Fed Worried About Lack of Inflation, Stock Market Bubble (Sort Of)

FOMC minutes show Yellen is no longer convinced that low inflation is transitory. Other members mention bubble concerns.

Minutes of the FOMC Oct. 31-Nov. 1 meeting reflect concern inflation could stay below target longer than expected. The minutes also show a concern over bubbles.

Inflation or not, the Wall Street Journal reports Fed on Track for December Rate Rise, but Inflation Worries Persist.

Federal Reserve officials said at their latest meeting they likely would raise short-term interest rates “in the near term” because of a strengthening economy, although several said their support for the move would hinge on whether they see inflation picking up.

With three weeks to go until the Fed’s final scheduled gathering of 2017, the minutes of the Fed’s last meeting reinforced market expectations that a quarter-percentage-point rate increase is imminent. The market for federal-funds futures contracts, where traders bet on the path of interest rates, suggested a 100% probability of a rate increase at the Dec. 12-13 meeting, according to CME Group.

Yet minutes of the Oct. 31-Nov. 1 meeting, released Wednesday with the usual three-week lag, indicated that officials thought persistently weak inflation could stay below their 2% annual target for longer than many expected, raising questions about the pace of rate increases next year.

FOMC Minutes

Let's dive straight into the FOMC Minutes for more details (Emphasis mine).

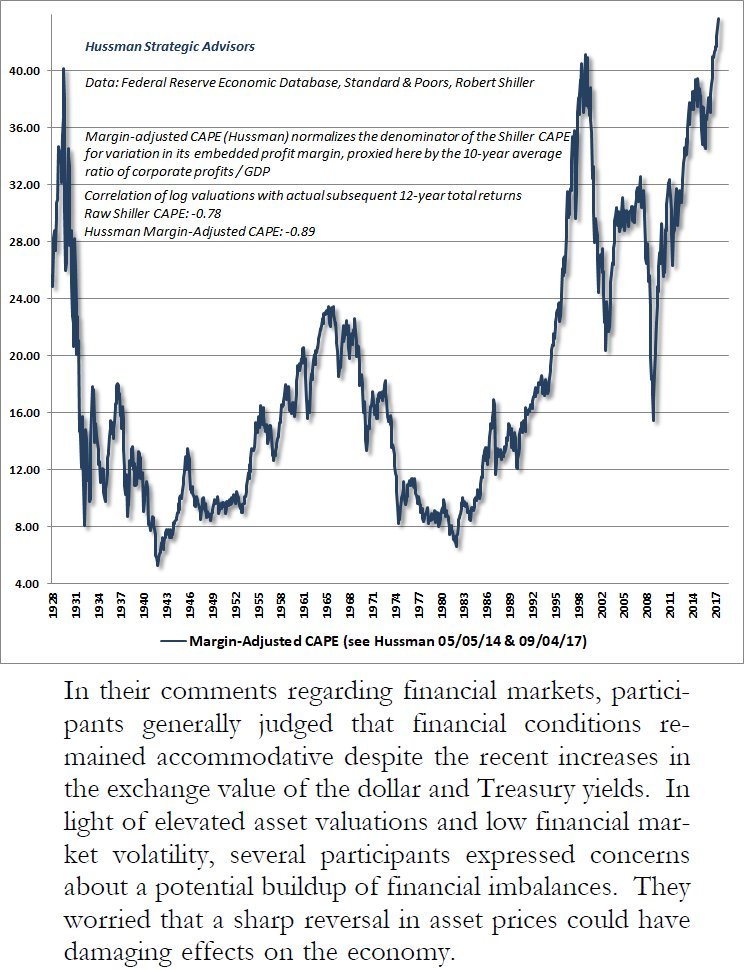

Asset Valuation Discussion

The staff continued to judge that the overall vulnerabilities were moderate: Asset valuation pressures across markets were judged to have increased slightly, on balance, since the previous assessment in July and to have remained elevated; leverage in the nonfinancial sector stayed moderate; and, in the financial sector, leverage and vulnerabilities from maturity and liquidity transformation continued to be low.

In their comments regarding financial markets, participants generally judged that financial conditions remained accommodative despite the recent increases in the exchange value of the dollar and Treasury yields. In light of elevated asset valuations and low financial market volatility, several participants expressed concerns about a potential buildup of financial imbalances. They worried that a sharp reversal in asset prices could have damaging effects on the economy. It was noted, however, that elevated asset prices could be partly explained by a low neutral rate of interest. It was also observed that regulatory changes had contributed to an appreciable strengthening of capital and liquidity positions in the financial sector over recent years, increasing the resilience of the financial system to potential reversals in valuations.

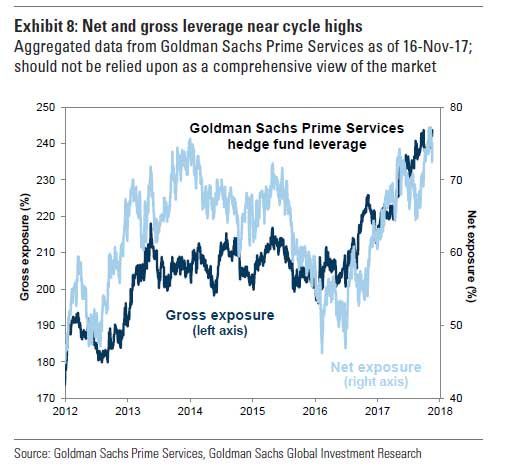

The participants essentially mentioned the asset bubble concern, then brushed it aside. Here are a couple of pertinent Tweets.

Hussman Tweet on Imbalances

ZeroHedge Tweet on Leverage

Following those well-stated points of view, let's return to the FOMC minutes for an absurd discussion of "inflation expectations".

FOMC Inflation Discussion

With core inflation readings continuing to surprise on the downside, however, many participants observed that there was some likelihood that inflation might remain below 2 percent for longer than they currently expected, and they discussed possible reasons for the recent shortfall.

Many participants observed that continued low readings on inflation, which had occurred even as the labor market tightened, might reflect not only transitory factors, but also the influence of developments that could prove more persistent. A number of these participants were worried that a decline in longer-term inflation expectations would make it more challenging for the Committee to promote a return of inflation to 2 percent over the medium term.

In view of the persistent shortfall of inflation from the Committee's 2 percent objective and questions about whether longer-term inflation expectations were consistent with achievement of that objective, a couple of participants discussed the possibility that potential alternative frameworks for the conduct of monetary policy could be helpful in fulfilling the Committee's statutory mandate.

Inflation Expectation Ridiculousness

As I have pointed out on numerous occasions, inflation expectation concerns are absurd.

Q: If consumers think the price of food will drop, will they stop eating out?

Q: If consumers think the price of food will drop, will they stop eating at home?

Q: If consumers think the price of natural gas will drop, will they stop heating their homes and stop cooking to wait for the event.

Q: If consumers think the price of gas will drop, will they stop driving or not fill up their car if it is running on empty?

Q: If consumers think the price of gas will rise, can they do anything about it other than fill up their tank more frequently?

Q: If consumers think the price of rent will drop, will they hold off renting until that happens?

Q: If consumers think the price of rent will rise, will they rent two apartments to take advantage?

Q: If consumers think the price of plane tickets, taxis, and bus tickets will drop, will they hold off taking the plane the train or the bus?

Q: If consumers think the price of plane tickets, taxis, and bus tickets will rise, will they rush out and buy multiple tickets driving the prices even higher up?

Q: If people need an operation, will they hold off if they think prices might drop next month?

Q: If people need an operation, will they have two operations if they expect the price will go up?

Those items constitute 80.254% of the CPI.

Stupidity Well Anchored

Yellen frequently comments that "Inflation expectations are well anchored".

The only thing that’s “well anchored” is the stupidity of the belief that inflation expectations generally matter.

In practice, the only time inflation expectations matter is when an economy is in or approaching hyperinflation. At such times, people will spend every cent on something the moment they can.

Asset Inflation Irony

In contrast to routine purchases of goods and services, people will rush to buy stocks in a bubble if they think prices will rise. They will hold off buying stocks if they expect prices will go down.

People will buy houses to rent or fix up if they think home prices will rise. They will hold off housing speculation if they expect prices will drop.

Bitcoin is another excellent example.

The very places where expectations do matter are the very things the Fed and mainstream media ignore.

Economic Challenge to Keynesians

Of all the widely believed but patently false economic beliefs is the absurd notion that falling consumer prices are bad for the economy and something must be done about them.

I have commented on this many times and have been vindicated not only by sound economic theory but also by actual historical examples.

-

My article Deflation Bonanza! (And the Fool’s Mission to Stop It) has a good synopsis.

-

My Challenge to Keynesians “Prove Rising Prices Provide an Overall Economic Benefit” has gone unanswered.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc