Export flop causes US trade deficit to widen to six-month low

Summary

U.S. exports slipped by the most since pandemic-related lockdowns in 2020 in April, pushing the U.S. trade deficit to its widest in six months. Some one-off factors are to blame for the weakness, but the data continue to demonstrate an unusual volatility in trade flows. Net exports are tracking to be a meaningful drag on Q2 GDP growth.

Continued volatility in US trade

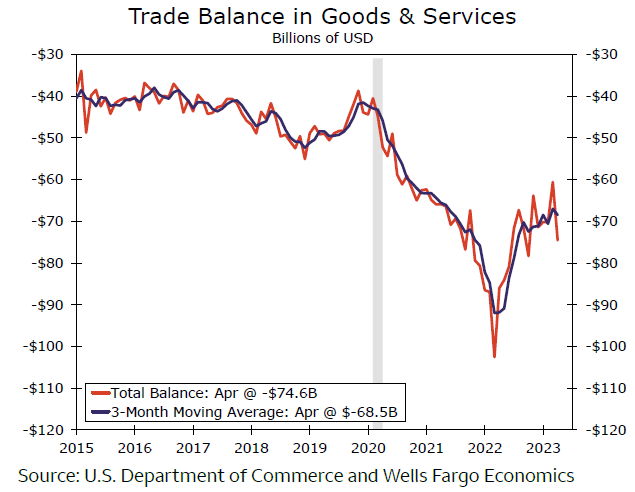

The U.S. trade deficit widened by a whopping $14.0 billion to $74.6 billion in April, more than reversing the $9.6 billion narrowing a month earlier. Monthly swings of this magnitude in the trade balance are normally very rare, but international trade flows continue to normalize from pandemic effects. Consider that in 11 of the past 20 months the trade balance has moved by $5 billion or more.

This month, a broadly weak outturn for exports is to blame. Exports fell $9.2 billion, or by -3.6% in April, while imports rose $4.8 billion (+1.5%). These data were largely foreshadowed by the previously released advance goods trade report, and position net exports to be a meaningful drag on second quarter growth. In the forecast update we published this morning, we estimate net exports will shave 1.4 percentage points off of topline growth in Q2 and these data do not materially change those expectations.

Export growth was broadly weak, with every major end-use category declining in April other than the volatile foods & feeds, which would have also posted a negative growth rate had it not been for a pop in soybean exports. Industrial supplies & materials posted the largest decline in exports, falling $6.1 billion (-9.4%) amid pullbacks in crude oil and fuel oil specifically. These two components accounted for over half of the industrial decline, but still only 11 of 47 underlying industrial categories saw exports rise during the month, demonstrating broad weakness in April. Capital goods exports slipped 0.7% and auto exports were down 0.2%. Consumer goods exports also demonstrated weakness broadly, without any one category accounting for the 7.6% decline in exports in April.

Imports broadly increased during the month, and auto imports posted the largest increase of $2.0 billion, signaling a continued normalization in supply. But beyond autos, one-off factors explain some of the strength. A $1.7 billion increase in cell phones, for example, accounted for nearly all of the $1.8 billion increase in consumer goods imports, with the remaining categories pretty much washing each other out. Similarly, the rise in finished metal shapes and non-monetary gold more than explain the industrial supplies & materials increase last month. Capital goods imports posted an only modest gain of $209 million.

Beyond goods trade, we continue to see some normalization in services. The trade surplus in services rose for the third consecutive month in April, up $573 million to $21.6 billion. Services exports rose 0.2%, the 15th consecutive monthly increase amid a normalization in the service sector. Imports of services have been a bit more volatile, and slid 0.6% in April. The U.S. has historically run a surplus in services trade, but even with the recent normalization, the surplus still remains about 13% below pre-pandemic levels.

All told, we expect trade flows to remain a bit volatile in the months ahead. In considering our expectation for underlying U.S. resilience to delay recession until the start of next year, we've increased our expectations around imports in the near-term, while also expecting slightly weaker export growth amid a stronger U.S. dollar.

Author

Wells Fargo Research Team

Wells Fargo