Fed November Preview: Is it time for a dovish signal?

- US Federal Reserve is widely expected to raise its policy rate by 75 bps.

- Markets are undecided about the size of the Fed’s December hike.

- Wall Street’s reaction to the Fed event could help the dollar determine its next direction.

Following its two-day policy meeting, the US Federal Reserve is expected to raise its policy rate by 75 basis points (bps) to the range of 3.75% - 4% on Wednesday, November 2. The market positioning suggests that such a decision is already priced in, opening the door for a significant reaction to the US central bank’s communication regarding future policy actions.

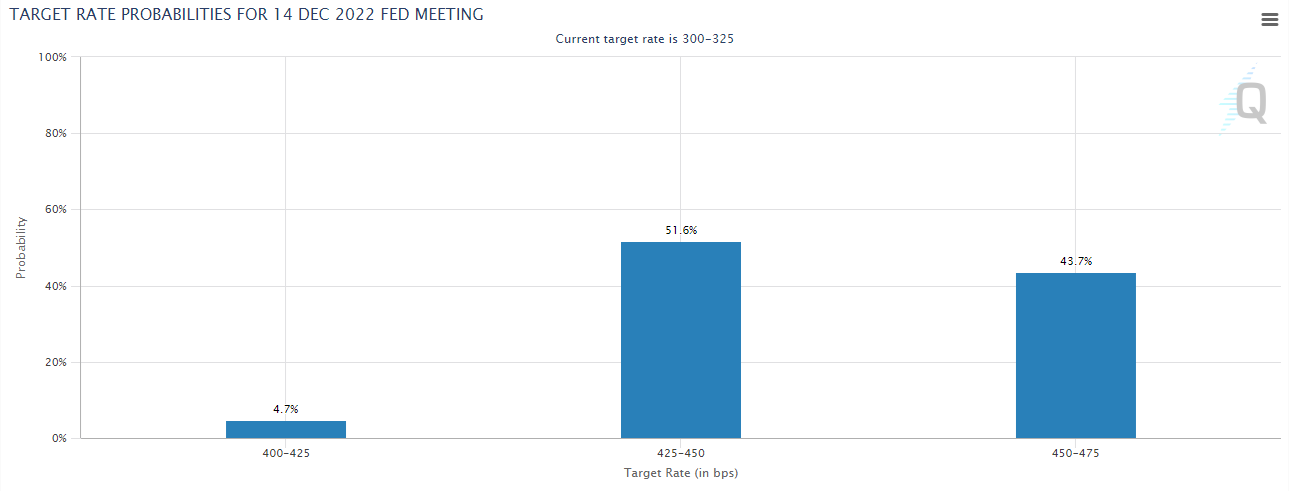

According to the CME Group’s FedWatch Tool, the probability of a 75 bps hike this week stands at around 90%. In December, however, there is a 51% chance of the Fed opting for a smaller 50 bps rate increase.

Source: CME Group

The change of heart came after Nick Timiraos, chief economics correspondent at The Wall Street Journal, wrote earlier in the month that the FOMC policymakers were planning to debate whether and how to signal a smaller hike at the last policy meeting of the year. Additionally, macroeconomic data releases from the US following that development caused investors to adopt a cautious stance and made it difficult for the US dollar to preserve its strength. The S&P Global’s PMI survey revealed that the Composite Output Index declined to 47.3 in October’s flash estimate from 49.5, showing an ongoing contraction in the private sector’s business activity at an accelerating pace.

Furthermore, investors grow increasingly concerned about a housing market collapse amid the negative impact of the Fed’s rate hikes on mortgage demand. The US Federal Housing Finance Agency reported that house prices declined by 0.7% in August and the National Association of Realtors announced that Pending Home Sales fell by 10.2% in September, bringing the annual decrease to an eye-opening 31%.

Dovish scenario

In case the Fed’s policy statement or FOMC Chairman Jerome Powell’s comments at the press conference confirms the US central bank’s intention to go for a 50 bps hike in December, that would likely be assessed as a dovish tilt in the policy outlook. It’s worth noting, however, that the Fed decided to abandon forward guidance earlier in the year and said that policy decisions will be based on incoming data and be taken on a meeting-by-meeting basis. Hence, it would be unlikely for Powell to outright name the size of the next rate move.

A mention of inflation showing signs of having peaked in the policy statement or the press conference could be seen as a dovish clue. The Fed will continue to tighten its policy regardless as its goal is to bring back inflation to its 2% target but it could afford to take its foot off the gas pedal if it actually doesn’t project further buildup in price pressures. A more concerned tone regarding the economic outlook, conditions in the housing market and the possibility of a recession could also fuel expectations that the Fed has reached its peak hawkishness.

Hawkish scenario

Powell will surely be asked about the next rate decision even if he doesn’t offer any clues in his prepared remarks. If the chairman clarifies that one more 75 bps hike will remain on the table for the December meeting unless they see a significant softening in inflation, that would confirm the Fed’s data-dependent approach. In such a scenario, investors would be forced to wait until the next batch of Consumer Price Index (CPI) data before deciding on the next policy action. Nevertheless, market participants are unlikely to commit to a risk rally if they have second thoughts about a potential Fed policy shift and allow the USD to stay resilient against its rivals in the near term.

Summary

FOMC policymakers are walking a fine line as they try to reassure markets that they will continue to battle inflation while avoiding a deep recession. In the absence of forward guidance, it will be even trickier for the Fed to communicate its policy outlook clearly. In December, the updated Summary of Economic Projections will be a useful tool for Fed officials if they want to convey that it’s time for them to ease on tightening. Thus, it wouldn’t be a shocker if the Fed doubles down on the data-dependent approach but investors will scrutinize Powell’s remarks and overall tone, paving the way for increased dollar volatility. Wall Street’s performance in the Fed aftermath could prove to be a reliable guideline in assessing the dollar’s next direction.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.