Five fundamentals for the week: Fallout from German vote, Fed's favorite figure stand out

- Germany's elections have a clear winner, but the pace of creating a government is among the uncertainties.

- Trump's tariffs are likely to remain market movers ahead of the March 1 deadline for Mexico and Canada.

- Core PCE – the Fed's favorite inflation gauge – provides a strong end to the week and the month.

Statements, not facts, are set to dominate the last week of February. Further fallout from Germany's elections and new comments from Trump on trade may overshadow most figures –but not the Fed's favorite inflation figure.

1) German political agility is critical for markets

The business-friendly CDU/CSU won the elections and markets cheered–but then things became complicated. While their leader Friedrich Merz can form a government with only one additional party, the SPD, things may take time. Outgoing Chancellor Olaf Scholz may struggle to steer his SPD party after a devastating defeat. Europe and the world need quick tasks to have a stable government.

Another worry is what a new government can do. The German constitution heavily limits debt spending, and mainstream parties lack the two-thirds majority needed to unleash the power of the purse. There are three ways to overcome this, and statements from Merz about his willingness to use them may go a long way to boost the Euro and Stocks.

First, he may take a break from the brake, but that is limited to one year. Second, he could convince eight parliaments from extreme parties to support a constitutional change–but they'll want something in return, and negotiations could take months. Third, Germany could push for common European lending for expenditures such as defense. Everything is possible, but nothing is easy.

It all starts with Merz's determination. Without it, market enthusiam may turn into a malaise, like Gemany's economy.

2) Trump may slap new tariffs on everybody

There seemed to be a detente with China–a potential new deal–but United States (US) President Donald Trump may have changed his mind. Reports suggest the White House is mulling new punishments for Beijing. Chinese and global equities are waiting.

After Vice President JD Vance said Europe's biggest problem is not China nor Russia but internal problems, the administration is not done with the old continent just yet. There is a risk of tariffs on various goods, which are delayed. At least so far, Trump congratulated Merz, which is a positive sign for the near future.

The focus will likely shift to countries closer to home. Mexico and Canada won a reprieve from instant duties in early February after agreeing to send troops to guard their borders with the US. That was a temporary suspension through March 1.

Will Trump slap 25% tariffs on his neighbors? Markets expect some deal to delay any moves, but nothing is guaranteed. The Canadian Dollar and Mexican Peso could come under pressure.

3) US GDP may shake nervous markets

Thursday, 13:30 GMT. While worries about consumer behavior in 2025 are rising, the updated Gross Domestic Product (GDP) report for the last quarter of 2024 looks at the basis of the US economy entering the Trump era.

The first release showed an annualized growth rate of 2.3%, and the economic calendar points to a confirmation of that figure. Given the limited expectations, there is room for any surprise to have a bigger impact than usual.

Any reaction depends on two factors. First, whether the other released figures –Durable Goods Orders and Unemployment Claims also point in the same direction. In some cases, a bulk release of data points in various directions, resulting in no meaningful move.

Second, the magnitude of the surprise matters. An outcome above 2.5% or below 2% would be more significant than a couple of tenths of percentage points.

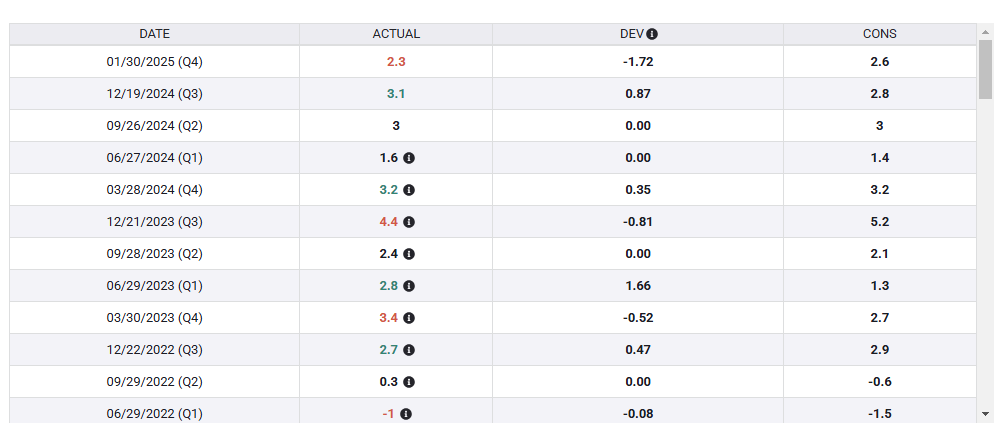

US GDP developments. Source: FXStreet.

4) Core PCE may trigger nasty surprise

Friday, 13:30. What the Federal Reserve (Fed) talks about when it talks about inflation–the core Personal Consumption Expenditure (core PCE). While markets react strongly to the early Consumer Price Index (CPI) report, the PCE released later on is critical for Fed decisions.

After edging higher in recent months, core PCE is expected to drop from 2.8% YoY in December to 2.6% in January. However, the MoM read is projected at 0.3% this time, up from 0.2% last time.

The calculations are based on the CPI and also the Producer Price Index (PPI) and deviations are limited. That makes any 0.1% surprise meaningful. I think there is more room for the upside than the downside in core PCE, which excludes volatile food and energy costs.

Another sign of higher inflation would boost the US Dollar, while a lower figure would support Gold and Stocks.

5) End-of-month flows may throw up all technicals

Friday, usually around between 15:00 to 17:30 GMT. When the last day of the week happens on the last day of the month, there is extra action from money managers scrambling to adjust their portfolios. There is usually a tendency to see a reversal of previous trends, but the moves can prove unpredictable

Traders who focus on price action only–technical analysis enthusiasts who dismiss fundamentals–should at least be aware of the timing. Technical barriers are suddenly shattered and they tend to hold up for a long time.

After some weakness in the US Dollar, there is room for a re-strengthening, assuming that does not occur on Friday.

Final Thoughts

Politics do not always trump (pun intended) data in such an extreme manner, but this week is special, so trade with care.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.