Expect a steady rather than spectacular Eurozone recovery

The Eurozone economy showed some resilience in late 2020, with the decline in Q4 GDP less than generally expected. That said, the economy still faces near-term challenges with lockdowns restricting activity and the distribution of vaccines gradual so far. As a result, we expect Eurozone GDP to contract further in Q1-2021.

The medium-term prospects for the economy are somewhat mixed. Household finances remain sound, meaning the Eurozone economy should be well-positioned for a consumer recovery once the economy fully reopens. However, the gradual rollout of vaccines as well as gradual implementation of further fiscal support measures suggest the pace of a medium-term recovery will not be especially robust.

A moderate Eurozone recovery suggests the European Central Bank will maintain an accommodative monetary policy stance for an extended period and that its rhetoric will generally tilt more dovish than hawkish. At this time, however, we do not anticipate any further monetary easing from the central bank.

Overall, we do not view the economic growth and policy mix as especially favorable for the euro. As a result, we recently revised our forecast for the EUR/USD exchange rate modestly lower and still view risks to that forecast as tilted to the downside.

Eurozone Economy Set for Another Decline in Q1

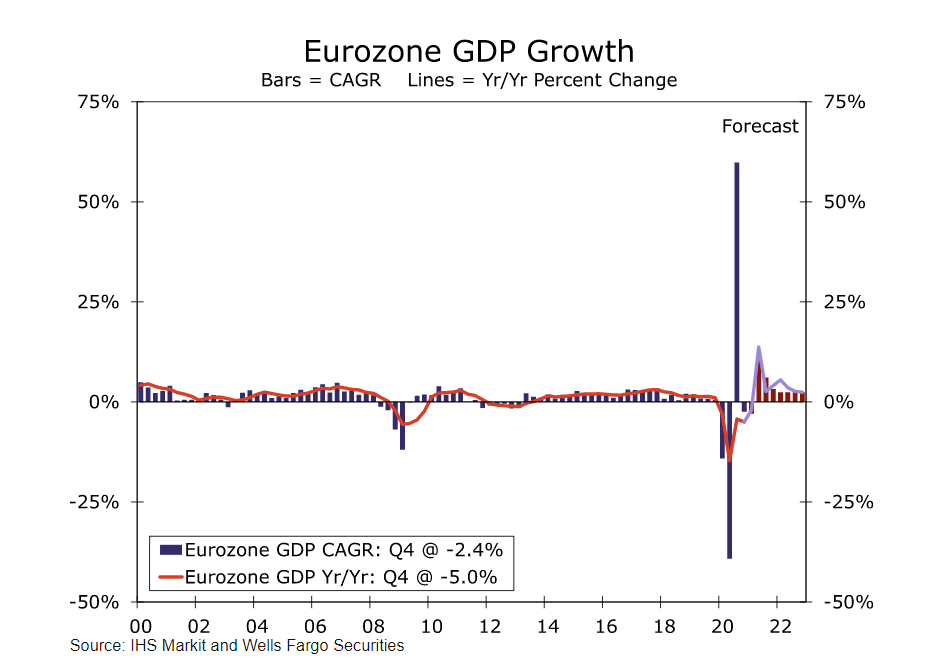

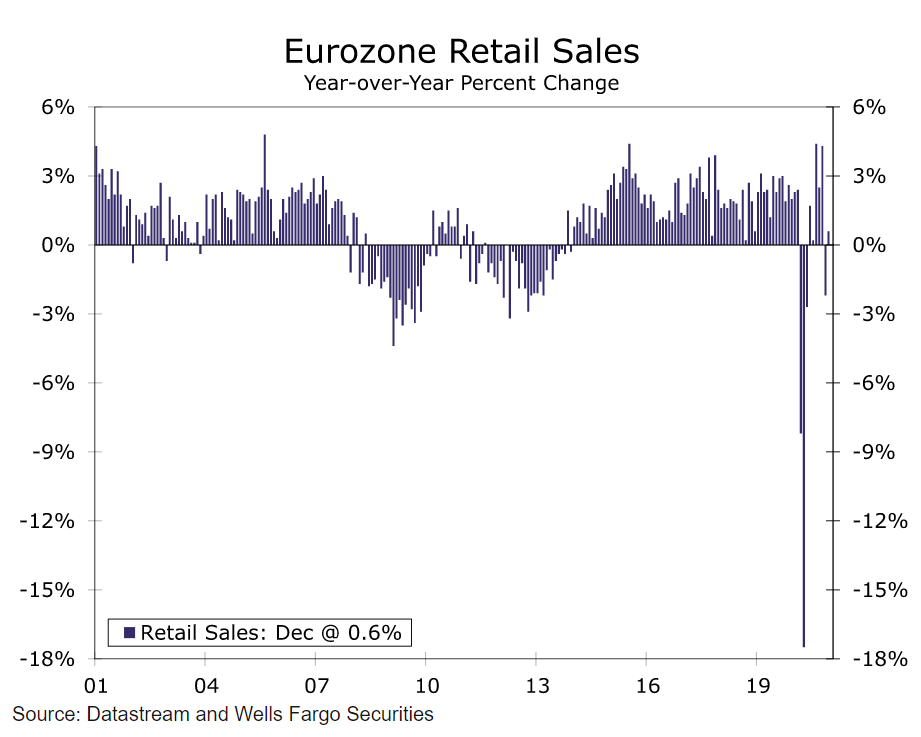

The Eurozone economy remained relatively resilient at the end of last year, as the economy shrank less than expected; however, further economic softness followed by a slow recovery appears likely this year. In the fourth quarter of 2020, Eurozone GDP declined 0.6% quarter over quarter, less than the 0.7% decline initially estimated, following the sharp rebound in the third quarter. The overall Eurozone economy shrank 6.8% for full-year 2020 due to the COVID pandemic. Heading into 2021, the Eurozone economy is likely to experience another contraction in Q1, with the decline expected to be somewhat steeper than in Q4. Recent growth and survey data have been mixed as the pandemic and associated lockdown restrictions continue to take a toll on the economy. Retail sales rebounded less than expected in December, rising 2.0% month over month, after a sharp 5.7% drop in November. The increase in December's print was due in part to a surge in textiles, clothing and footwear sales, which rebounded 12.4% over the month, while automotive fuel in specialized stores also posted a solid increase, rising 5.1%. Other activity data were soft. December industrial output declined 1.6% month over month, more than expected, as production of capital goods fell 3.1% and non-durable consumer goods declined 0.6%.

