Five fundamentals for the week: Fed-CPI “Super Wednesday” to provide double whammy

- A fresh read on US inflation may ease fears triggered by the strong Nonfarm Payrolls.

- Any Federal Reserve's rate cut signals are at the center of its decision.

- BoJ officials are likely to weigh on the Yen after weak GDP, raising intervention risks.

- US PPI and consumer confidence data may trigger opportunities to go contrarian.

Top-tier events and London buses have something in common – sometimes the wait is long, and then two come simultaneously. This week, the US Consumer Price Index (CPI) report is published only several hours before the Federal Reserve (Fed) announces its decision, which will be accompained by fresh interest-rate projections. Policymakers may scramble to adapt their projections. These two key events on Wednesday stand out.

1) US CPI may paint a rosier picture than Nonfarm Payrolls, aiding markets

Wednesday, 12:30 GMT. How fast is inflation falling? That has been the main question for markets for over a year. The Consumer Price Index (CPI) is the No. 1 market mover. While the Fed targets the PCE index, another gauge of price rises, CPI is released earlier and triggers fireworks.

The year started with stubbornly high inflation readings, and the calm came only in the April report, which showed a decline in core inflation, which excluded volatile energy and food items.

After receding to 3.6% YoY in April, the economic calendar points to 3.5% in May, another small retreat. Economists are more cautious about the monthly figures, and a repeat of the 0.3% increase seen in April is on the cards.

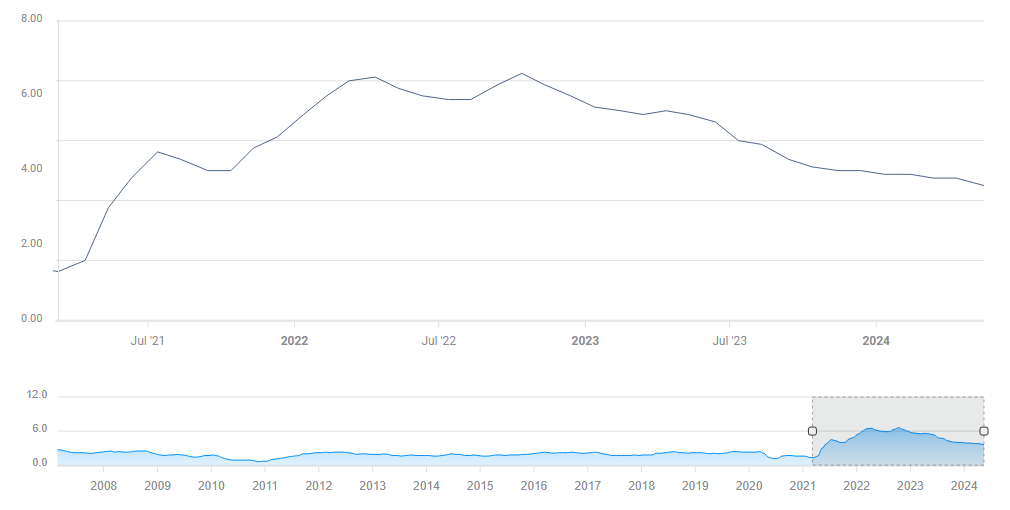

Underlying inflation is falling slowly:

Core CPI YoY. Source: FXStreet

Every tenth matters to markets – and also to policymakers at the Federal Reserve who convene at another place in Washington and announce their decision. One thing is certain – the reaction will be choppy. Some market participants will want to react to the data, while others would want to wait for the Fed to respond to the data.

In case of a deviation of 0.2% percentage points or more from expectations on core numbers, the reaction will be strong, but a miss or beat of only 0.1% percentage points in both monthly and yearly core figures, just in one or none at all would probably trigger up-and-down whipsaws.

In case yearly core CPI comes at 3.5% as expected, it would still be another step down – good news for the Fed, stocks, and Gold. However, the lack of surprise would delay any positive reaction until after the Fed decision.

2) Fed decision hinges on the dot plot

Wednesday, 18:00 GMT, press conference at 18:30 GMT. One or two cuts this year? Some Federal Reserve officials have signaled no reductions to interest rates at all. Every three months, the Fed publishes an updated forecast for growth, inflation, employment, and, most importantly, interest rates. Back in March, the median of forecasts pointed to three cuts in 2024 – but only just.

The world´s most powerful central bank is widely expected to leave interest rates unchanged once again, but these new forecasts, the "dot plot," are released at the same time and will trigger the initial reaction.

A median of one cut would boost the US Dollar (USD), while two cuts would buoy stocks and Gold.

