Eurozone money markets: ECB cuts come to an end but the balance sheet shrinks further

The European Central Bank (ECB) easing cycle could end soon, which has helped bring down volatility of some money market spreads. The balance sheet continues to shrink, and while still a long process, the future will likely hold more upside pressure for longer-term money market funding spreads.

ECB outlook: One more cut could still come

The ECB kept rates on hold in July, and markets are no longer fully pricing another cut from the ECB in this cycle. At the peak, the curve prices less than 20bp of easing – but only next year.

Our economists note that the US-EU deal is far from ideal, but it does provide a degree of stability for the time being. They do not expect an economic contraction in the second half of 2025 and have slightly upgraded their growth forecast for this year and next. While this has complicated the call for one further ECB rate cut in September, falling inflation still narrowly argues in favour of one more move, delivered before the fiscal impulse out of Germany gains traction.

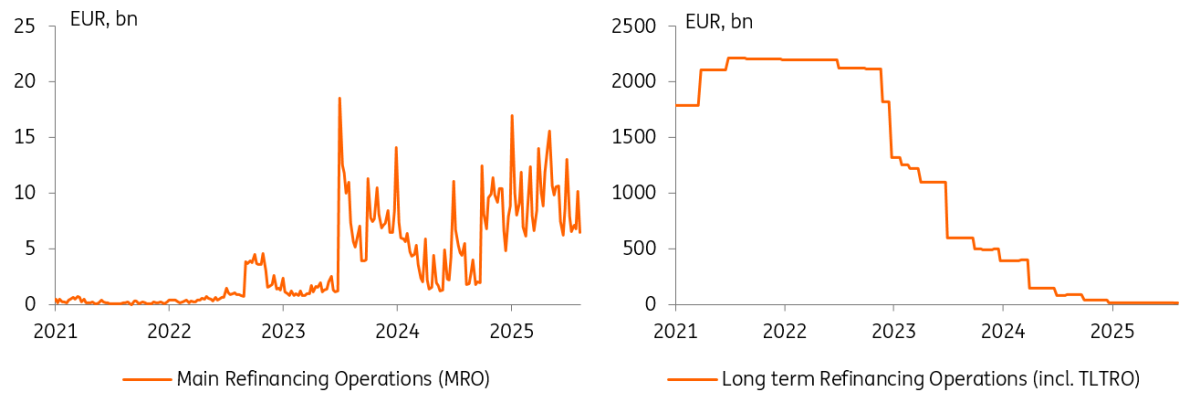

Excess reserves inch lower but ECB liquidity operations see little pickup

Excess liquidity in the banking system continues to trend lower and now stands at just above €2.6tr. There has been no material increase in banks’ recourse to the ECB’s liquidity operations. The weekly main refinancing operations (MRO) come in around €6bn to €10bn and the 3m long-term refinancing operations (LTRO) at below €13bn in total; amounts that are still negligible relative to the overall amount of excess liquidity.

It is still relatively more attractive to borrow in the market, and the last ECB survey of monetary analysts conducted ahead of the July meeting does not indicate the situation will change anytime soon. Banks expect the MRO take-up to have increased to €30bn and the LTRO to €50bn by the end of next year. Taking into account the bond portfolio projections, excess liquidity would have just fallen below €2tr. This is assuming constant autonomous liquidity factors that can also influence banks’ liquidity needs.

That said, the Eurosystem estimates that excess liquidity will have fallen to €1.5tr by the end of 2027. This is where many market observers expect excess liquidity levels to stabilise in the long run. Since the ECB’s bond portfolios would continue to shrink at that point, the idea is that regular liquidity operations would start to see more pickup to offset that effect. Then, at some point, the ECB would introduce structural liquidity operations.

No sign of greater demand for ECB liquidity

Source: ECB, ING

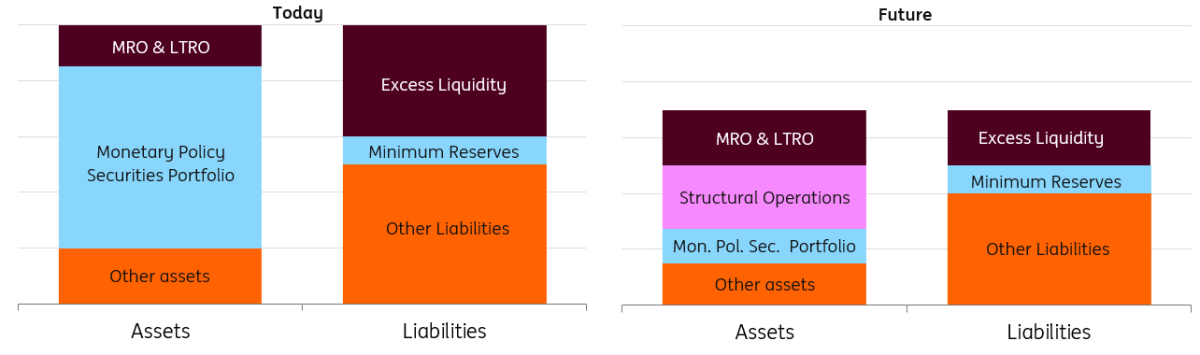

The future of the ECB balance sheet according to the Bundesbank

In its June monthly report, the Bundesbank outlined some of its thinking around the future composition of the ECB’s balance sheet. Remember that the ECB’s March 2024 review of the operational framework outlined the transition to a system where the level of excess liquidity is determined by banks’ demand.

The Bundesbank suggests that after an increase in regular open market operations, the ECB should first introduce structural refinancing operations. These would be variable-rate tenders with limited allotment volumes, rather than today’s fixed-rate full allotment tenders. Only at a later stage would a structural bond portfolio be introduced. The thinking is that the structural operations largely cover bank liquidity needs stemming from autonomous factors and minimum reserve requirements, while the regular operations would cover banks’ demand for excess liquidity. The upshot from this operational design is that the ECB would provide only a softer cap on term liquidity beyond three months.

Current and future stylised ECB balance sheet

Source: Bundesbank June Monthly Report, ING

Drivers of liquidity demand and the recourse to ECB liquidity operations will be banks' individual business models and financing costs. Regulatory factors such as liquidity regulation will also determine the relative attractiveness of the ECB operations.

And with a view to regulation determining demand, the latest data for the first quarter of 2025 by the ECB shows that banks have reduced their aggregate Liquidity Coverage Ratio (LCR) ratio from 158% to 156.25%. While this was down more to rising net outflows, with liquidity buffers even increasing, it could signal some openness by banks to normalise their LCR levels from currently still-elevated levels. Separately, more granular data from the European Banking Authority on the composition of liquidity buffers shows that the share of central bank reserves remains on a declining trend, making up 47.3% in the first quarter (-0.4 percentage points).

Recall that LCR levels had been inflated by the ECB’s injection of excess reserves into the banking system. But as excess reserves began to decline again, banks had initially chosen to maintain the higher LCR levels and replaced the central bank cash in their buffers with other high-quality liquid assets.

All things equal, a prospective decline in LCR ratios could lower the stable level of excess reserves that the banking system operates in the future and thus push back the timeline for a pickup in (structural) liquidity operations. We would still expect the ECB to outline its designs in more detail after the review it has flagged for 2026.

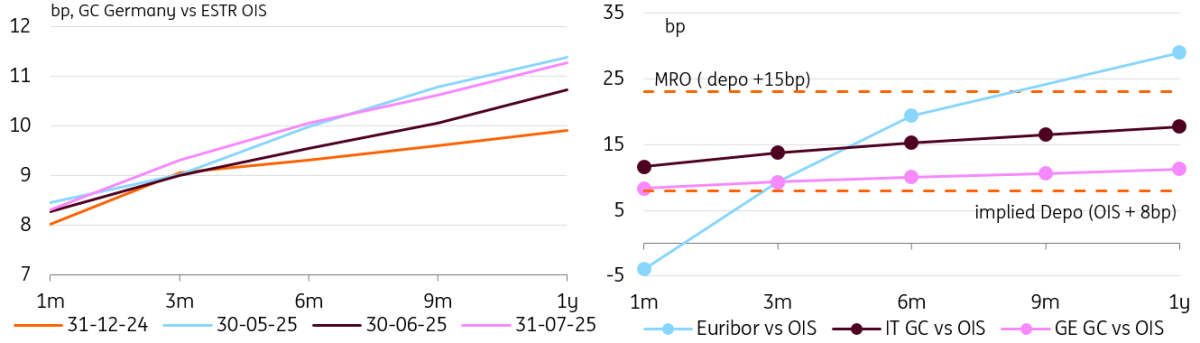

Repo markets stabilise and prices slightly above the implied deposit facility rate

Repo market volumes underpinning the Stoxx GC pooling overnight repo indices have receded from their peaks as rate levels fluctuate around the ECB’s deposit facility rate.

The German as well as the Italian GC government collateral curves versus (Overnight Index Swap) OIS were slightly steeper at the end of July, but not at their steepest levels for the year. Germany had seen its steepest month-end in May.

Market funding options still cheaper than the ECB

Source: ING

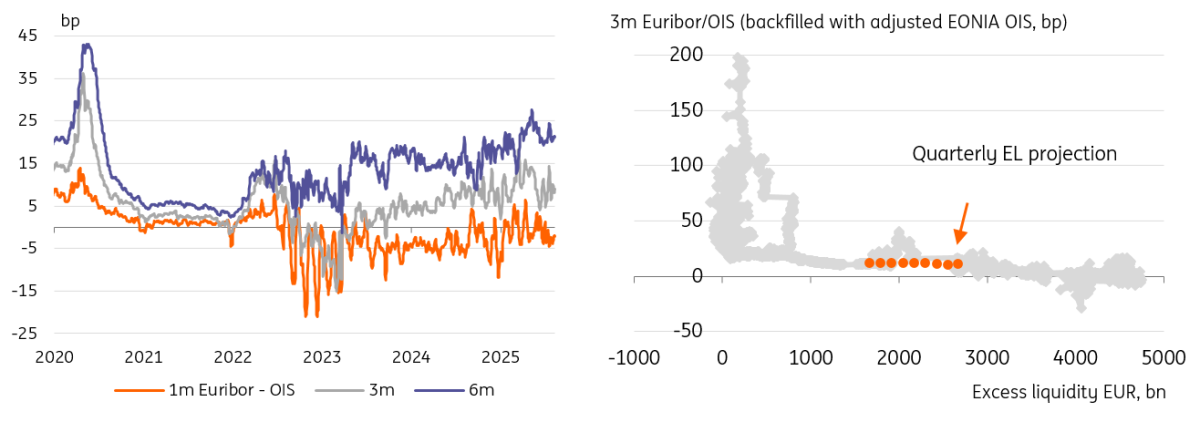

Unsecured funding remains more attractive than ECB operations

Short-dated unsecured rates remain below the ECB deposit facility rate, although the overnight Euro Short-Term Rate (ESTR) is showing a subtle upward trend now averaging slightly less than 8bp below the depo rate. 1m Euribor is more consistently below the 1m ESTR OIS rate by around 3bp on average, lower than the virtually flat average over the first half of the year. That higher level seemed more down to a lag effect of the Euribor rate that is now less relevant since the ECB has paused cutting rates.

The spread of 3m Euribor over ESTR OIS has become somewhat more volatile even as the ECB has paused, but it is still the OIS-leg of the spread that drives fluctuations with Euribor more stable. The spread averaged around 9bp since the end of June, with market pricing seeing this spread widening only marginally over the next year to 12-13bp. This market view has remained relatively stable and reflects expectations that the gradual decline of excess reserves will have a limited impact in the near to medium term.

The longer 6m Euribor rates have occasionally spiked above the implied MRO rate (at around 23bp MRO/ESTR = 8bp Depo/ESTR + 15bp MRO/Depo), but now mostly settle just below at around 21bp above ESTR/OIS, indicating that the ECB operations do offer a soft cap to the market pricing. The 2y IRS/OIS basis has largely remained in the 23bp to 25bp area over the past quarter.

Euribor-OIS spreads with structural upwards pressure is still seen as some time away

Source: Refinitiv, ING

ECB data on EUR unsecured short-term funding by euro area banks shows an increase over May and June to €377bn, the highest outstanding amount since the start of the data set in 2021. To a large extent, the EUR increase reflects a shift away from short-term funding via foreign currencies.

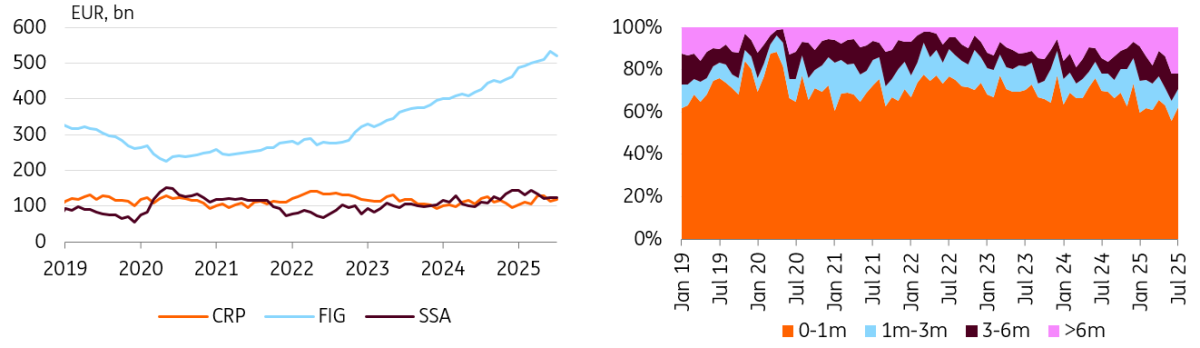

A look at the outstanding EUR commercial paper by the broader financial sector shows a more steady increase and continuation of a trend that accelerated already in 2023. From a low of €224bn in 2020, the outstanding CP volume has almost doubled to €530bn by the end of June with only a small drop to €520bn over July. The backdrop for the longer trend was the maturities of the ECB TLTROs, the last of which matured last December. The trend to increased CP financing has continued and what the past half-year has shown within this trend was an increasing reliance on longer-dated CP issuance.

Banks funding via commercial paper and deposits still trends higher

Source: CMD, ING

Read the original analysis: Eurozone money markets: ECB cuts come to an end but the balance sheet shrinks further

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.