Five Fundamentals for the Week: US inflation, UK bond rout and Donald Trump set to rock markets

- Investors fear a bump up in inflation after robust employment data

- Britain's on-edge bond market will be tested by the United Kingdom's inflation report.

- Comments from President-elect Donald Trump may stir markets ahead of his inauguration next week.

Are British bonds the "canary in the coal mine?" The sell-off in the UK bond market and potentially higher interest rates in the US put investors on edge. Several critical releases – and comments from President-elect Donald Trump – are set to cause high volatility.

1) Trump tariff talk may sway markets

President-elect Donald Trump enters the White House on January 20, but his comments have been rattling markets for long weeks. At the time of writing, Trump has been focused on the fires in Los Angeles, criticizing local officials. For markets, his focus on bashing political rivals is a relief – he is not talking about the economy.

Previously, Trump and his team threatened Mexico and Canada with high tariffs, disrupting the trade agreement signed during his previous tenure. Will he shift to China now that the Asian giant reported record exports?

Any threats of tariffs or other measures would hit markets and boost the US Dollar (USD), while calmer tones would support Stocks and weigh on the safe-haven Greenback.

There is a difference between Trump's comments and those of his circle. His remarks carry more weight than theirs.

2) US PPI serves as a warm-up ahead of the CPI

Tuesday, 13:30 GMT. The Federal Reserve (Fed) was supposed to focus on the labor market rather than inflation, but prices have been on the rise once again. The hawkish shift in the bank's approach came due to a bump up in price rises. Now, prices at factor gates also matter, especially as these are released ahead of consumer prices.

The Producer Price Index (PPI) rose by 0.4% MoM in November, while the core PPI advanced by a more modest 0.2%. Similar figures are on the cards for the December report. Weaker figures would boost Stocks and Gold, while elevated numbers would boost the US Dollar.

It is critical to note that the PPI and Wednesday's Consumer Price Index (CPI) are only loosely correlated. Thus, a surprise in one direction for the PPI does not mean that the CPI in the same month will follow its path. Nevertheless, markets are set to respond sharply.

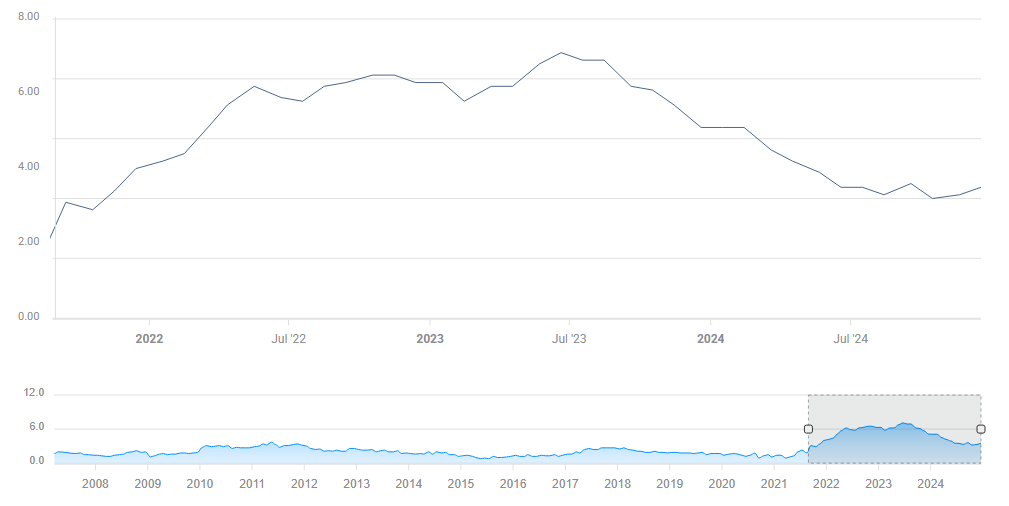

3) UK CPI is closely watched by the Bank of England and global markets

Wednesday, 7:00 GMT. UK bonds have suffered a sell-off without any immediate trigger. UK Chancellor of the Exchequer Rachel Reeves presented her budget in late October and the Bank of England (BoE) has been steady at the wheel. Nevertheless, fears of unsustainable debt have hit the UK, and unfavorable comparisons between the current Labour government and the Conservative one led by Lizz Truss have emerged. That may spread to other markets.

The BoE may be forced to keep interest rates higher to boost the falling British Pound (GBP) and fight stubborn core inflation. Elevated borrowing costs would add to pressure on the central bank and also on bond markets.

UK ore CPI. Source: FXStreet

Britain's Consumer Price Index (CPI) report serves as a test of inflation. Due to the fragility of bond markets, the reaction will likely be counterintuitive. A soft outcome means less pressure on the BoE and the government, thus allowing Sterling to recover.

A higher CPI read would mean higher rates and more pressure on the government, weighing on sentiment and the Pound. Further trouble in British bond markets may spread to other areas, namely Eurozone countries. The Euro could slip alongside the Sterling in such a case.

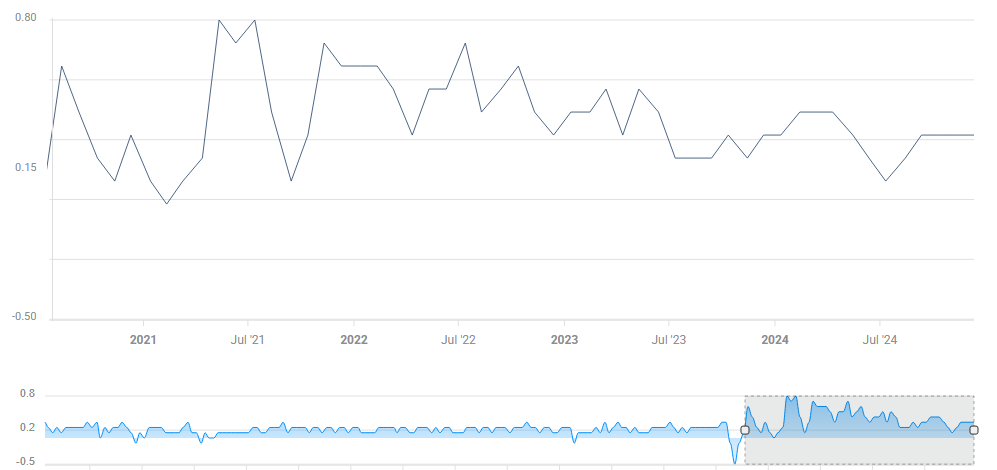

4) US CPI is left, right and center for markets

Wednesday, 13:30 GMT. After the warm-up on Tuesday, the main event awaits on Wednesday – America's first read of consumer inflation. Headline inflation has slipped below 3% YoY, but core prices – excluding volatile energy and food – have been stubbornly high.

The most important figure to watch is core CPI MoM, which rose by 0.3% in the past four months. The annualized rate of 0.3% MoM is roughly 3.6%, which is too high. A 2% core inflation rate is desired, and getting closer to that level would allow the Fed to cut interest rates.

US core CPI MoM. Source: FXStreet.

This time, a more moderate 0.2% increase is expected, and such an outcome would soothe markets – even if it does not mean a rate cut in the Fed's upcoming decision. Investors remain on edge after the strong Nonfarm Payrolls report for December released on Friday.

5) US Retail Sales may provide more volatility

Thursday, 13:30 GMT. The current "US exceptionalism" in economic growth stems from America's relentless consumer. The Retail Sales report for December will provide more details about consumption in the holiday season.

Back in November, around the Black Friday shopping festivity, sales rose by 0.7%, an impressive clip. A more modest increase is on the cards now. The Control Group, aka the "core of the core," is also of high importance, and so are revisions to previous figures.

In general, a strong report would support the US Dollar and weigh on Gold and Stocks – good news for the economy is bad news for equities. A softer read would provide some relief for Stock and Gold, while taking some of the hot air out of the Greenback.

Final thoughts

Markets have been experiencing high volatility at the beginning of 2025 – and with Trump's looming inauguration, it is set to continue, even when the President-elect is not speaking.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)