Fed was still raising rates. Gold stopped believing in the story almost two months before the bond market did, and you could argue even before that as gold was never bought as a hedge during this period of inflation hysteria. Normally, investors buy gold as a hedge against inflation, but in 2018, once the market realized inflation and growth were never going to materialize, gold started getting bought as a hedge against 10 years of monetary policy failure.

Gold has a long history of being a medium of exchange and an asset that backs a monetary system. There are many gold “bugs” out there today that believe the global monetary system is headed back to another gold standard. I am not going to argue for or against this (although I think it’s unlikely), but the point is, as monetary policy continues to fail, gold becomes a viable alternative, hence the strong performance of gold the last couple of years. Notice (above) that gold traded sideways, then fell off during the inflation hysteria. Again, gold is a hedge against inflation and should have been bought during that time, but it wasn’t. It started to go up once the market realized monetary policy failed again, and was confirmed two months later when yields started to fall, amidst the Fed still raising rates.

Further stimulus is expected, post-election, which will be a positive for gold. Yes, there is more inflationary expectations from the mainstream, but as I wrote here, I believe it will be short lived.The more stimulus that is required, the more monetary policy is failing, which will send gold higher and higher. I won’t speculate, as there have been so many different figures thrown around regarding where the price of gold will be over the next few years. But, I will say that the regularly mentioned figure of $5,000 per ounce of gold does not seem far-fetched, by any stretch of the imagination.. Whether or not gold is involved in a new monetary system in the future is irrelevant to its price over the next few years, because as long as monetary policy continues to fail, without a replacement, gold will continue to see inflows of capital.

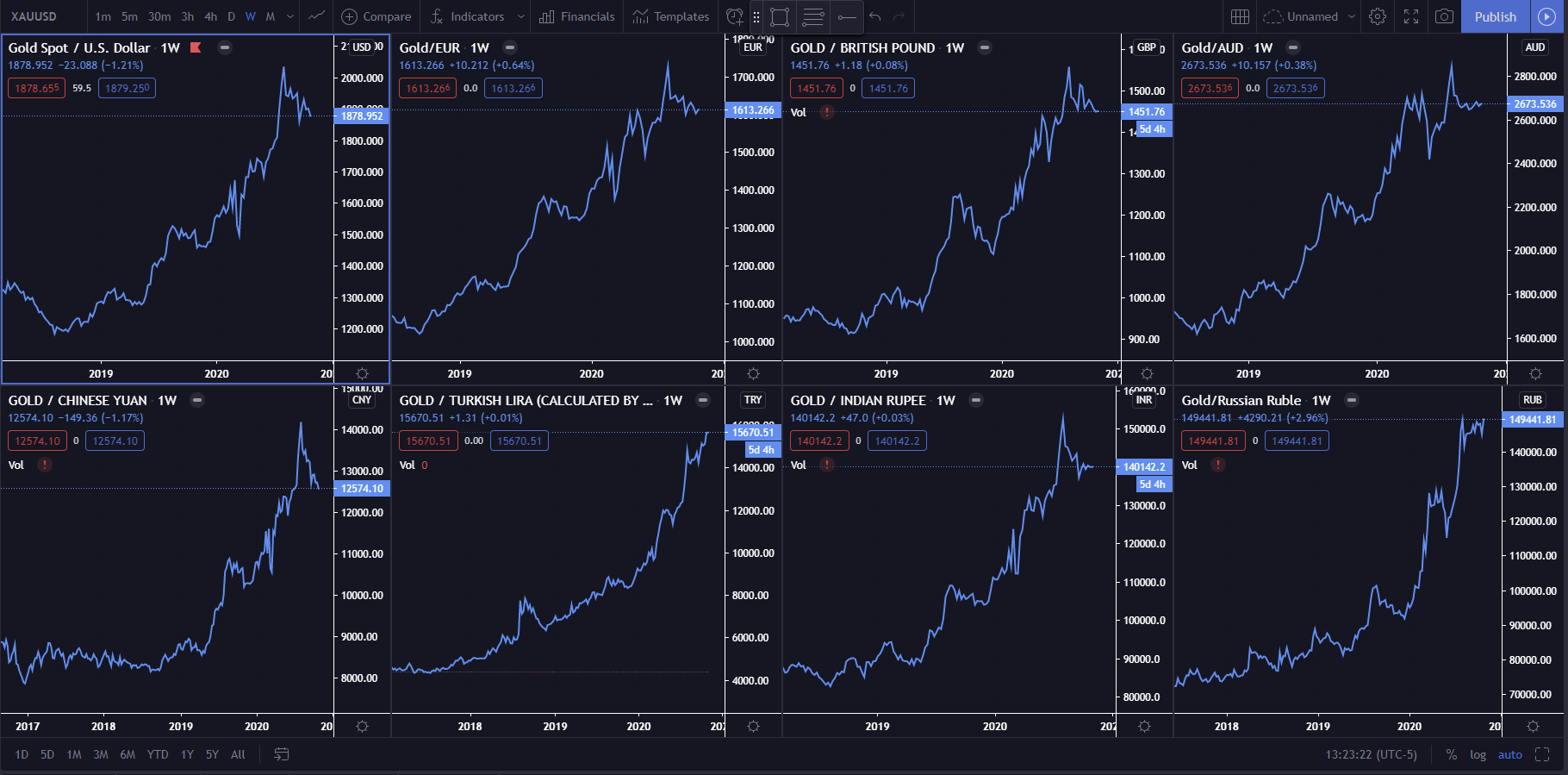

Failed monetary policy is not specific to the U.S. Central bankers around the world have been using the same tools, with no luck. Gold created a new all-time high back in August, in U.S. dollar terms. However, if you look below, gold has been creating new all-time highs against virtually every fiat currency across the globe. This tells me that monetary policy is failing on a global level. Globally, central bankers have all been “printing” money and lowering interest rates. It has proved ineffective in its efforts to stimulate economic growth over the last thirteen years. Yet, central bankers continue to go back to the same well.