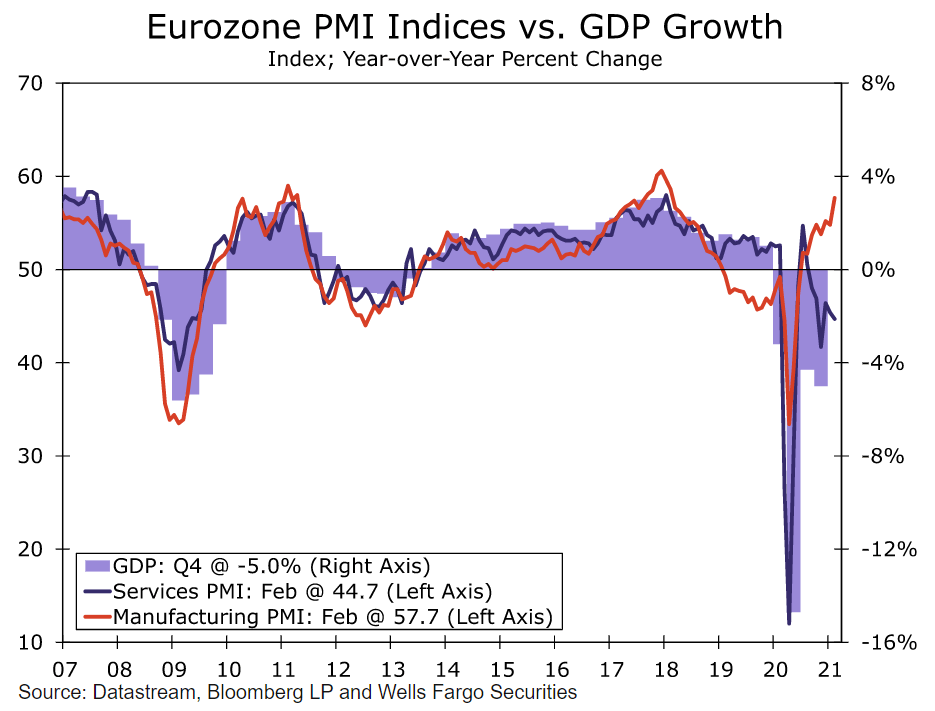

Survey data for February were also mixed and suggest the economy has started 2021 on a weak footing. The Eurozone composite PMI suggests business activity across the region declined for a fourth consecutive month in February, in particular driven by COVID restrictions weighing on the service sector. The services PMI weakened further to 44.7, a three-month low. In contrast, the manufacturing PMI rose to 57.7—a 36-month high—as inflows of new business pushed activity higher. Manufacturing growth was especially strong in Germany, although the French manufacturing sector slumped further.

Eurozone Lagging Its Peers on COVID Vaccination

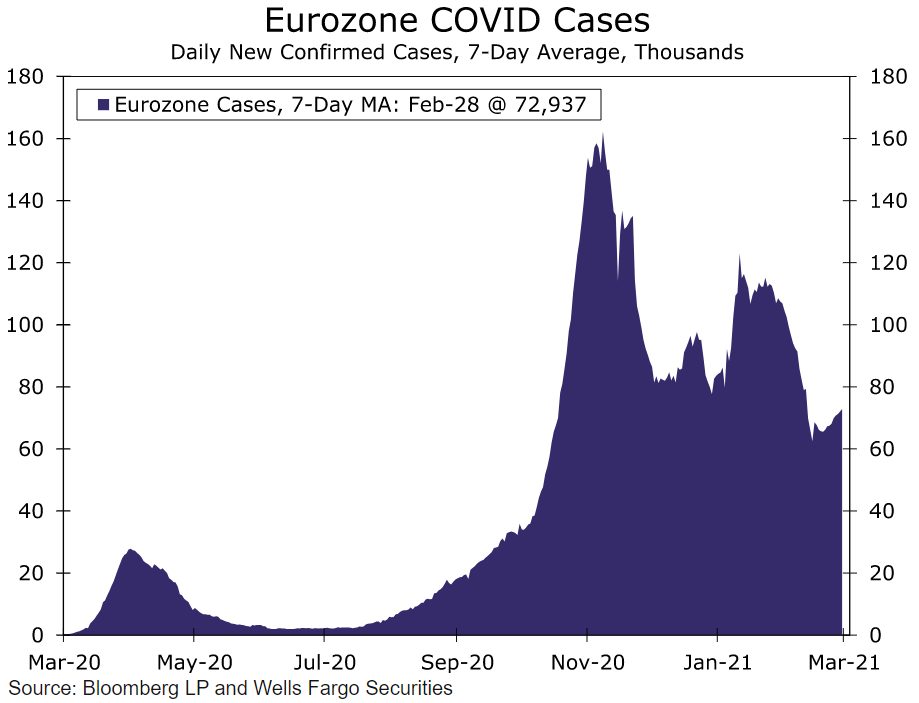

Much like the rest of the world, the Eurozone economy continues to be influenced by and sensitive to the COVID pandemic. Although new COVID cases have fallen dramatically since the start of the year, lockdowns were extended into early 2021, which should have a negative effect on growth in the first quarter. Notably, Germany and France reintroduced lockdown measures, and recent government comments suggest that despite the decrease in cases from its recent peak, the outbreak is still likely to hamper the ability to ease COVID restrictions. German Chancellor Angela Merkel warned of a third wave of COVID across Germany and noted caution with reopening schools and businesses. Meanwhile, France introduced new COVID restrictions for the area around its common border with Germany. France has also begun to increase local restrictions, with the area around Dunkirk temporarily putting in place weekend restrictions, while Moselle called for a local lockdown.

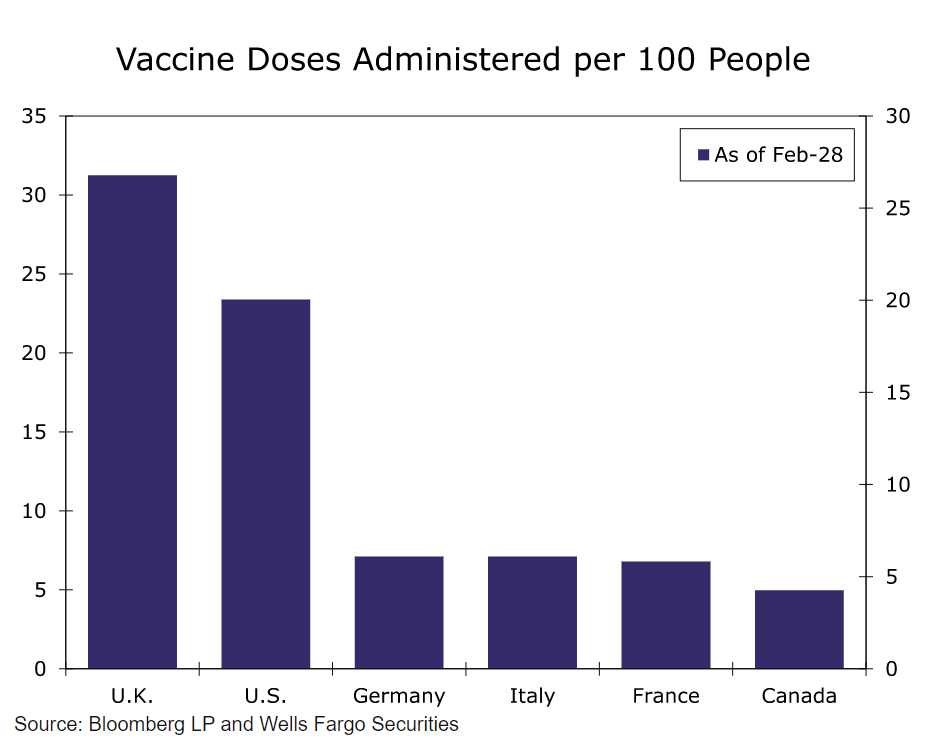

In addition, vaccination programs have so far been rolled out at only a gradual pace, which might restrain the timing and speed of medium-term recovery. In particular, Germany's, Italy's and France's vaccination programs lag that of the United Kingdom and United States, due in part to problems in vaccine production. The European Union also opted for a centralized EU approach and did not start its vaccination campaign until Dec. 27, compared to the United Kingdom which began its vaccination rollout on Dec. 8. In addition, some recent surveys suggest that the French population is the most hesitant about getting a vaccine if it were available, noting that French residents are most worried about the side effects. The European Union has only secured 2.6 billion vaccine doses from six vaccine developers; however, only three vaccines are authorized for use in the EU. EU officials are also still conducting exploratory talks with two other vaccine developers regarding the purchase of about 260 million more vaccine doses. Although the EU's vaccine rollout is well-behind its peers, we expect the economic recovery to pick up steam once the speed of vaccinations picks up and COVID cases continue to retreat.

Eurozone Household Finances a Potential Economic Positive

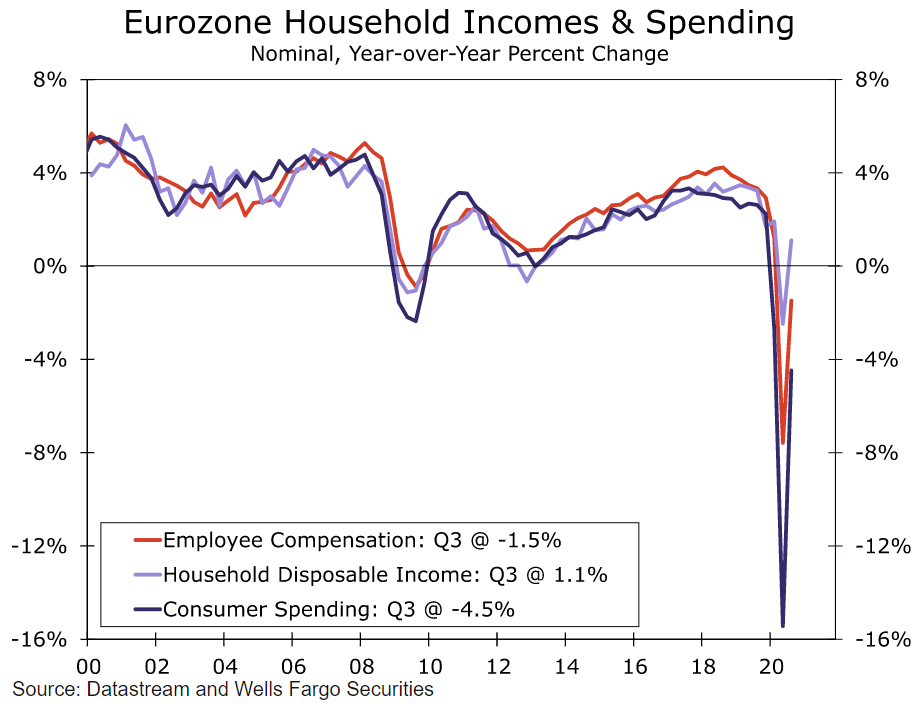

While the gradual pace of vaccinations may be an influence that constrains the pace of medium-term economic recovery, a more constructive factor is the relatively sound household finances that should be supportive of a consumer rebound as the economy reopens. The latest official data on Eurozone household incomes are for Q3-2020. Those figures show that, for the Eurozone region in aggregate, Q3 household disposable incomes rose 4.0% quarter over quarter, following a 3.2% decline in Q2. That said, the increase in Q3 (nominal) consumer spending was even larger, with a rise of 13.9% quarter over quarter.

There is only partial data relating to Q4 incomes and spending so far, though the information that is available suggests that incomes rose further while consumer spending potentially declined. So far, Germany and France, the Eurozone's two largest economies, have published Q4 household disposable income figures. Germany reported a rise of 0.3% quarter over quarter, while French household disposable income rose a larger 1.5%. For Spain, data on employee compensation (as opposed to total household income) are available and show a Q4 increase of 2.2% quarter over quarter, while we suspect Italy's Q4 employee compensation likely rose as well. Based on these results for the region's four largest economies, we believe another sequential gain in Eurozone Q4 household disposable income is likely.

Information on Eurozone Q4 consumer spending is also partial but, we believe, probably signals a decline in consumer spending for the quarter. In particular, Eurozone real retail sales fell 1.5% quarter over quarter in Q4, potentially suggesting a decline in broader consumer spending is also likely. At a national level, Q4 consumer spending fell 3.3% quarter over quarter in Germany and 5.4% in France. If, as seems likely, Q4-2020 saw a rise in household incomes and a decline in consumer spending, that would mean a further increase in the household saving rate from its already elevated level of 17.4%. Accordingly, we view the overall state of Eurozone household finances as well-positioned to support a consumer recovery as the economy gradually and fully reopens.

European Central Bank Takes It Easy on Monetary Policy

Clearly, there are both positive and negative fundamentals influencing the medium-term economic outlook. Another important factor to consider in terms of the Eurozone outlook (for both the economy and currency) is economic policy settings. In recent months, there has been more attention on the monetary policy than fiscal policy front. While monetary policy developments have been somewhat mixed, we would argue they have been dovish overall.

The last policy action taken by the European Central Bank (ECB) was in December when, among other things, the ECB increased the purchase envelope for its Pandemic Emergency Purchase Program (PEPP) by €500 billion to €1.850 trillion. The ECB also extended the duration of that purchase program until at least the end of March 2022. The comments surrounding that bond purchase action were somewhat mixed, with the ECB saying that the purchase program might not be used in full, but equally that the program can be recalibrated if needed to maintain favorable financing conditions.

More recent comments from ECB policymakers have, in our view, generally been tilted toward the dovish side. ECB President Lagarde has, in various forums, stressed that accommodative monetary policy remains essential and also highlighted the importance of maintaining favorable financing conditions. Even more recently, other ECB policymakers have suggested the central bank might need to lean against a premature rise in bond yields. Lagarde said the ECB is "closely monitoring" bond yields, while ECB policymaker Schnabel said the central bank may have to boost monetary support for the economy if rising government yields hurt growth.

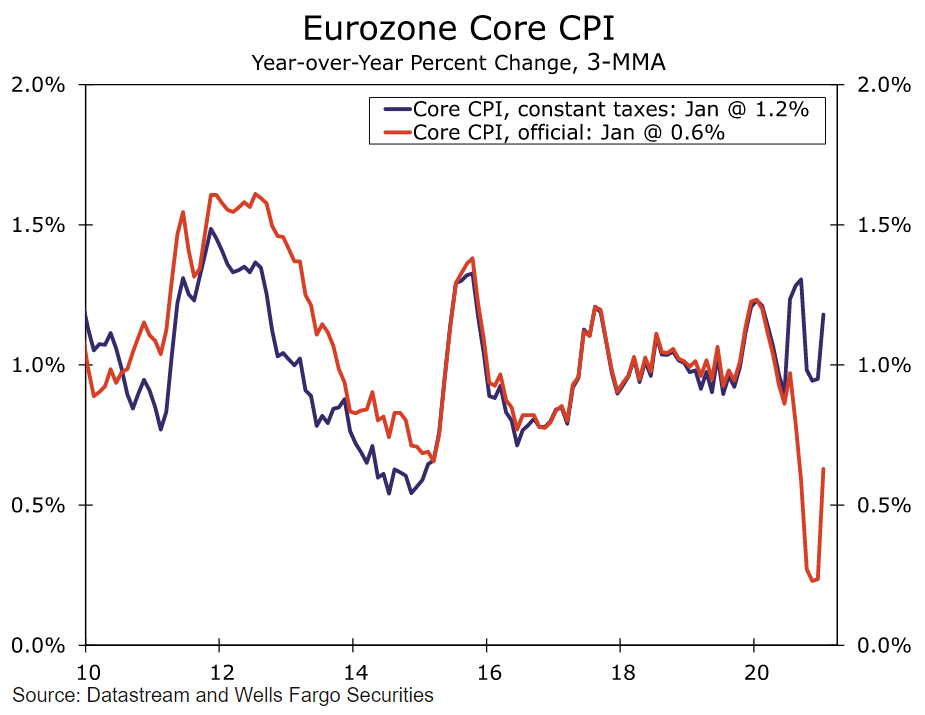

It is not clear to us the ECB will "walk the walk"—that is, further monetary easing is possible, but it is not our base case. While inflation trends are subdued, they are not dangerously low, in our opinion, such that there is a significant risk of persistent or malignant deflation. In particular, a temporary VAT tax reduction in Germany that went into effect last July and ended in December temporarily depressed inflation readings. The chart below shows Eurozone core CPI inflation on a three-month average basis to remove some noise. While the official core CPI readings have been especially low, excluding the effect of any tax changes, core CPI inflation trends have remained much closer to 1% year over year. Thus, given we do not expect an extended relapse in Eurozone economic growth or a sustained move into deflationary territory, we do not foresee further ECB easing at this time.

What is clear however is that the European Central Bank is currently and will likely continue to "talk the talk." Generally, ECB policymaker comments have taken on a perceptibly dovish bias, a trend we suspect will persist. Those dovish comments from the central bank are likely, we think, to act as a drag on the euro exchange rate versus the U.S. dollar.

Fiscal Policy Support: Good Enough, but Could Be Better

The other key policy theme, in terms of considering the Eurozone economic outlook, is developments on the fiscal policy front. By their own historical standards, Eurozone governments were active in 2020, with the International Monetary Fund estimating in its January 2021 Global Fiscal Monitor that extra spending and foregone revenue amounted to around 7.7% of GDP. While that was clearly a sizable fiscal response, it was still less forceful than seen in other major economies, such as the United States, Japan or Canada.

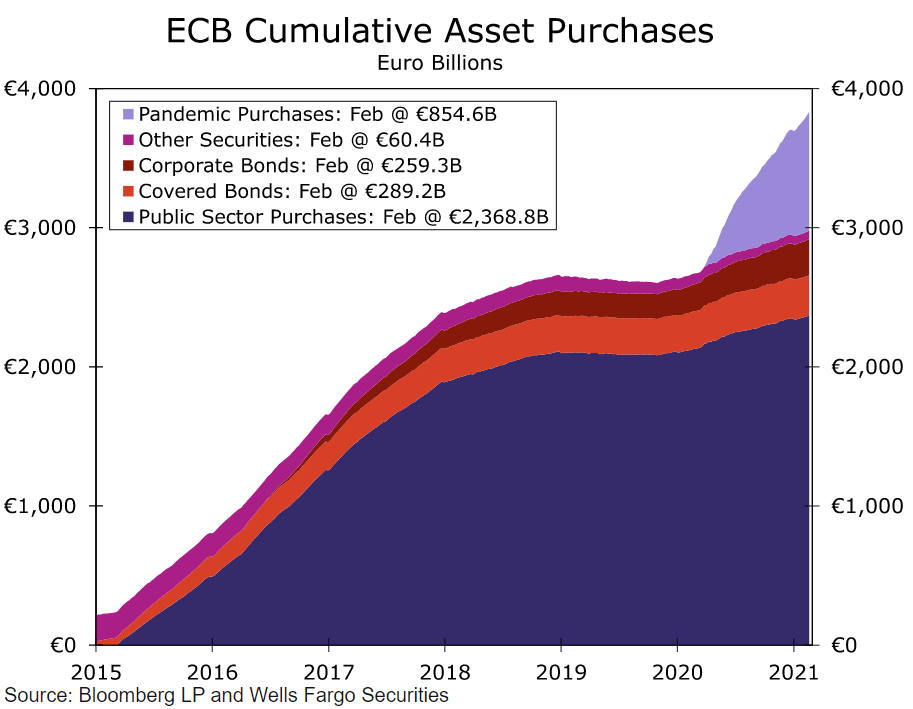

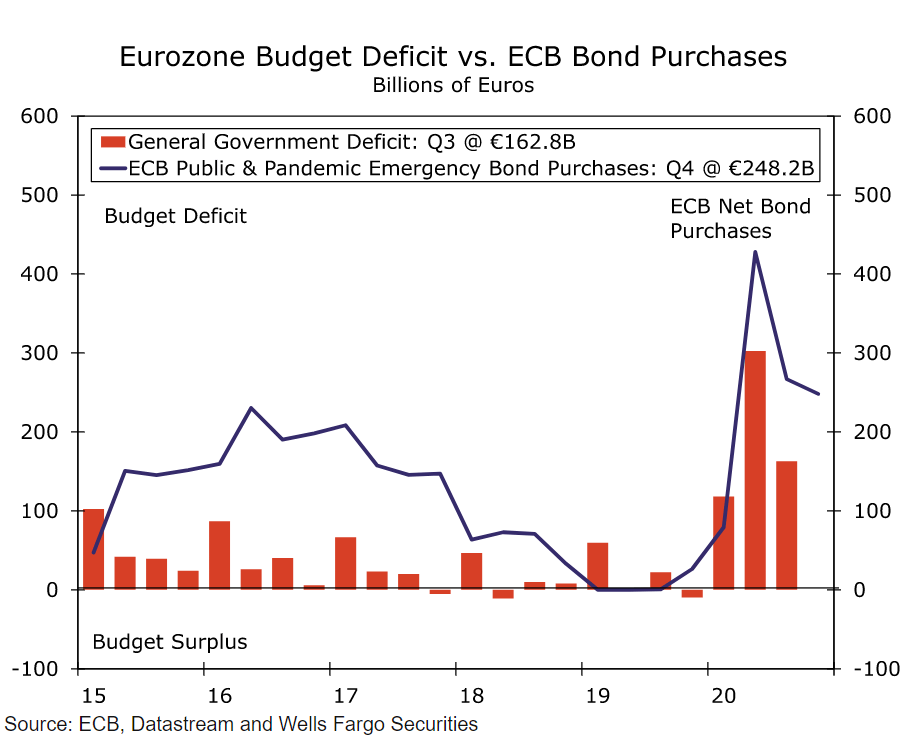

Assessing fiscal developments first from a financial perspective, we expect that even with the sharp widening in the Eurozone budget deficit and resulting increase in debt issuance, Eurozone government bond markets should remain quite stable overall. The chart at right shows the Eurozone general government budget deficit (a proxy for the region's borrowing or financing needs) compared to the ECB's public sector purchases under the Public and Pandemic Emergency Bond Purchase Programs. Even with the large increase in the deficit in 2020, the approximation for the region's financing needs has been comfortably exceeded by the ECB's bond purchases. As a result, we anticipate that even historically more unsettled peripheral government bond markets, such as Italy or Spain, will likely remain stable. Indeed, following recent political jitters surrounding the collapse of the Italian government, the appointment of former ECB President Mario Draghi as Italy's new Prime Minister saw the spread between Italian and German 10-year government bond yields narrow to less than 100 bps.

However, the relative stability of bond markets perhaps also highlights that the Eurozone region's fiscal response might not have been quite as forceful as desirable. As we highlighted above, the Eurozone fiscal response has not been as noticeable as for some other major economies. In addition, the implementation of the region-wide European Recovery Fund (amounting to €750 billion, including €390 billion in grants and €360 billion in low cost lending) has been relatively gradual. European governments have until the end of April to submit detailed spending plans, while initial disbursements from the Fund seem unlikely until the second half of the year. The gradual implementation of the region-wide fund, as well as a reduced frequency of national level fiscal measures announced in recent weeks and months, is another factor that could limit the robustness of the Eurozone's medium-term economic rebound.

Expect a Steady Rather Than Spectacular Eurozone Recovery

Overall, our assessment points to a rather mixed outlook for the Eurozone economy. Despite some near-term challenges, we believe the risk of a renewed period of extended decline is unlikely. Relatively sound household finances should underpin the economy and support recovery, although the gradual rate of vaccine distribution to date means that recovery might not be especially robust. Moreover, the moderate growth outlook, in part stemming from gradual vaccine rollout and a gradual implementation of fiscal support, likely means the ECB will maintain an accommodative policy stance, and the central bank's rhetoric will be more dovish than hawkish. We do not view this mix of economic growth and economic policy as especially favorable for the euro. Indeed, these are among the factors that saw us revise our EUR/USD exchange rate forecast modestly lower in our February International Economic Outlook, and why we believe the risks to that forecast probably remain tilted to the downside.

Author

Wells Fargo Research Team

Wells Fargo