Investors will also eye the statement, especially comments on inflation, on the back of fresh CPI data published earlier in the day. The key word is confidence. If the bank is confident that inflation is falling, it would be positive to markets, while reiterating a worried approach on price rises would weigh.

Fed Chair Jerome Powell will meet with the press 30 minutes after the release, and his comments on rates, growth, inflation, and employment all matter. Back in May, he said that "unexpected weakness" in the labor market would trigger an earlier rate cut. While the Fed still seemed focused on inflation, Powell seemed to put more emphasis on employment than beforehand.

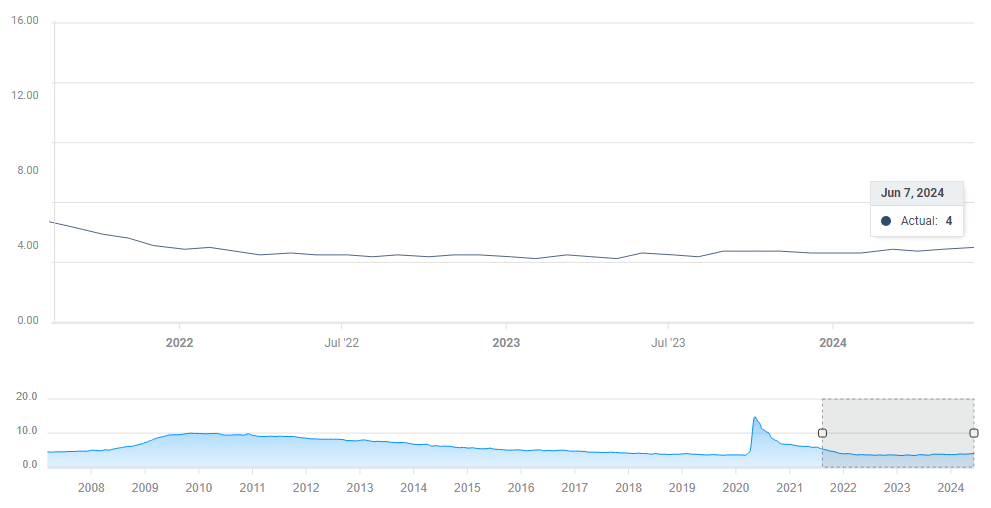

According to the Nonfarm Payrolls, the unemployment rate rose to 4% in May. Does that worry Powell?

US unemployment rate. Source: FXStreet

Any concern over the labor market would trigger hopes of an early rate cut. On the other hand, that same NFP also showed a significant increase in jobs, of 272,000.

One certainty about Powell is that he will say that the Fed is data-dependent. Specific comments about the CPI report will be of interest – and it may unleash some pent-up pressures related to the report. That would add to volatility.

All in all, the dot plot will likely trigger the initial reaction, and further moves will depend on the statement on Powell – and what happened earlier in the CPI.

3) PPI may trigger choppy price action

Thursday, 12:30 GMT. Less than 24 hours after the Fed decision, the Producer Price Index (PPI) report provides another view on inflation. Prices at factory gates, as PPI is also known, serve as an indicator of future consumer inflation. While the correlation is weaker than in the past, it will trigger some market action.

After a jump of 0.5% in core PPI in April, some moderation is on the cards now. A deeper drop would comfort markets, boosting stocks and Gold, while signs of rising inflation would lift the US Dollar.

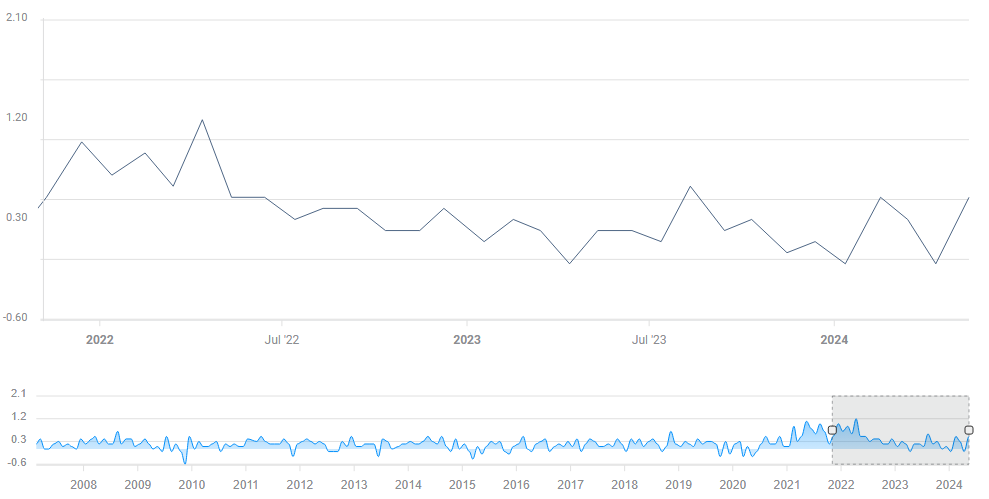

Core PPI has been choppy in recent months:

Core PPI MoM. Source: FXStreet

I expect any reaction to be short-lived, providing an opportunity to go contrarian – algorithms react first, and humans digest the full meaning of the data later. A whipsaw is more likely if the data goes against the narrative painted in the CPI and the Fed decision.

If markets are gloomy and PPI is weak, optimism will fade quickly. A strong PPI against the backdrop of a dovish Fed and softer CPI would also result in a snapback.

4) BoJ to weigh on Yen with dovish policy

Friday, during the Asian session. Will Japanese interest rates rise again? The Bank of Japan (BoJ) was the last major central bank to raise rates – and only to 0% from negative levels. While the world's third-largest economy is out of its deflationary mindset, inflation remains subdued.

With a 5% differential between US and Japanese interest rates, there is no wonder USD/JPY is up – but that means imports into Japan are becoming unnecessarily expensive. Officials in Tokyo want some domestic inflation but not imported one – hence the occasional interventions to strengthen the Yen.

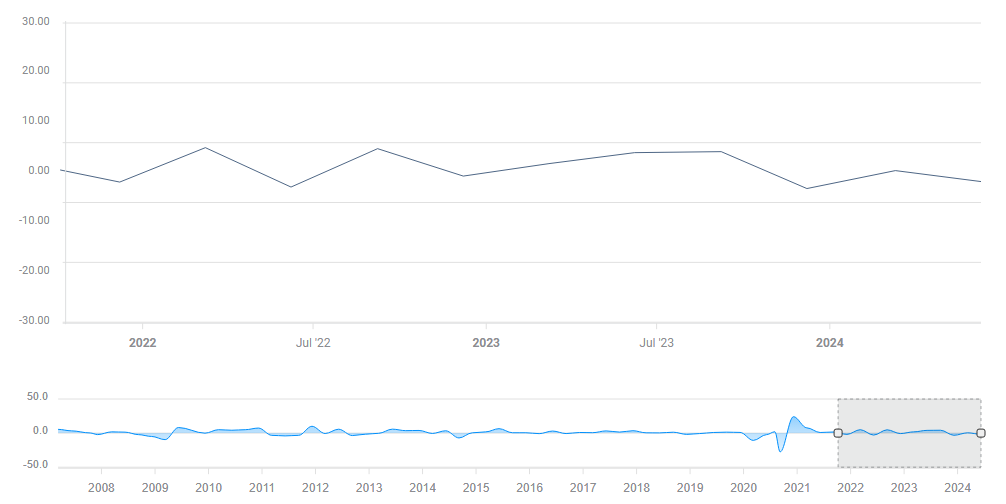

At this junction, the BoJ is set to leave rates unchanged – not only because inflation remains moderate, but also as the economy squeezes. Updated Gross Domestic Product (GDP) data for the first quarter showed an annualized fall of 1.8%. That is alarming, and implies no rate hikes on the horizon.

Japanese GDP. Source: FXStreet

A dovish message from the BoJ could trigger a fresh weakening of the Yen, causing the Japanese Ministry of Finance (MoF) to instruct an intervention.

Despite the lack of change in monetary policy, USD/JPY and Yen crosses may experience extreme volatility in the aftermath of the decision.

5) Consumer confidence has the last word of the week

Friday, 14:00 GMT. A sneak peek into consumption in June – that is what the University of Michigan's Consumer Sentiment Index promises. The correlation between confidence and actual shopping has weakened – Americans say the economy is weak but that they are doing well, and retail sales are robust.

Nevertheless, after a week packed with action, the mere publication of this data point is set to rock markets. Investors will be watching the long-term inflation expectations components of this report, as the Fed also looks at it. The final read for May stood at 3%, and any deviation may trigger a reaction.

Like with PPI, I expect a short-term move that could be reversed. The mere publication of the data means there are no more figures, and that investors can take a look back at the week. If the moves were strong, some profit-taking could come, reversing some of the moves triggered by "Super Wednesday" and other events.

Final Thoughts

It is rare for the CPI and the Fed decision to happen on the same day, and that means unexpected volatility – that could be unleashed with a delay. I recommend trading with extra care.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.