Global stock markets start the year at or near all-time highs

-

FTSE and sterling rally in first genuine post-Brexit trading day.

-

Entain shares surge on MGM offer.

-

Markets eye big week with Georgia Senate runoffs.

Global stock markets enter 2021 at or near all-time highs despite ongoing uncertainty around the pace of recovery from the pandemic and the threat of fresh lockdowns lasting well into the spring. Despite the anxiety around when we get back to normal, the major fears of last year have receded and liquidity remains strong. Asian markets ex-Japan rose to new all-time highs, with Tokyo finishing the day off 0.7% due to concerns about tougher coronavirus restrictions in the capital and surrounding areas. European stocks got the new year trading session off to a solid start, with the DAX up 0.5% and Stoxx 50 rising 0.25%.

The FTSE 100 had ended 2020 on a bit of a sour note, but is much firmer this morning with the index +2% and well bid above the 6,500 mark and bulls eyeing the recent highs close to 6,700. There is a general risk-on mood and vaccine positivity could be a factor - the UK approved the use of the Oxford University/Astra Zeneca vaccine, with half a million doses ready today. It will allow a faster easing of restrictions, but the country looks likely to endure tougher restrictions in the meantime. We could also say that the lack of chaos/Armageddon/doomsday from Brexit is also a factor. Indeed after a fairly muted response in the FX markets to news of the deal on Christmas Eve, following the UK’s leaving the EU properly on Hogmanay, sterling has headed higher. GBPUSD advanced to its highest in almost three years above 1.37 amid broad dollar softness. We could not see sterling slowly grind its way to 1.40 as long as the economy can recover from the pandemic quickly enough to stop the BoE doing any further damage by taking rates negative.

Entain shares popped on news MGM Resorts International made a bid for the company. The offer of 1,383p per Entain share represents a premium of 22% based on the Dec 31st closing price, but the board say the proposal ‘significantly undervalues the company and its prospects’. The market thinks MGM (or another) will be good for more – shares rose 27% at 1,440p. We knew the opening up of the US gaming market would be good news for UK firms with interests there and so it is proving. And it should be said the yanks would certainly prefer the Brits to stay off their turf. We should also note that good global businesses trading with a UK-listed discount to the share price remain attractive to foreign groups hungry for growth. Clarity around Brexit at long last may see more bids of this nature emerge.

Talking of UK discounts, Ferguson is heading in the other direction and selling its Wolseley UK division for £308m to private equity group Clayton, Dublier & Rice. CEO Kevin Murphy says the move ‘further simplifies the group and allows us to focus entirely on investing in and developing our business across North America where we have the greatest opportunities for profitable growth’. True, and could it also now allow it to make the move to America it so desperately wants?

US stocks wrapped up 2020 on a high, with the Dow Jones and S&P 500 up 0.65% to new all-time peaks last Thursday. Futures are pointing to a firmer open today around the 30,700 and 3,770 areas respectively. The New York Stock Exchange will delist three Chinese telecos because of links to China’s military. China Telecom, China Mobile and China Unicom Hong Kong will be delisted in New York this month, but they all retain listings in Hong Kong.

Tesla reported strong Q4 delivery numbers, taking the annual print to half a million as it benefitted from the initiation of Model Y production in China. The company delivered 180,570 vehicles in the fourth quarter, beating expectations for around 174k. New US and German plants set to open this year will enable it to significantly raise production in 2021 and beyond.

Data this week includes the Fed’s meeting minutes, PMIs and a nonfarm payrolls report on Friday. Labor Department figures last Thursday showed initial jobless claims declined by 19,000 to 787,000 in the week ended Dec 26th, which was better than expected. Continuing claims fell 103k to 5.2m, whilst the number of people receiving benefits across all programmes fell by 800k to 19.6m.

Tomorrow’s Georgia runoff elections for the two Senate seats will be crucial – if the Democrats take both they would end the GOP majority and with a 50/50 split the deciding vote would sit with VP Harris. This is high stakes stuff – if the GOP can hold one they can block the Biden agenda. But if they fail it opens up the likelihood of some of the more progressive tax and spend policies becoming reality.

Oil prices rose ahead of the OPEC+ meeting, the first of new monthly ministerial discussions between the cartel’s members and allies led by Russia on how to proceed with production curbs initiated last year. In December, OPEC+ agreed to limit a tapering of output cuts to just 500k bpd in January and decided on monthly meetings to decide on output for the following month. Prices for Brent have stabilised around the $50 level following the vaccine news in November last year, whilst market intervention by OPEC and allies is clearly having some influence. Bulls will be looking for OPEC and co to signal they are not in a rush to raise production in February, which could be premature.

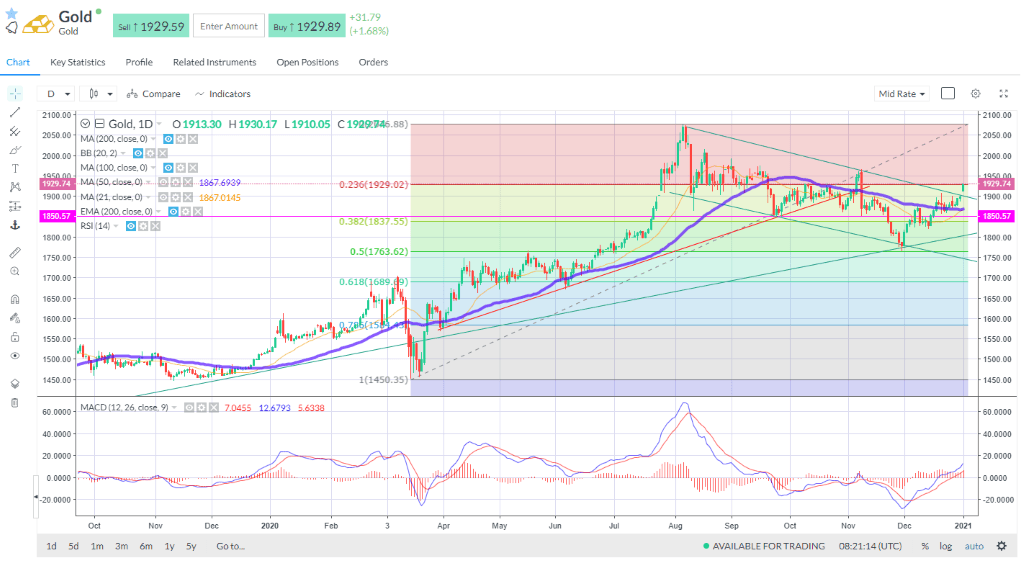

Gold appears to have made a decisive move higher with a breach of the top of the channel and its 50-day simple moving average with a bullish crossover by the 21-day line showing good upside momentum. Resistance seen at the 23.6% Fib level at $1,929. Declining US real rates (10yr TIPS back to -1.06%) and a weaker dollar are conspiring to create the conditions for another bump higher for gold.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.