Global macro transmission monitor – Week ending July 10, 2026

Executive transmission map

The macro transmission chain remained centered on policy stability and resilient growth last week as markets navigated the release of the FOMC Minutes alongside generally constructive labor-market data from Canada.

Inflation remained a secondary driver, allowing policy expectations and relative economic resilience to shape cross-asset pricing. The USD retained broad support, while gold struggled to attract sustained defensive flows. Oil and copper continued benefiting from stable growth expectations despite softer US services activity.

Cross-asset alignment remained strong, with inflation, growth and policy signals broadly reinforcing the existing market regime rather than generating a meaningful repricing.

1. Macro shock layer

A. Inflation shock

What moved

No major inflation releases dominated the week, allowing markets to focus primarily on policy communication and labor-market conditions.

Inflation expectations remained relatively stable, maintaining support for the USD and limiting upside participation across precious metals.

Why it matters

The absence of significant inflation surprises reinforced the market view that future policy decisions will depend increasingly on growth and employment rather than price dynamics alone.

Transmission path

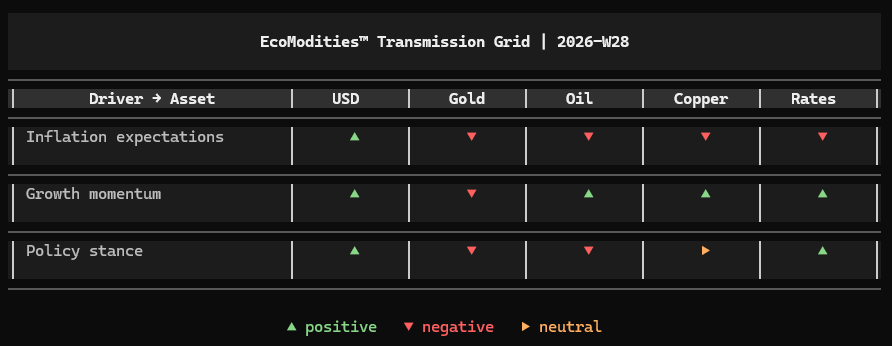

- USD retained inflation-related support

- Gold remained under pressure

- Oil and copper traded within stable macro conditions

- Rates pricing changed only modestly

FX transmission

The dollar continued benefiting from stable inflation expectations while major currency pairs traded inside relatively contained macro ranges.

B. Growth shock

What moved

Growth signals remained constructive despite a modest slowdown in US services activity.

- ISM Services PMI: 54.0 vs 54.2 expected

- Previous: 54.5

- Canada Employment Change: 18.2K vs 11.2K expected

- Canada Unemployment Rate: 6.5% vs 6.6% expected

Why it matters

Canadian labor data reinforced the resilience of North American economic activity, offsetting the modest moderation in US services momentum.

Transmission path

- USD remained supported through relative growth resilience

- Oil benefited from constructive demand expectations

- Copper remained supported by industrial activity

- Gold continued facing reduced defensive demand

- Rates remained firm

FX transmission

The Canadian dollar strengthened following stronger labor-market data, while broader FX positioning continued favoring currencies supported by resilient domestic fundamentals.

C. Policy shock

What moved

The FOMC Minutes broadly confirmed the Federal Reserve's cautious and data-dependent policy approach.

The Reserve Bank of New Zealand maintained the Official Cash Rate at 2.50%, as expected.

Why it matters

Markets interpreted the Minutes as confirmation that policy easing will remain gradual, reinforcing existing expectations without triggering a meaningful repricing across asset classes.

Transmission path

- USD retained policy support

- Gold remained pressured

- Oil remained broadly neutral

- Copper stayed neutral to policy developments

- Rates remained supported

FX transmission

Policy differentials continued supporting the USD as central-bank communication remained broadly consistent with existing market expectations.

2. Cross-asset transmission grid | 2026-W28

3. Market alignment check

Cross-asset alignment remained consistent during the week.

Stable inflation expectations, resilient North American labor markets and a largely unchanged policy outlook continued supporting the USD and rates. Gold remained constrained by limited demand for defensive positioning, while oil and copper reflected continued confidence in underlying growth conditions.

The macro chain remains primarily driven by policy stability and resilient growth rather than by inflation repricing.

4. Forward pressure points

USD

Pressure remains concentrated around labor-market resilience and evolving Fed policy expectations.

Gold

Gold remains highly sensitive to real yields and any change in policy expectations.

Oil

Oil continues balancing resilient demand expectations against financial conditions.

Copper

Copper remains dependent on industrial demand and manufacturing activity.

Rates

Rates markets remain vulnerable to shifts in Fed communication and labor-market data.

One-line takeaway

The macro transmission chain remained stable last week, with resilient growth and consistent policy expectations continuing to support the USD and rates while limiting defensive participation across gold.

Author

Luca Mattei

LM Trading & Development

Luca Mattei is a market analyst focusing on FX, metals, and macroeconomic trends. He develops trading tools for retail and professional traders, coding indicators and EAs for MT4/MT5 and strategies in Pine Script for TradingView.