Federal Reserve: High(ER) for longer

In the world of central banking, nothing is what it seems. The ECB’s recent rate hike was considered dovish whereas the pause by the Federal Reserve received the label hawkish. These reactions show that, beyond the rate decision, the accompanying message also matters. That of the ECB was interpreted as signaling that the terminal rate had been reached. In the US, the latest rate projections of the FOMC members -the dot plot- point toward another hike before year end and a federal funds rate that would stay elevated for longer. This is unsurprising given the resilience of the US economy in reaction to the aggressive monetary tightening and the concern that bringing inflation back to the 2% target would take more time. These projections are surrounded by a lot of uncertainty at the current juncture considering that part of the impact of past rate hikes still needs to manifest itself, the recent significant increase in energy prices and the headwinds from weak growth in China and the Eurozone.

In the world of central banking, nothing is what it seems. Central bank watchers called the latest rate hike by the ECB a dovish hike, whereas the decision of the Federal Reserve to leave the federal funds rate unchanged was considered a hawkish pause.

At first glance, these descriptions seem counterintuitive, but they reflect the importance of the message that came with the announcements. The monetary policy statement of the ECB mentioned “that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our target.”1 This has been interpreted as signaling that policy rates in the Eurozone probably have reached their peak2. The Federal Reserve on the other hand may very well increase the federal funds rate again before the end of the year3.

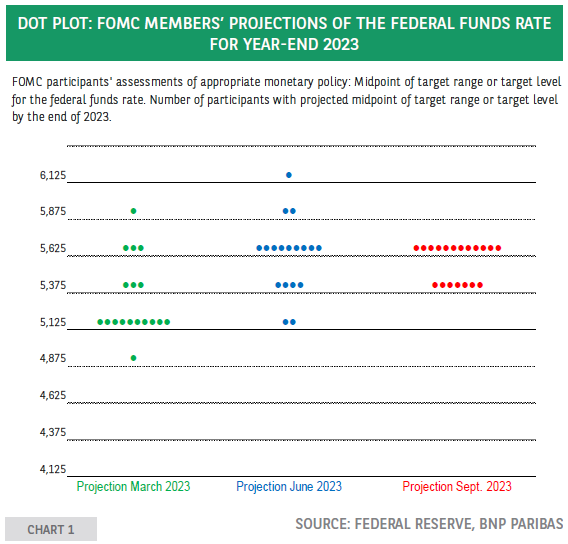

The new Summary of Economic Projections (SEP) shows that 12 FOMC members consider a further 25 bp increase of the federal funds rate by the end of the year appropriate, given the Fed’s mandate and the growth and inflation outlook. Seven members think that the policy rate already is at the appropriate level. Consequently, the median estimate of the federal funds rate at the end of this year is 25 bp higher than its current level. During this year, the year-end projection has drifted higher (chart 1) reflecting an upward revision of the growth and inflation projections. More important however in the latest SEP is the 50 bp increase of the projected federal funds rate at the end of 2024 and 2025, respectively to 5.1% and 3.9%. The prospect of official rates moving higher and staying there for longer explains why the decision to leave rates unchanged received the label of a hawkish pause and why Treasury yields moved higher whereas equity markets in the US and abroad declined.

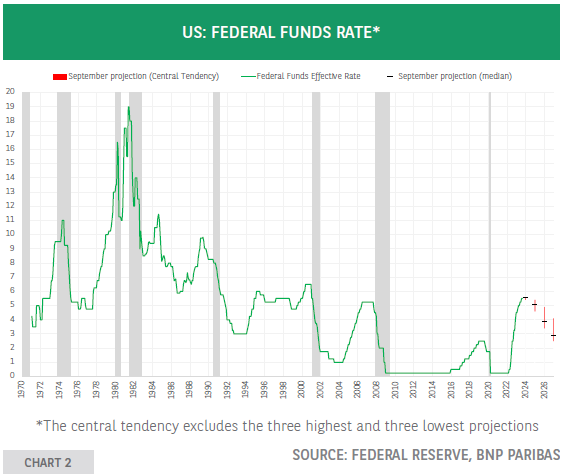

As shown in chart 2, the projections show a federal funds rate that would stay elevated throughout next year, despite the start of an easing cycle. The latter is expected to be slower compared to previous experiences.

This reflects a view that bringing inflation back to the 2% target will take time and that the central bank should not ease too quickly. Premature rate cuts could boost growth thereby running the risk of stopping the disinflation process and the Fed losing its credibility. The projected rate path can also be seen as reflecting an expectation of a soft landing. In such case there is no need to cut rates aggressively.

These projections are surrounded by a lot of uncertainty, in particular at the current juncture considering that part of the impact of past rate hikes still needs to manifest itself. The recent significant increase in energy prices, weak growth in China and the Eurozone are headwinds for the US economy and complicate the analysis. In this respect, it was very revealing that during his press conference, Jerome Powell answered the question “Would you call the soft landing now a baseline expectation?” by saying “No, no. I would not do that”, adding that it is possible, whilst refusing to express a view on how likely such an outcome would be4. Monetary policy of the Fed is data dependent and the projections of the FOMC members as well. The Fed and its watchers will continue to scrutinize the incoming data more than ever.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.