Eurozone lockdown live: The risk of an asymmetric recovery

Judging from mobility data, the lockdown measures in the eurozone seem to have different impacts across the countries. With some countries easing the lockdown measures, while others remain locked down for longer, the risk of an asymmetric recovery has increased.

Eurozone lockdowns are not all alike

While the French need to do paperwork to walk their dog, the Dutch can still do some shopping. The lockdown measures in the eurozone are similar but definitely not the same. Countries did not only react differently in terms of the timing of the lockdown measures, but also in terms of their strictness.

As Italy was the first severely affected country in Europe, it also started the lockdown measures earlier than the rest. Most other countries followed in the second half of March. However, the announced measures differed significantly in terms of the strictness and scope. Some started off with prohibiting public gatherings, others immediately decided on a shutdown. The countries which started off relatively mildly often stepped up the measures quickly afterwards, so that by end-March almost all eurozone countries were in a de facto full lockdown.

To get a sense of how much of public life has been interrupted, we look at Google’s COVID-19 Community Mobility Reports. Google publishes data showing the percent change in visits to certain places like grocery stores, workplaces, and retail shops compared to a baseline (ie. the average of visits for the same day of the week between January 3 and February 6). While categorization may differ between countries, this data does provide an interesting first peek at how significantly public lives have been affected by the softer and harder lockdowns.

