Fed Eyes Second Quarter Recovery, Expects Trump Fiscal Policy Will Expand Economy

Data supporting the second quarter recovery thesis is nonexistent. Four out of four of the recent hard data economic reports have been negative.

Soft data diffusion indexes do not look so hot either.

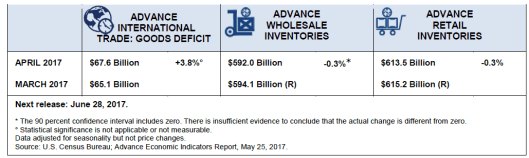

Earlier today the Census Bureau reported the trade deficit widened. The same report shows retail and wholesale inventories declined by 0.3% each.

Advance Wholesale Inventories

Wholesale inventories for April, adjusted for seasonal variations but not for price changes, were estimated at an end-of-month level of $592.0 billion, down 0.3 percent (±0.4 percent)* from March 2017, and were up 1.8 percent (±1.1 percent) from April 2016. The February 2017 to March 2017 percentage change was revised from up 0.2 percent (±0.4 percent)* to up 0.1 percent (±0.4 percent)*.

Advance Retail Inventories

Retail inventories for April, adjusted for seasonal variations but not for price changes, were estimated at an end-of-month level of $613.5 billion, down 0.3 percent (±0.2 percent) from March 2017, and were up 3.0 percent (±0.5 percent) from April 2016. The February 2017 to March 2017 percentage change was revised from up 0.5 percent (±0.2 percent) to up 0.3 percent (±0.2 percent).

Fed Economic Outlook

Let’s compare what’s actually happening to Fed expectations as noted in Minutes of the Federal Open Market Committee Meeting on May 2-3.

Staff Economic Outlook

In the U.S. economic forecast prepared by the staff for the May FOMC meeting, real GDP growth was projected to bounce back in the second quarter from its weak first-quarter reading. The staff judged that the weakness in first-quarter real GDP was probably not attributable to residual seasonality and that it instead reflected transitorily soft consumer expenditures and inventory investment. Importantly, PCE growth was expected to pick up to a stronger pace in the spring, which would be more consistent with ongoing gains in employment, real disposable personal income, and households’ net worth. In addition, the sharp decrease in the contribution to GDP growth from the change in inventory investment in the first quarter was not expected to be repeated. Beyond the near term, the forecast for real GDP growth was a little stronger, on net, than in the previous projection, mostly due to the effect of a somewhat lower assumed path for the exchange value of the dollar. The staff continued to project that real GDP would expand at a modestly faster pace than potential output in 2017 through 2019, supported in part by the staff’s maintained assumption that fiscal policy would become more expansionary in the coming years. The unemployment rate was projected to decline gradually over the next couple of years and to run somewhat below the staff’s estimate of its longer-run natural rate over this period; the staff’s estimate of the natural rate was revised down slightly in this forecast.

Second Quarter Reality

- Wholesale Inventories: Down 0.3% in April. March revised lower from 0.2% to 0.1%.

- Retail Inventories: Down 0.3% in April. March revised lower from 0.5% to 0.3%.

- Trade deficit in April widens by 3.8% with exports down and imports up: Trade Deficit Widens, Exports Weak: Economists Miss the Mark

- Tax Receipts: Federal Tax Receipts Running Below Expectations

- April New Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: New Home Sales Contract 11.4%: Sales Barely Up Year-Over-Year

- April Existing Home Sales: Spring Housing Flop: Existing Home Sales Decline 2.3 Percent, Inventory Issues Persist

- April Housing Starts: About that Strong April Recovery: Housing Starts and Permits Flop, March Revised Lower

- April Empire State Manufacturing Survey: Empire State Manufacturing Survey Turns Negative: Welcome News?

- April Retail Sales: Sales were at least positive (+0.4%), but they were well under economists projections: Retail Sales Disappoint Again: Department Stores Clobbered in 2017

Economists Conclude: Don’t Worry, It’s Transitory

Here was my interpretation after the housing reports yesterday.

Gotta love this quote: The staff continued to project that real GDP would expand at a modestly faster pace than potential output in 2017 through 2019, supported in part by the staff’s maintained assumption that fiscal policy would become more expansionary in the coming years

Say What? Yep, the Fed expects Trump fiscal policy to expand the economy.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc