Federal Reserve Preview: The Good, the Bad and the Ugly, why the US Dollar would rise

- The United States Federal Reserve is set to raise rates by 25 bps despite some signs of economic weakness.

- A relatively robust jobs market will likely cause Fed Chair Jerome Powell to be relatively hawkish.

- Officials are set to wait for new data and new forecasts in March to signal potential softer policy.

The cracks are beginning to show – but the world's most powerful central bank will likely shrug it off. Seeing the glass half full will likely hit stocks and boost the US Dollar in the upcoming Federal Reserve (Fed) decision, set to be announced on Wednesday, February 1 at 19 GMT.

The Good – Inflation is coming down while unemployment remains low

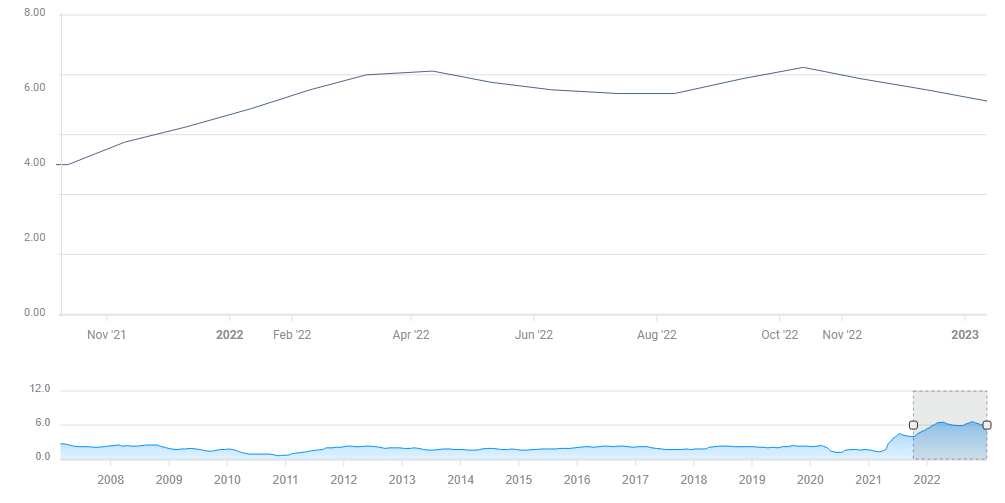

The Federal Reserve has two mandates, full employment and price stability. Headline inflation has come down from a peak of 9.1% to 6.5%, and also the Core Consumer Price Index (Core CPI) is down from its peak, at 5.7%.

It is not only the price at the pump, nor the prices of food, but also less-volatile items:

US CPI ex Food & Energy (YoY)

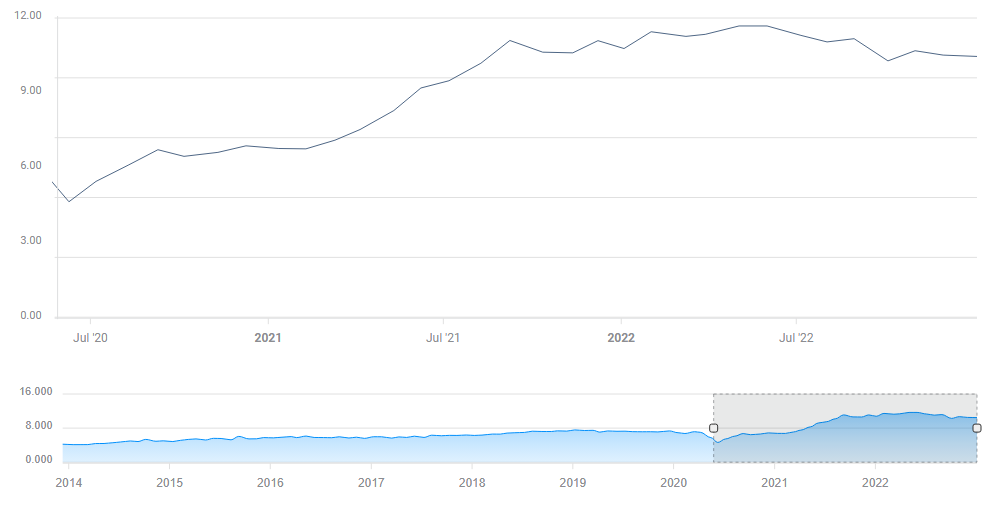

On the other mandate, employment, the picture is rosier – thus pushing inflation higher. According to the most recent JOLTs job openings reports, there are roughly two vacancies for every unemployed person in the United States.

US JOLTS Job Openings

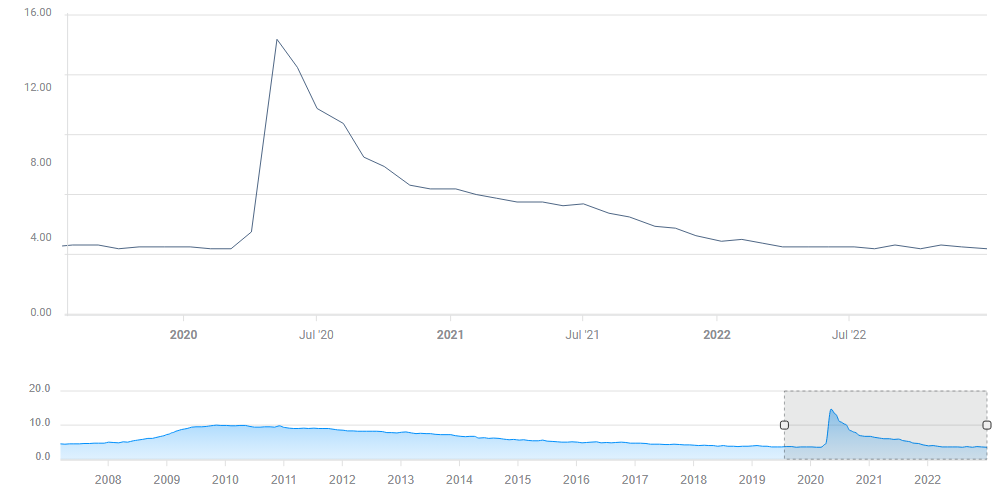

That drives employers to raise wages, adding to price pressures. The broader measure of the labor market, the unemployment rate, is at 3.5%. That matches the pre-pandemic trough – also the lowest since 1969.

US Unemployment Rate

In such an environment, there is more room to raise interest rates to ensure that inflation continues falling. Fed Chair Jerome Powell stressed that the bank wants to refrain from moving prematurely. History shows that declaring victory early leads to renewed price pressures down the road.

The Bad – Cracks are showing in the US economy

Is the labor market so resilient? Layoffs in tech companies have been intensifying and accelerating in recent weeks, affecting not only top earners hired in the talent wars of 2021, but also reaching other workers. That is some hard data to digest.

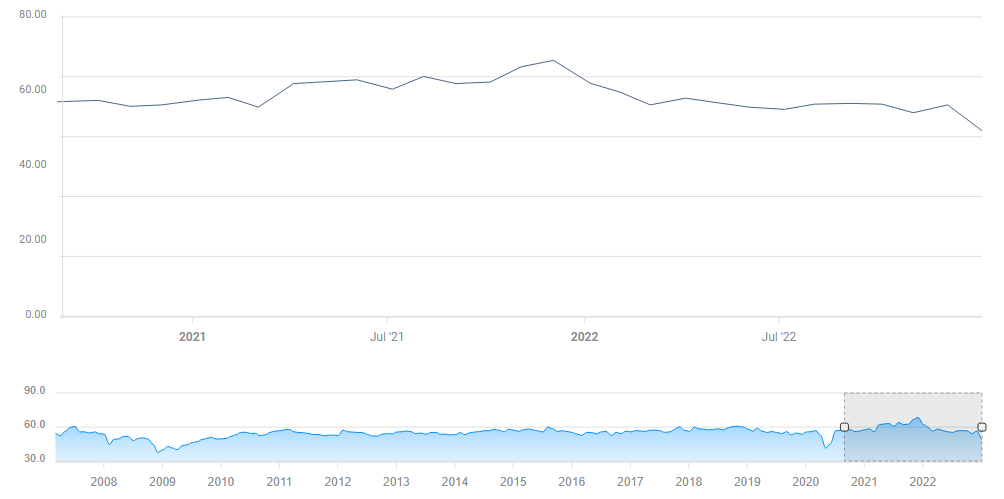

Fears of a recession are also showing in soft data. The ISM Purchasing Managers' Index (PMI) for the Services sector paints a worried picture, falling into contraction in America's largest sector.

ISM Services PMI

Layoffs at Silicon Valley and a drop in business sentiment may push inflation lower, and they join signs of cooling from the housing sector – directly impacted by rising interest rates. Supply chain issues have mostly been resolved, also cutting costs.

The Ugly – Uncertainty is high

The Fed's interest rate rose from 0% to a range of 4.25-4.50%, and there may be more room to raise rates, but how long does it take these moves to crush inflation? In the past, it took policy some 12-18 months to fully reach the economy. However, the times are changing and everything is moving faster. But exactly how fast? That remains a topic of heated debate.

Moreover, Fed "insider" Nick Timiraos of the Wall Street Journal (WSJ) reported that some at the Federal Reserve are worried about a renewed wave of inflation. Some disagree.

The final arbiter is the data. Between the upcoming Fed decision on February 1 and the following one in March 22, the United States releases two more Nonfarm Payrolls (NFP) reports, and a pair of CPI publications.

In addition, the Fed will present new forecasts for inflation, employment, growth and interest rates in its March decision. All in all, there is no reason for the central bank to stray from its message – to hike borrowing costs to above 5% and leave them there for the remainder of the year.

Fed Interest Rate expectations

Expected market reaction – Stocks down, US Dollar up

The Federal Reserve is set to raise interest rates by 25 bps – that is fully priced in, and the bank does not surprise investors. The question is: will officials signal an upcoming pause? My answer is a clear “No.”

While worrying signs are beginning to show, Fed Chair Jerome Powell and his colleagues will find evidence of softness too weak at this point. The bank will likely continue focusing on robust job data and the fact that non-shelter core services inflation – which is price rises driven by wages – is still too high.

Moreover, the uncertainty mentioned above is a reason to wait with any signal of a pause – and that is not what investors want to see. Bond markets are pricing a peak interest rate of just below 5% and cuts later this year. A denial from Powell would send it down.

If Jerome Powell conveys a hawkish message as I expect, the US Dollar will rise, benefiting from prospects of higher rates – and from safe-haven flows. If the United States continues to cool down its economy, it will affect the entire world, causing a downturn. In times of worry, the Greenback is the currency of choice.

Will the downbeat mood persist? Not necessarily. Another message that Powell is set to reiterate is that the bank is data-dependent. Additional cracks in the US economy would cause a rethink by officials. The focus will soon shift from fighting inflation to fighting a recession – but not in the February 1 Fed decision.

Final thoughts

Markets react several times to the Federal Reserve decision, making trading the event difficult compared to other ones. Investors respond to the publication, then to Jerome Powell's press conference, and the narrative takes more time to settle in. I recommend new traders to trade with lower leverage or stay on the sidelines.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.