Falling Employment Growth, Rising Recession Risk?

Slower employment growth is associated with rising recession probabilities and weaker GDP in the Post-Great Recession era, which often indicate the need for more monetary policy accommodation.

Is an Accommodative Monetary Policy in the Near-Term?

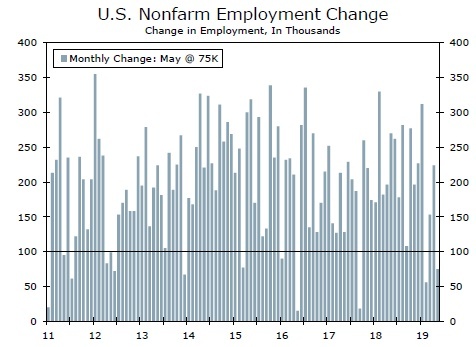

Job growth surprised to the downside in May as employers added only 75K jobs and the prior two months saw the largest downward net revision since 2010. The weakness in May was broad-based across industries including employment in education & health services, government payrolls and professional & business firms. The overall trend in hiring downshifted, which provides evidence of further weakening for growth.

In previous reports, we argued that there are seasonal distortions in the initial estimate of Q1 nonfarm payrolls data.1 Each year during the Post-Great Recession (PGR) era, one month of Q1 nonfarm payrolls typically has had a much larger or smaller change in payrolls than the other two months. We identify these outliers as "rogue-months."

Outside of the first quarter, unusually volatile employment data is uncommon although it is typically attached to weaker GDP growth (top chart). For example, in 2011-2019 outside of the first quarter, nonfarm payroll data dipped below 100K in 2011, 2012, 2013 and 2016, consistent with slower GDP growth in those periods.2

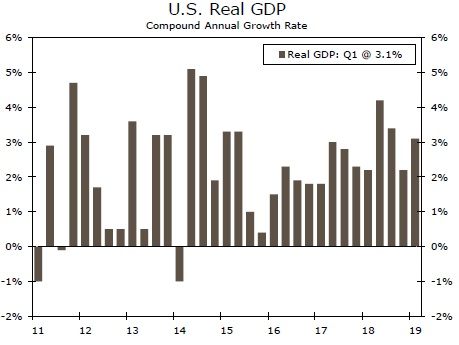

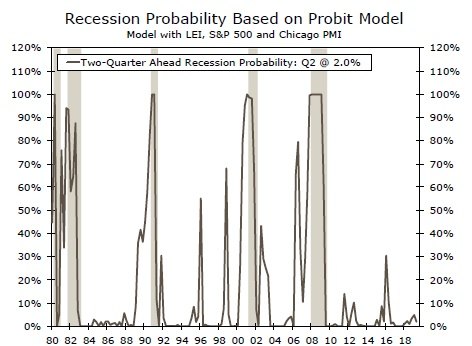

Additionally, weaker GDP growth rates are associated with higher recession probabilities. GDP growth figures fell into negative territory in Q1-2011 (-1.0%) and Q3-2011 (-0.1%). GDP growth also slowed in Q3-2012 and Q4-2012 (0.5% for each quarter). In 2016, the average growth rate edged down to 1.9%, the weakest in the 2014-2018 period (middle chart). The slowdown in GDP growth corresponded to heightened risk of recession from our Probit model. In 2011 our official Probit model predicted a double-digit chance of recession for the first time in the PGR era (bottom chart).3 Meanwhile, in 2012 and 2016 our model also predicted a double-digit risk of recession based on our predictors of the LEI, Chicago Employment Index and S&P 500.

Weakened employment and GDP growth is associated with rising recession probabilities, which often indicate the need for a more accommodative monetary policy. In November 2010 and September 2012 the Fed announced second and third rounds of the quantitative easing program as an effort to stimulate the weakening economy. In Q4-2015 the Fed projected three rate hikes in 2016, but ended up hiking only once at year-end in light of slower growth.

Overall, softer employment data and further weakening in the economy, could drive the Fed to be more cautious about the outlook for growth. We now expect two rate cuts later this year.

Author

Wells Fargo Research Team

Wells Fargo