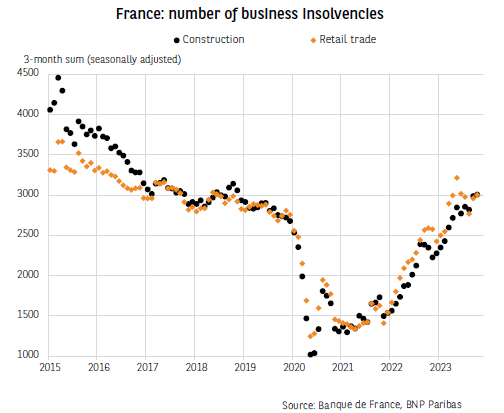

France: Insolvencies in the construction sector catch up with those in retail trade

Business insolvencies continued to rise in October and are now 10% higher than their pre-COVID level (2019 figures) in cumulative terms over the last three months, according to data from Banque de France.

This rise has been accelerating in retail trade since the start of 2022, as this sector has been one of the hardest hit (along with the accommodation and catering sector) by the inflationary shock due to rising production costs and falling household demand. The total three-month business insolvencies in the retail trade sector was even higher at the end of May than at the end of October. This decrease in business insolvencies, although moderate, is mirroring with some delay the disinflation path: after peaking at 7.3% y/y in February, inflation now only stands at 3.8% in November (harmonised index), a fall that gained momentum recently (inflation was still 5.7% y/y in September).

However, the construction insolvencies curve has continued to grow, and the sector’s figures have caught up with retail trade insolvencies. A number of factors are fuelling this rise:

- Higher interest rates: although the ECB raised its key rate for the last time in September, this hike is not expected to be completely passed on to domestic interest rates until the start of 2024;

- Reduced activity in the sector: in October 2023, the 12-month cumulative figure for housing starts was 23% down from its January 2022 peak. The outlook for construction starts is at an all-time low (the balance of opinion in the INSEE real estate developers survey stood at -40 in October);

- The deterioration (albeit relative) in payment behaviour: 34.6% of companies reported late payments in the second half of the year (compared to 28.7% in the first half) and cash-flow difficulties (the balance of opinion was -11.1 in October, compared to -7.2 in July according to INSEE’s construction sector survey).

The insolvencies curves for the retail trade and construction sectors could intersect more noticeably. The inflationary shock is expected to continue easing, while the negative shock on construction activity could continue until 2025. This is reflected in our growth scenario: whereas household consumption is expected to recover in 2024 (standing at 1.2%, following on from 0.7% in 2023), household investment is likely to continue dropping (standing at -3.7% in 2024, following on from -4.9% in 2023).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.