Federal Reserve Policy: Patience and a good economy

- Fed reduces economic and rate projections for 2019 and 2020

- Dollar drops, equities recover then fall, interest rates decline

- Powell lauds economy while Fed rate policy pauses

FOMC Policy and Projections

The Federal Reserve downgraded its view of US growth this year and next, officially moved to a neutral rate policy yet kept its optimism about the general state of the American economy which Chairman Jerome Powell referred to several times “As in a good place.”

In its closely followed Projection Materials which the central bank issues four times a year, in March, June, September and December, economic growth in 2019 dropped to 2.1% from 2.3%, core PCE inflation slipped to 1.8% from 1.9% and the estimated fed funds rate at year end fell to 2.4% from 2.9%.

In the six months since the September release of the same information the Fed’s estimate for GDP has fallen 0.4% from 2.5%, core inflation 0.3% from 2.1% and the fed funds rate has decreased 0.7% to 2.4%.

From a policy prospective the drop in the fed funds estimate brought the bank’s three year old rate hike campaign to a halt.

In December's materials the 2.9% forecast for 2019 coupled with the 0.25% increase at that meeting meant two more hikes would be needed this year to 3.0% to cover the 2.9% goal. The new projections with 2.4% this December, which would strictly require one 0.25% reduction from the current 2.5%, and 2.6% by December 2020, which would need one or two hikes depending on the action this year, imply some possibility for rate flexibility, in practice it is a formula for the Fed to be inactive through the end of next year.

The Fed also clarified its intentions on the disposition of its balance sheet acquired in the years after the financial crisis of 2008 and recession. “Since 2017 we have been allowing our assets to decline. We intend to slow the runoff of assets in May and stop in December,” said Chairman Powell in the press conference following the policy announcement.

Market Reaction

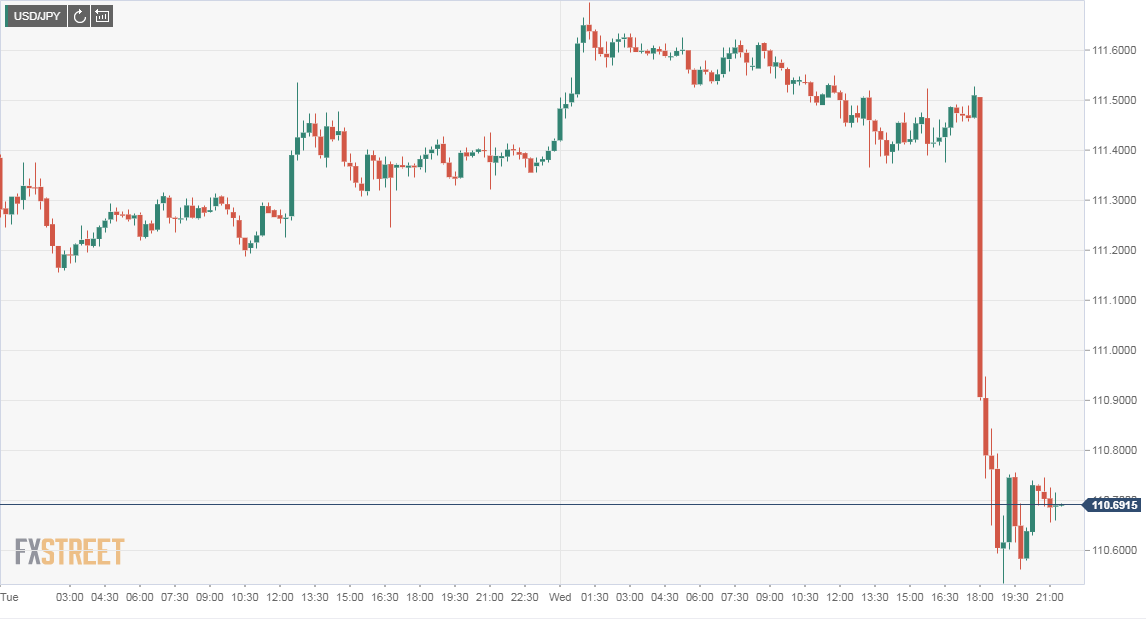

Markets reacted swiftly to the change in Fed policy. The dollar fell sharply losing a figure against the euro to 1.1448 and a figure versus the yen to 110.53, though it regained some of its losses against both currencies into the close.

Equities were whipsawed with the Dow initially running higher on the dovish rate news but slipping into the finish, closing off 141.71 points, 0.55% at 25745.67. The S&P 500 lost 8.34 points, 0.29% to 2824.23.

Dow

CNBC

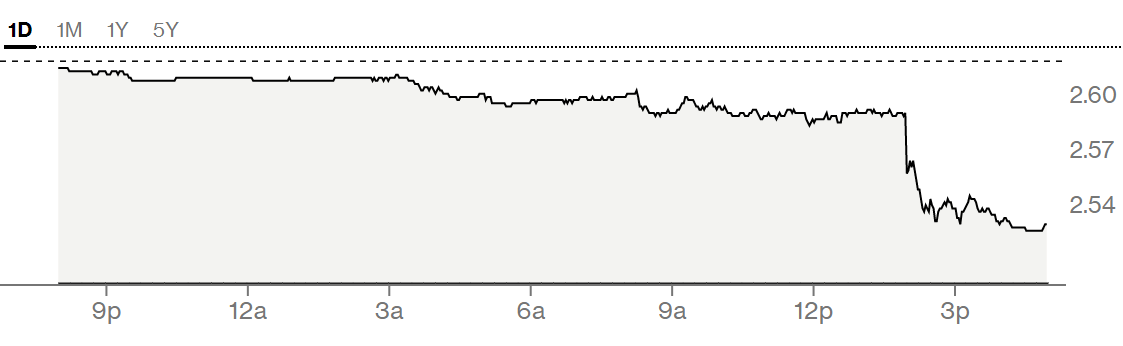

Treasury prices moved higher and rates lower with the 10-year yield losing 9 points to 2.53% almost at the bottom of its 52 week range of 2.52% to 3.26%. The 2-year lost 7 points of yield to 2.40% its lowest return in almost a year.

10-Year Treasury Yield

Chairman Powell in his lengthy news conference stressed the good condition of the US economy. The FOMC statement said “The Committee continues to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes.” The closing sentence of that paragraph was unchanged from January, “In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support these outcomes.”

Is it possible that the international risks cited by the Chairman Powell, Brexit, the US-China trade dispute and slowing global growth resolve themselves by the end of the second quarter and the Fed’s discretion and patience is rewarded with revived prospects for the US economy? Chairman Powell would probably answer ‘Yes, but that is not the data we have now.”

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.