Feds runs another massive budget deficit in July despite surge in tariff revenue

Uncle Sam is cashing in on tariff revenue, but it’s not keeping up with his out-of-control spending habits.

Despite triple the amount of tariff income, the July budget deficit surged to $294.14 billion, 19 percent higher than a year ago, according to the Monthly Treasury Statement.

Meanwhile, the national debt officially eclipsed $37 trillion on Aug. 11.

The fiscal 2025 budget deficit stands at $1.63 trillion with two months remaining.

Federal revenues were up about 2 percent year-on-year in July thanks to a surge in tariff receipts. The government collected $22.7 billion in customs receipts. That compares to $7.1 billion in July ’24.

Through the first 10 months of fiscal 2025, the U.S. government brought in $135.7 billion in customs duties. That’s up $73 billion, or 116 percent, from the same period in fiscal ’24.

In total, the federal government has collected $4.35 trillion so far in fiscal 2025. That’s 6.6 percent higher than through the same period last year.

However, the healthy boost in income isn’t keeping pace with the incessant government spending.

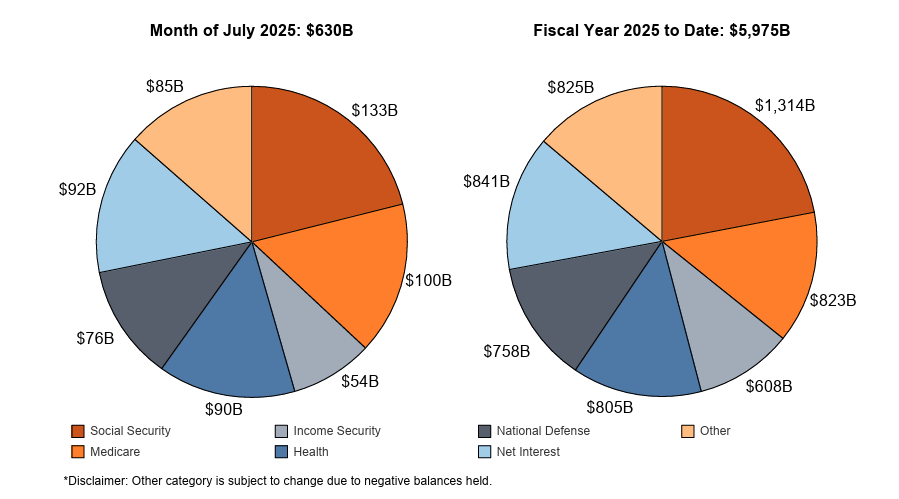

The Trump administration blew through $629.64 billion in July. That was 10 percent higher than last year.

So far in fiscal 2025, the federal government has spent $5.98 trillion, a 6.8 percent increase over the same period last year.

There is no indication that spending will slow down any time soon. The Big Beautiful Bill “cut” some spending but increased it in other areas. Furthermore, those “cuts” were from projected spending increases. Actual spending will still go up, just not as fast as originally planned. The bottom line is that even with the Big Beautiful Bill, spending will increase on an absolute basis.

This is par for the course.

You might recall that President Biden promised that the [pretend] spending cuts would save “hundreds of billions” with the debt ceiling deal (aka the [misnamed] Fiscal Responsibility Act).

That never happened.

Supporters of the Big Beautiful Bill expect economic growth stimulated by tax cuts to boost revenue and narrow the deficit. However, history casts significant doubt on this claim.

The ugly truth is the government isn't committed to cutting spending in any meaningful way, and it always finds new reasons to spend even more, whether for "crises" at home or wars overseas.

The interest problem

The federal government is being increasingly burdened by its skyrocketing interest expense. This is one of the reasons President Trump and others in the administration are pressuring the Federal Reserve to slash interest rates.

Interest on the national debt cost $91.9 billion in July. That brought the total interest expense for the fiscal year to $1.01 trillion, up 6 percent over the same period in 2024.

Net interest (interest expense – interest receipts) stands at $841 billion through the first 10 months of this fiscal year.

So far, in fiscal 2025, the federal government has spent more on interest on the debt than it has on national defense ($758 billion) or Medicare ($823 billion). The only higher spending category is Social Security ($1.31 trillion).

Uncle Sam paid $1.13 trillion in interest expenses in fiscal 2024. It was the first time interest expense had ever eclipsed $1 trillion. We’re close to that number already, with two months remaining in the fiscal year.

Much of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and must be replaced by bonds yielding much higher rates. And even after the Federal Reserve cut rates, Treasury yields have pushed upward as demand for U.S. debt sags.

Ramifications

Some people claim that borrowing, spending, and big national debts don’t matter.

They do.

According to the national debt clock, the current debt level represents 123.3 percent of the GDP. Studies have shown a debt-to-GDP ratio of over 90 percent retards economic growth by about 30 percent.

And as the Bipartisan Policy Center points out, the growing national debt and the mounting fiscal irresponsibility undermine the dollar.

“Confidence in U.S. creditworthiness may be undermined by a rapidly deteriorating fiscal situation, an increasing concern with federal debt set to grow substantially in the coming years.”

This could lead to lower economic growth, higher unemployment, and less investment wealth.

Lack of confidence in the U.S. fiscal situation could also lower demand for U.S. debt. This would force interest rates on U.S. Treasuries even higher to attract investors, exacerbating the interest payment problem. As already mentioned, we saw a big spike in Treasury yields despite Fed rate cuts. Yields increased again in the wake of the trade war. There is growing evidence that Treasuries are already losing their safe-haven appeal.

Biden ran the debt higher at a dizzying pace, but to be fair, this isn’t just a Biden problem. Every president since Calvin Coolidge has left the U.S. with a bigger national debt than when he took office.

It’s going to take more than DOGE rooting out waste to get the borrowing and spending under control. Even if the Trump administration manages to slash discretionary outlays as promised, that only accounts for 27 percent of total spending. The vast majority is for entitlements, and there is little political will to take the scissors to Social Security or Medicare.

And the sad fact is that, given the political incentives, people in power will always kick the debt can down the road. It is a long-term problem that will require painful measures to fix. Politicians don't want to create pain. That's a quick path out of office. So, they will punt the debt problem and spend more to make constituents happy.

This is all well and good, but the problem with playing kick the can down the road is that you eventually run out of road.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Mike Maharrey

Money Metals Exchange

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.