Global macro transmission monitor – Week ending June 5, 2026

How macro shocks propagated through FX, commodities and rates last week.

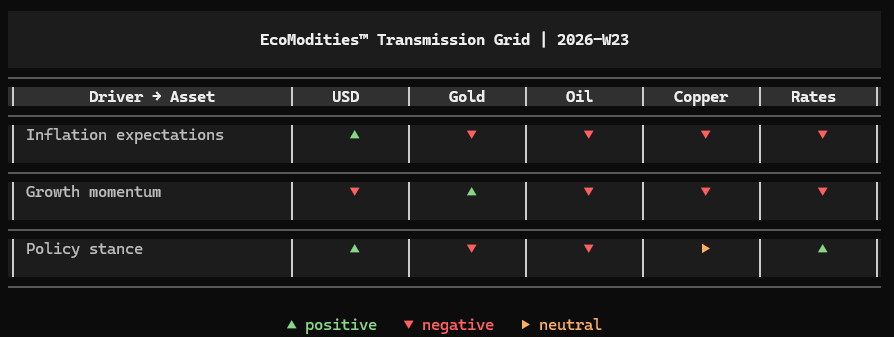

Executive transmission map

Growth data dominated the macro transmission chain last week as US activity indicators and labor-market data continued signaling resilience despite ongoing concerns around global growth momentum. ISM Manufacturing and Services both surprised to the upside, while US employment data remained broadly stable, reinforcing confidence in the underlying strength of the US economy.

The result was renewed support for the USD and rates markets, limiting upside participation across gold and commodities. At the same time, softer growth signals from Australia contrasted with stronger North American labor data, creating regional divergence across the broader macro landscape.

Policy transmission remained relatively contained as central-bank communication reinforced existing market expectations rather than generating significant repricing. Cross-asset alignment improved around the growth narrative, with markets increasingly reflecting US economic resilience rather than disinflation or policy easing.

1. Macro shock layer

A. Inflation shock

What moved

No major inflation release dominated the week. Markets instead continued interpreting previous inflation trends through the lens of stronger economic activity and labor-market resilience.

Why it matters

The absence of significant downside inflation surprises allowed markets to maintain expectations that policy easing will remain gradual and data dependent.

Transmission path

- USD retained support through inflation stability.

- Gold faced headwinds from firm macro conditions.

- Oil and industrial commodities struggled to attract fresh inflation-driven flows.

- Rates remained relatively firm.

FX transmission

USD remained supported against major currencies as inflation expectations stabilized and growth remained the dominant macro driver.

B. Growth shock

What moved

US economic data broadly exceeded expectations while Australian growth disappointed.

- ISM Manufacturing PMI: 54.0 vs 53.3 expected.

- ISM Services PMI: 54.5 vs 53.7 expected.

- ADP Employment Change: 122K vs 118K expected.

- Non-Farm Payrolls: 172K vs 85K expected.

- Australia GDP q/q: 0.3% vs 0.5% expected.

Why it matters

The data reinforced the narrative that the US economy continues expanding at a healthy pace despite tighter financial conditions. Markets interpreted the releases as evidence that recession concerns remain premature.

Transmission path

- USD strengthened through relative growth leadership.

- Gold lost defensive support.

- Oil and copper faced pressure from stronger dollar conditions.

- Rates repricing shifted modestly higher.

FX transmission

USD outperformed across major currency pairs, while AUD weakened following softer domestic growth data. Commodity-linked currencies struggled to match the strength of the US macro backdrop.

C. Policy shock

What moved

Central-bank communication from the BOE, BOJ and RBA generated limited market repricing, while policymakers largely maintained existing guidance.

Why it matters

Markets interpreted policy communication as confirmation that monetary authorities remain cautious and heavily dependent on incoming economic data.

Transmission path

- USD retained policy support.

- Gold remained pressured by stable policy expectations.

- Oil remained sensitive primarily to growth and positioning factors.

- Rates remained supported by resilient macro data.

FX transmission

Major FX pairs continued trading around relative growth and rate differentials rather than fresh policy surprises.

2. Cross-asset transmission grid – 2026-W23

3. Market alignment check

Cross-asset alignment strengthened during the week around the US growth narrative.

Manufacturing activity, services activity and labor-market data all pointed toward continued economic resilience, supporting USD and rates markets while limiting participation across gold and commodities.

The growth layer remains the dominant macro force, while inflation and policy transmission continue acting as secondary confirmation mechanisms rather than primary market drivers.

4. Forward pressure points

USD

Pressure remains centered on whether incoming growth data continue validating US economic resilience.

Gold

Gold remains highly sensitive to real-yield dynamics and the persistence of stronger-than-expected economic activity.

Oil

Oil remains vulnerable to USD strength and shifting demand expectations despite stable underlying fundamentals.

Copper

Copper continues balancing industrial demand expectations against tighter financial conditions.

Rates

Rates markets remain vulnerable to additional upside surprises in growth and employment data.

One-line takeaway

The macro transmission chain shifted decisively toward growth resilience last week, with stronger US activity and labor-market data supporting the USD and rates while limiting participation across gold and commodity markets.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.