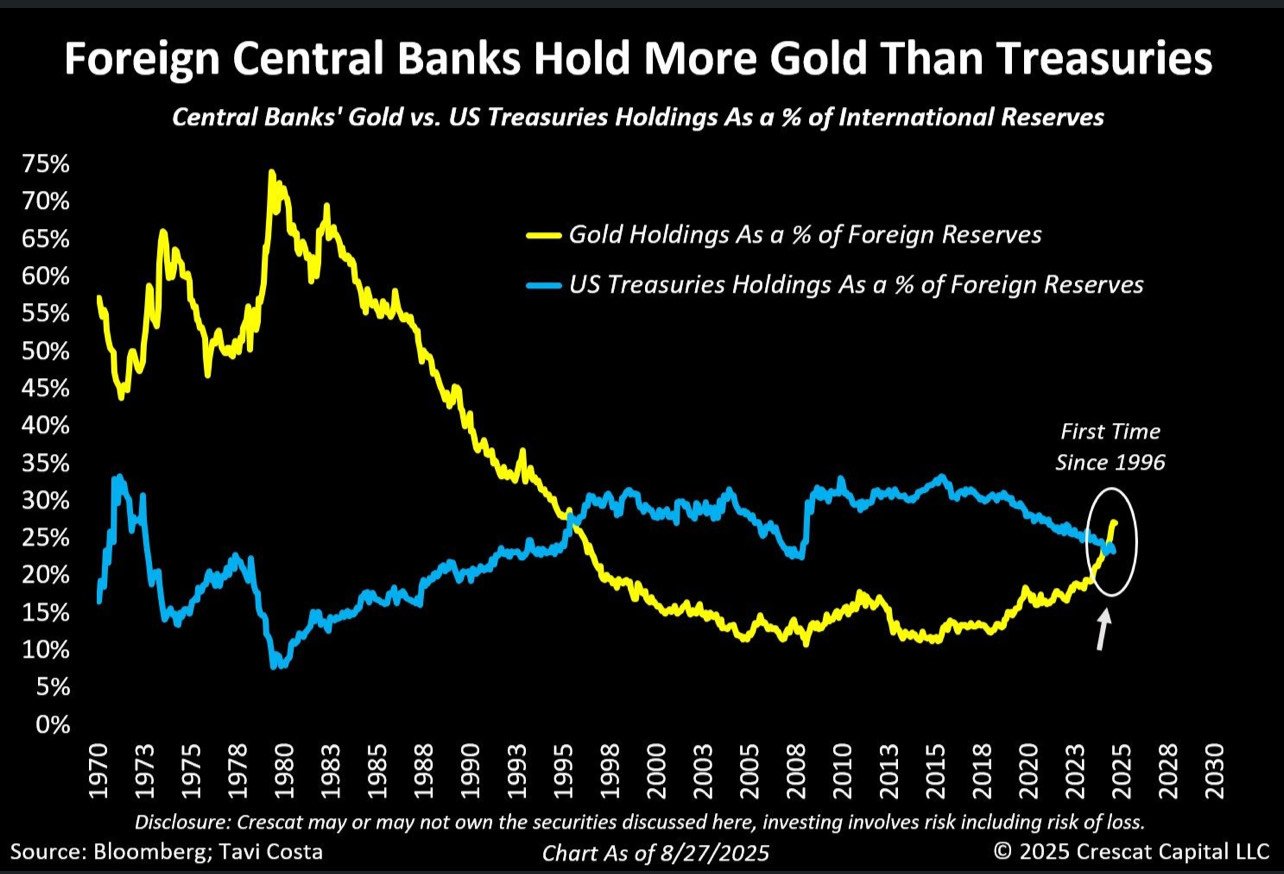

For first time in nearly 30 years, foreign central banks hold more Gold than U.S. treasuries

For the first time since 1996, foreign central banks hold more gold than U.S. Treasuries as the world continues to de-dollarize.

Crescat Capital macro strategist Tavi Costa highlighted the crossover moment in a post on X, saying it is “likely the beginning of the most significant global rebalancings we've experienced in recent history.”

Central banks have been aggressively adding gold to their reserves over the last three years.

Last year was the third-largest expansion of central bank gold reserves on record, coming in just 6.2 tonnes lower than in 2023 and 91 tonnes lower than the all-time high set in 2022. (1,136 tonnes). 2022 was the highest level of net purchases on record, dating back to 1950, including since the suspension of dollar convertibility into gold in 1971.

To put that into context, central bank gold reserves increased by an average of just 473 tonnes annually between 2010 and 2021.

At the same time, dollar reserves have been falling. As of the end of last year, dollars made up 57.8 percent of global reserves. That is the lowest level since 1994, representing a 7.3 percent decline over the last decade. In 2002, dollars accounted for about 72 percent of total reserves.

A recent JPMorgan note said this reveals the waning dependence on the U.S. dollar in trade that is being reflected in the gold market.

“The main de-dollarization trend in FX reserves, however, pertains to the growing demand for gold. … This increased demand has in turn partly driven the current bull market in gold, with prices forecast to climb toward $4,000/oz by mid-2026.”

On the other side of the coin, there is sagging demand for U.S. Treasuries.

Why de-dollarization?

Why are so many countries spurning the dollar?

Many are concerned about the weaponization of the U.S. currency. In an article published by the Atlantic Council, Kimberly Donovan and Maia Nikoladze point out that “central banks that are worried about getting sanctioned, want to protect themselves from a potential global financial crisis, or both have been stacking up gold at record levels.”

There are also growing worries about the U.S. government’s fiscal irresponsibility. Earlier this month, the national debt pushed above $37 trillion, and there is no sign that the borrowing and spending will slow down any time soon.

Earlier this year, analyst Artis Shepherd called the sagging demand for U.S. Treasuries “red lights blinking.”

“The bond market is sending a message to the U.S. government that its spending is out of control and the reserve currency ‘privilege’ it has abused for the last 80 years is running out.”

Ramifications

The dollar isn’t in danger of collapsing or even losing its reserve status – at least not yet. However, even a modest de-dollarization spells trouble for the federal government and the U.S. economy.

In a nutshell, the United States needs the world to need dollars.

The U.S. depends on this global demand for dollars supported by its reserve status to underpin its massive government. The only reason Uncle Sam can borrow, spend, and run massive budget deficits to the extent that it does is the dollar’s role as the world's reserve currency. It creates a built-in global demand for dollars and dollar-denominated assets. This absorbs the Federal Reserve’s money creation and helps maintain dollar strength despite the Federal Reserve’s inflationary policies.

WolfStreet summed up the risk the U.S. faces as the dollar’s status continues to erode.

“The status of the U.S. dollar as the dominant global reserve currency has helped the U.S. fund its twin deficits and thereby has enabled them: the huge fiscal deficit every year and the massive trade deficit every year. The reserve currency status comes from other central banks (not the Fed) having purchased trillions of USD-denominated assets such as Treasury securities, other government securities, corporate bonds, and even stocks. The dollar's status as the dominant reserve currency has been crucial for the U.S., and as that dominance declines ever so slowly, risks pile up ever so slowly.”

While the threat isn’t immediate, a slowly growing pile eventually turns into a giant pile.

But again, even a modest de-dollarization will have significant impacts. If the world needs fewer dollars, they will begin to return to the U.S., causing a dollar glut. This will increase inflationary pressure domestically as the value of the U.S. currency further depreciates. In the worst-case scenario, the dollar could collapse completely, leading to hyperinflation.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Mike Maharrey

Money Metals Exchange

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.