France, youth employment: On the verge of a more pronounced downturn?

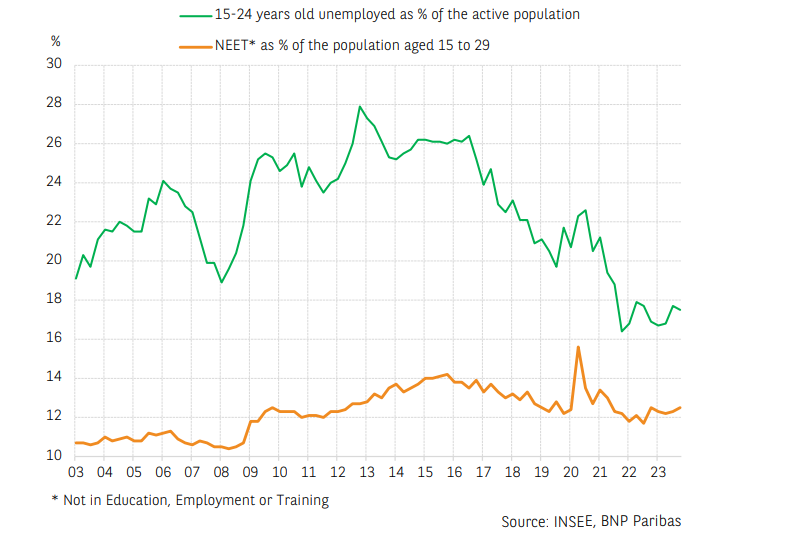

After the youth unemployment rate (15-24 years old) hit its lowest level for more than 30 years at the end of 2021, standing at 16.4% of the working population, it has risen slightly since then, with a figure of 17.5% in Q4 2023 (compared to 16.7% in Q1 2023). Despite being almost 3 points above the Eurozone average, this rate is still substantially lower than the 2019 one (20.8%).

This improvement since 2019 has been driven by two factors, which are now on the wane:

-

Nearly 1 million young people were on an apprenticeship in 2023, compared to less than 500,000 in 2019, which also boosted the employment rate of 15-24 years old (35.3% in Q4 2023 compared to 29.8% at the end of 2019). However, the number of apprentices only increased by 5% in 2023, suggesting that it is starting to plateau;

-

The shortage of available labour, with an unemployment rate of the 25-49 years old hitting an unprecedented low in Q1 2023 since 2008 (excluding the Covid period) at 6.4%, helped to increase employment among younger workers. However, the unemployment rate of 25-49 years old began to rise to 7% at the end of 2023, which is expected to continue in 2024 and could bring an increase in the youth unemployment rate with it.

Most notably, these improvements have done nothing to alter the percentage of young people not in education, employment or training (NEET). At the end of 2023, it remained close to its 2019 average, standing at 12.5% of the total population aged 15-29 years old, after increasing during the 2008 crisis and never coming back down again. This amount is also almost 4 points higher than the rate in Germany (8.6% in 2022). Therefore, while apprenticeships have helped to move young trainees towards more professional qualifications, they have seemingly only had a marginal impact on the proportion of NEETs (i.e. the individuals who struggle the most in finding a job), suggesting that other measures need to be identified in order to reduce this phenomenon.

The difficulty in accessing housing could be an additional factor further hindering young people’s entry into the labour market. It could indeed become even more acute, against the backdrop of a significant downturn in new construction (only 299,500 housing starts in 2023, the lowest figure since 1997) and a relative drop in transactions on existing homes which could shrink the rental market (transactions on existing homes have almost been 3 times higher than housing starts since 2016, compared to a ratio of 1 to 2 previously). Yet, difficulty in accessing housing is among the major barriers to young people’s entry into the labour market.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.