Lockdown impact on economic activity

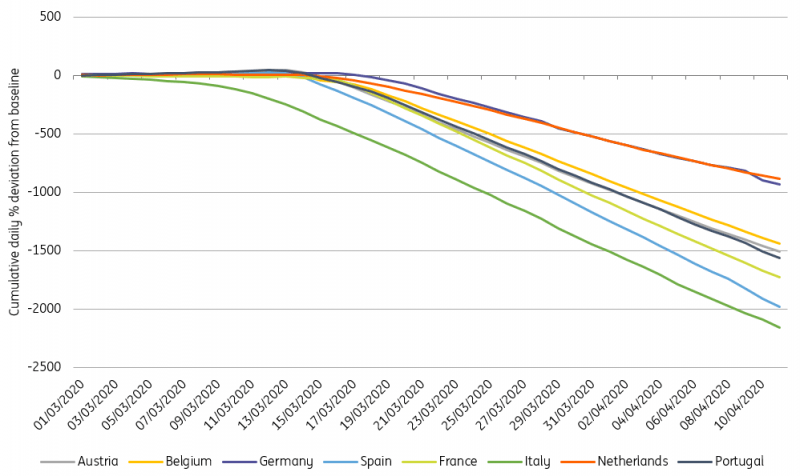

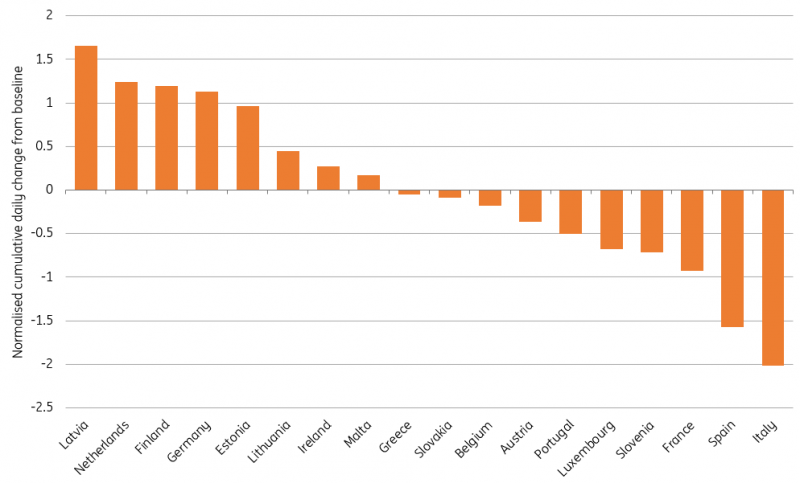

Looking at the cumulative deviation from the baseline for an average of the Google categories ‘grocery stores’, ‘workplace’ and ‘retail shops’ should give an interesting first proxy of how the lockdown measures could affect the different eurozone economies. It does not really come as a surprise that Italy saw a much quicker deviation from the baseline than other countries and has the largest cumulative impact at the moment. Spain has been closing in though and France ranks third in terms of restricted activity. The Netherlands, Finland and Germany are near the bottom of the list in terms of the severity of the lockdown in practice. Greece, Belgium, Austria and Ireland are in the middle of the pack. This suggests that the direct economic impact is likely larger in the Southern eurozone economies and France than in the Northern countries where the lockdown has been lighter.

The cumulative lockdown impact shows which countries have seen daily life most interrupted

Google COVID-19 Community Mobility Reports, ING Research

Note: data from Google COVID-19 Community Mobility Reports, simple average taken of the categories "retail and recreation", "grocery and pharmacy" and "workplace" and cumulated the daily percent deviation from the neutral baseline.

The impact on Southern eurozone economies has been more severe than in most Northern economies

Google COVID-19 Community Mobility Reports, ING Research

Note: data from Google COVID-19 Community Mobility Reports, simple average taken of the categories "retail and recreation", "grocery and pharmacy" and "workplace" and cumulated the daily percent deviation from the neutral baseline.

Which way to the exit?

Now that the new number of Covid-19 cases is dropping across the eurozone, the first plans for exits from the lockdown have been put into place. One overarching theme is clear: there is no sudden return to pre-Covid 19 daily life. A gradual return to normalcy is par for the course as concerns about a quick return of the virus and another spike in hospital admissions leads governments to be very cautious about the endgame.

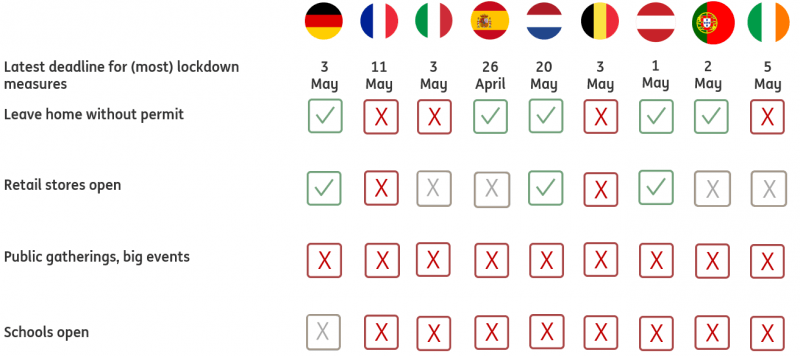

Austria leads the way here as small businesses and DIY and garden centers have been allowed to re-open after Easter. Austria had one of the stricter lockdowns in place from a retail perspective and is now trying to alleviate the impact a little as progress has been made in containing the virus. A gradual opening of hotels and restaurants and also schools are planned for the month of May. Public events are not permitted until July. In Germany, something similar has been announced, with smaller retail businesses open as of April 20 and schools opening gradually. Hotels and restaurants, however, remain closed. Large gatherings have been prohibited until the end of August. Other countries have actually lengthened measures. France, for example, which already has one of the more severe lockdowns in terms of impact on daily life and the economy, has announced an extension of the measures until May 11.

What are the current lockdown restrictions and when will they be lifted or re-evaluated?

ING Research

Lockdown and exit measures likely to increase divergence

Covid-19 is often labelled as a symmetric shock hitting the eurozone economy. While this is correct regarding the nature of the shock, differences in the length and depth of the lockdown measures seem to have a rather asymmetric impact on the eurozone economy. Currently, a pattern seems to be emerging that the eurozone countries which experienced the sharpest impact on public (and economic) life will be the last countries exiting the lockdown measures. Add to this significant differences across countries regarding the size of the fiscal reaction and there is a clear risk of an asymmetric recovery in the eurozone.

Read the original analysis: Eurozone lockdown live: The risk of an asymmetric recovery

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.