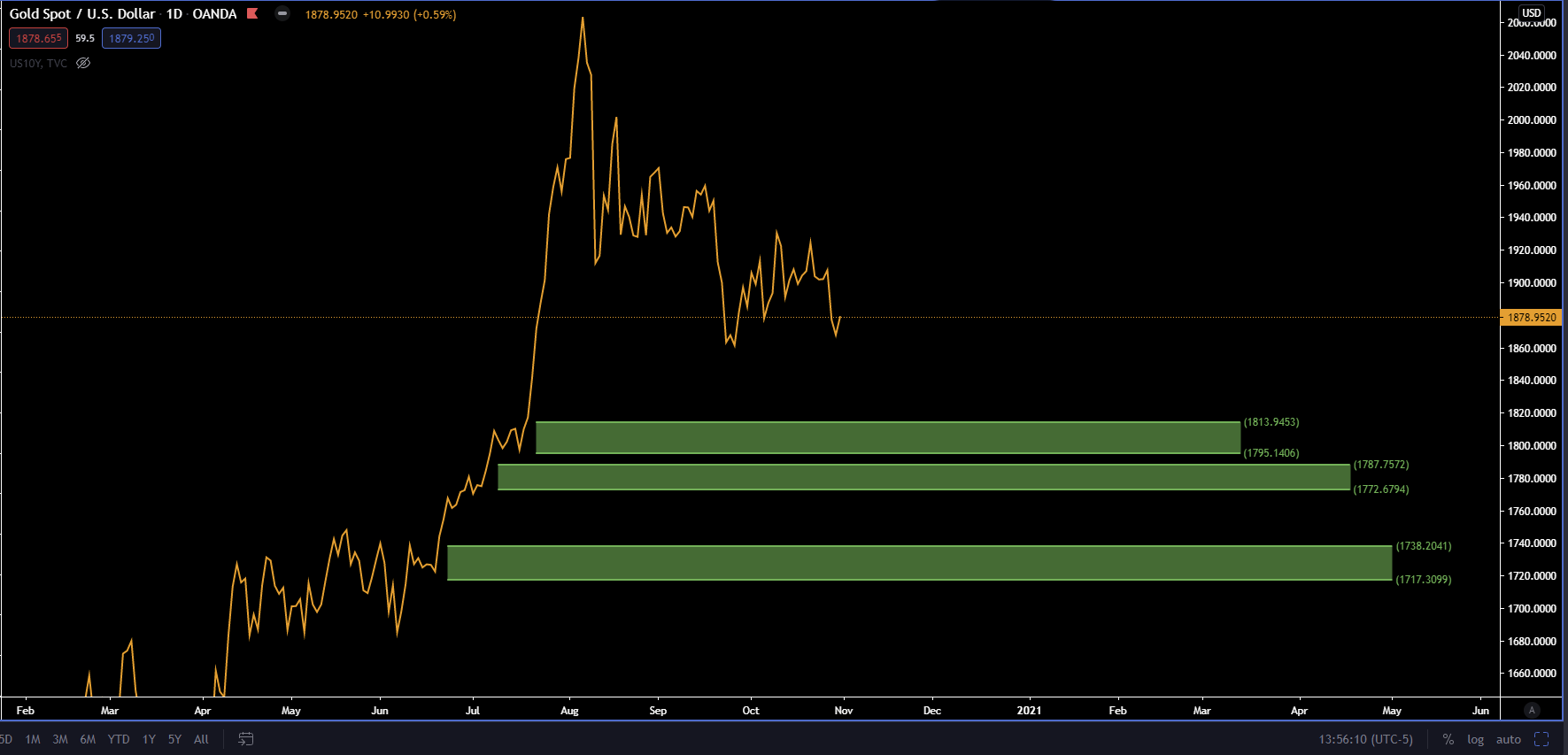

I have said it before and I will say it again, I am expecting over the next several months another selloff in risk assets similar to the event we saw in March of this year. The cause of this, I presume, will be further household and business insolvencies, once payments that were deferred back in the early pandemic months start coming due. Similar to March, I think we will see a correction in gold again. Investors will sell gold, not because they will want to, but because they will have to in order to obtain dollars to service their debt payments and margin calls. This will create a great buying opportunity in gold, before its next leg up in creating new all-time highs. I have drawn out some demand levels (below) to look out for. Just keep in mind with more stimulus on the horizon and inflation hysteria picking up again, gold could consolidate for a period of time and/or pullback further, similar to what it did in 2017-18 before rallying.

Author

Ryan Miller

Ryan Miller Trading Economics

Ryan Miller received a Bachelors Degree in History from William Paterson University. Through his studies of U.S. history, he developed an interest in the implications the financial markets have on the economy.