The Fed disregards CPI in favor of the GDP deflator

Outlook: The top headline in the online FT is “Spread of Delta variant casts a shadow over Europe’s economic rebound--Economists fret over rising infections and return of pandemic restrictions.”

Funny, while many attribute last week’s whipsaw to Delta fear, you don’t see headlines like that in the major US newspapers. As for restrictions, aka lockdowns, forget it. Far too many in some states, including hotspot states like Missouri, would protest the guv’mint “taking away their freedom.” That the number of cases is up 47% in one week does not, apparently, deserve top headline notice.

Europeans are more sensible. ECB chief Lagarde, in an interview with Bloomberg, tempers optimism about growth and where the ECB can go with being “only ‘guardedly optimistic’ about the recovery prospects for the euro area with the Delta variant of the coronavirus posing a threat to efforts to return to normal life.” She did announce a revision to forward guidance at the next policy meeting on July 22, breaking with the tradition that the second meeting is always a dud. Still, she expects the current asset purchase program to run until “at least” March 2022.

As noted above, earnings season kicks off this week, along with G20 and trade meetings. G20 is going to cement that minimum tax proposal but we judge the probability of the US Congress going along at the same odds as a blizzard in Florida in August, so it will not be an FX factor (this time).

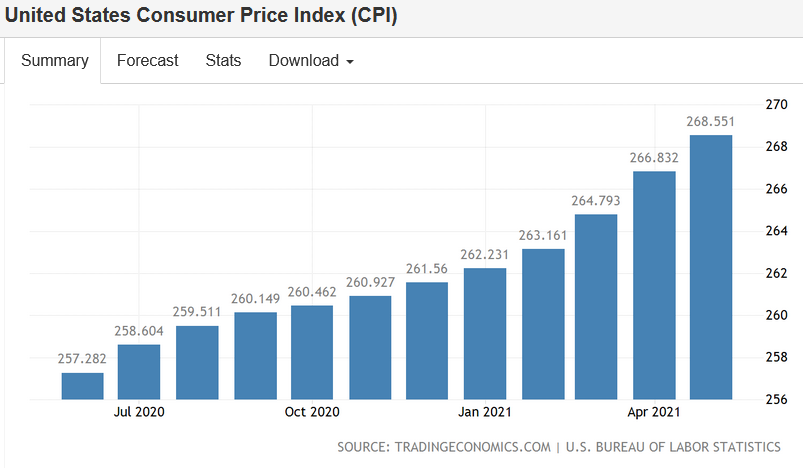

And it’s that time again for inflation data. We get CPI tomorrow. We also get PPI, industrial production, retail sales, and the Empire and Philly Fed manufacturing surveys. But the CPI is the headline winner, not least because the next day Powell deliver his semi-annual monetary policy report to the House Financial Services Committee (and to the Senate on Thursday). Powel has a tough row to hoe given higher numbers last time that can’t have come down much this time coupled with the Fed’s stance that they are transitory. Somebody in Congress might note that those wage gains to induce labor supply tend not to go down afterward—wages are “sticky” to the downside.

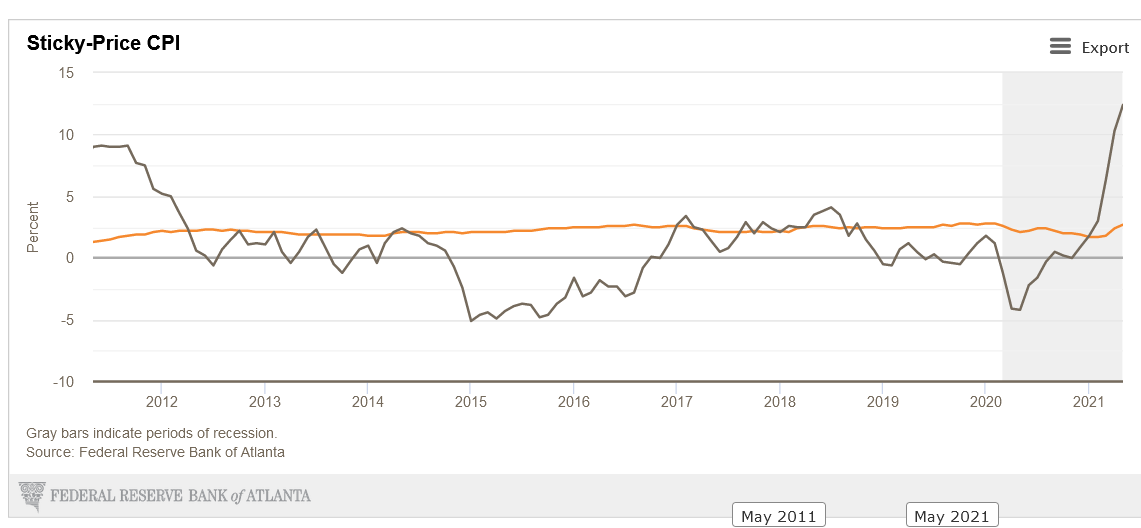

Even the Atlanta Fed’s “sticky price” calculations are not all that reassuring about the transitory nature of current inflation. According to the website, the latest update from June 10 is 4.5%. We get the July update right after the BLS reports CPI tomorrow.

“The Atlanta Fed's sticky-price consumer price index (CPI)—a weighted basket of items that change price relatively slowly—increased 4.5 percent (on an annualized basis) in May, following a 5.5 percent increase in April. On a year-over-year basis, the series is up 2.7 percent.

“On a core basis (excluding food and energy), the sticky-price index increased 4.3 percent (annualized) in May, and its 12-month percent change was 2.6 percent.

Bottom line, there’s no escaping that the US is experiencing inflation, and debate rages about whether is can go back down to the longstanding sub-2%. Debate also rages about whether the Fed is behind the curve. If inflation remains this high and unless Powell acknowledges it, there is some probability the bond market breaks ranks and gets another sell-off that lifts yields. This is probably dollar favorable but doesn’t’ count chickens.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat