Eurozone: The dichotomy between manufacturing and services

Based on the PMI data and the European Commission business surveys, it seems that in the Eurozone, industry is clearly slowing down, demand is softening and labour market bottlenecks have eased somewhat. In combination with input prices that are down, this should lead to an easing of output price inflation. In services, the picture is different. Hiring difficulties remain a big constraint on activity, momentum in terms of activity and orders has improved. Input price and output price inflation has eased only slightly. Such a dichotomy complicates the task of the ECB: ongoing strength in services would imply that past rate hikes didn’t yet have a significant impact and would justify more tightening, but this would only make things worse for the industrial sector. Eventually, such a negative dynamic should spill over to services.

Over the course of a business cycle, developments of the major sectors -industry, services, trade, construction- tend to be highly correlated, but in the short run divergences may exist that complicate the assessment of the cyclical environment and outlook. At the current juncture, we are in this type of situation. According to the ECB’s latest Economic Bulletin, “the manufacturing sector is working through a backlog of orders, but its prospects are worsening. Meanwhile, the services sector is growing more strongly, especially owing to the reopening of the economy.”

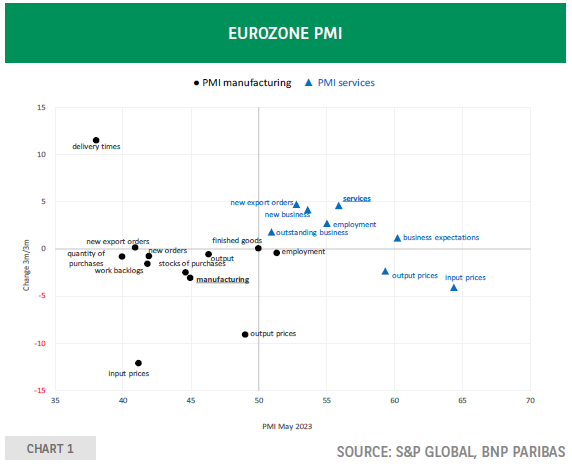

Chart 1 visualises this dichotomy. It shows the level of the purchasing managers’ indices and their momentum. The data for services are almost exclusively in the upper right quadrant whereas those for manufacturing are predominantly in the lower left quadrant1. It is as if both sectors are worlds apart. Most of the data for manufacturing are below 50, which implies that a majority of companies report a decline compared to the previous month. Employment is an important exception, and the hiring plans of companies illustrate the resilience of the labour market. Moreover, series like new orders, backlogs and the manufacturing PMI in general display negative momentum: the latest 3 months have a lower score than the previous 3 months.

The situation is very different for services. All data are above 50 and except for input and output prices, momentum is positive: the recent numbers are better than those in earlier months. Another striking difference concerns the price data. A clear majority of services companies report rising input prices and even more companies are raising their sales prices.

Based on the momentum data, the situation has hardly improved in recent months. In manufacturing on the other hand, momentum has been very negative for output prices and even more so for input prices. Only slightly more than 40% of survey participants still report rising prices. For output prices, the number is higher but has also dropped below 50%.

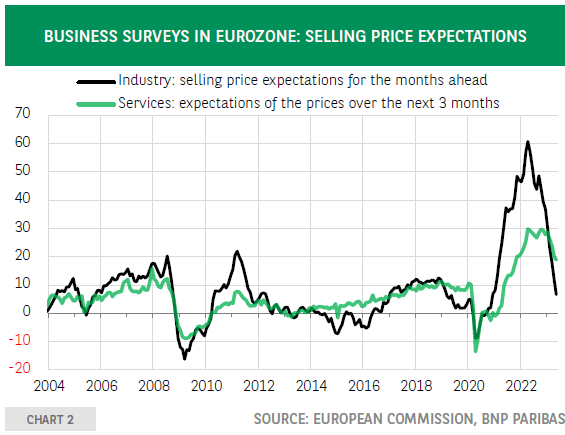

The contrasting price dynamics in manufacturing and services remind us of the difficulty of gauging the pace of disinflation. The conclusion is similar when looking at the price expectations data from the European Commission’s business survey (chart 2).

Both industry and services show a declining trend but whereas the former has reached a level that is in line with the historical experience, for services this is not yet the case, which points to ongoing inflation pressure in this sector. Recruitment difficulties and the impact on wages may play a role.

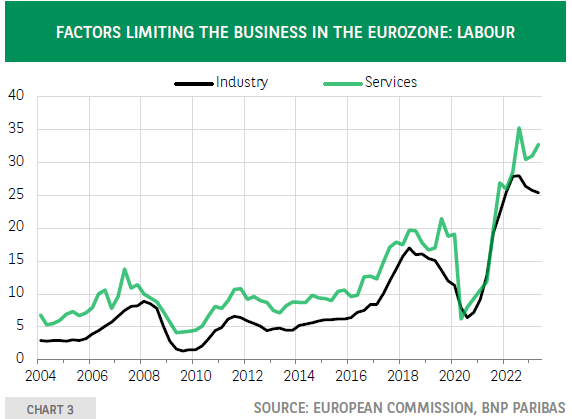

Chart 3 shows that labour shortages remain an important factor weighing on production in the services sector and the situation has worsened again in recent quarters. In industry however, the constraint of labour shortage has eased somewhat, although it remains high from a historical perspective. In industry, weak demand is increasingly mentioned as a constraint on output, but the level remains low. In services, the assessment of demand has been stable in recent quarters and, as in industry, the level remains low.

Based on the PMI data and the European Commission survey, it seems that industry is clearly slowing down, demand is softening and labour market bottlenecks have eased somewhat, which in combination with input prices that are down should lead to an easing of output price inflation. This is also clearly what companies in this sector expect. In services, the picture is different. Hiring difficulties remain a big constraint on activity, momentum in terms of activity and orders has improved. Input price and output price inflation has eased only slightly.

Such a dichotomy complicates the task of the ECB: ongoing strength in services would imply that past rate hikes didn’t yet have a significant impact and would justify more tightening, but this would only make things worse for the industrial sector. Eventually, this negative dynamic should spill over to services. The ECB recently reported that its contact with large, nonfinancial companies show subdued activity in the transport sector “with activity in road haulage and shipping described either as declining or as stabilising at somewhat lower levels than a few quarters ago.” However, demand for travel, tourism and IT services is growing strongly2. It looks as if in services, the growth slowdown will be a slow process.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.