Eurozone inflation rises at the fastest pace in December 2016

Consumer prices in the eurozone were seen rising at the fastest annual rate in December 2016. The headline inflation rose for first time in more than three years which is bound to be encouraging for policy makers at the European Central Bank, after a series of stimulus plans launched since mid-2014 targeted towards pushing inflation to the 2% target rate. Inflation in the eurozone has been damped by the weakness of the recovery since a return to economic growth in mid 2013.

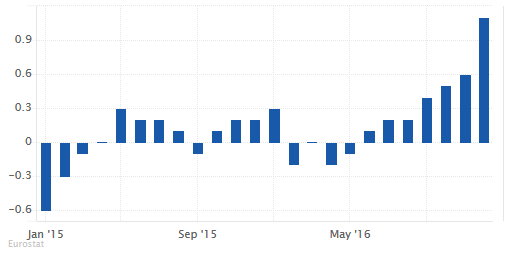

Economic data released by the EU’s statistics agency on Wednesday last week showed that consumer prices in the eurozone rose 1.1% in December compared to a year ago. This was the highest level seen since September 2013 and beat forecasts of 1.0%. Consumer prices accelerated from 0.6% in November.

Driving consumer prices higher was no doubt higher energy prices which rose 2.5% from a year ago and reversing the 1.10% declines registered in November. The recent uptick in oil prices has put many economists to upgrade their inflation forecasts for the eurozone. Many expect that inflation could edge closer to the ECB’s 2% target rate within the first quarter of 2017, a feat that could potentially take a lot of pressure on the ECB which only in December 2016 announced an extension to its QE program beyond the initial date of March 2016, albeit at a slower pace of monthly purchases.

The Eurozone, as with most other advanced economies fell victim to weak consumer prices which fell as recently as May 2016. However, there has been a subtle trend which pointed to a modest recovery in consumer prices which has allayed fears that the eurozone could be at risk of sliding into a deflationary spiral with implications of slowing economic growth and difficulty in repaying the debts.

The recent uptick in oil prices and steadying inflation potentially explains the ECB’s decision on cutting the monthly bond purchases to €60 billion from the previous monthly purchase of €80 billion, due to be effective April 2017. The policy change also came with the central bank noting that the QE would be extended to the end of the year with the potential for further extension if need be.

Despite encouraging signs in headline inflation, the core inflation which excludes the volatile food and energy prices remained little changed. While headline inflation jumped 1.10% in December, core inflation was seen steady at 0.90% in December, slightly higher from November 0.80% previously and remains within the June 2014 levels when the ECB first launched its stimulus program including negative interest rates on deposits and extending the bond purchases to thecorporate sector.

If the core inflation continues to remain steady and shows no signs of increase, policy makers could be increasingly worried that the boost from oil prices to inflation could be short lived.

This view was conveyed by ECB’s executive board member Benoit Coeure who recently said that while there wassign of acceleration in headline inflation, he said that policy makers were still waiting for signs that core inflation will rise and exceed the 1% target.

The economic data from Eurozone last week, however, showed encouraging signs of expansion. IHS Markit’s PMI gauges showed that manufacturing and services sector in the Eurozone rose to 54.4 in December, up from 53.9 a month ago. It marked the highest level since May 2011 and was slightly higher than the initial flash estimates which showed a print of 53.9. IHS Markit’s data was consistent with other economic indicators that showed that the Eurozone’s quarter over quarter growth likely rose 0.4% - 0.5% in the last three months of 2016. This would mark a modest increase from the third quarter’s growth which expanded just 0.3%.

While the economic data might be encouraging for the Eurozone, traders will be looking at the upcoming elections across Germany, France, and the Netherlands which could prove to be a crucial factor and one that could overshadow the economic performance in the near term.

Author

John Benjamin

Orbex

John is a market analyst for Orbex Ltd. and is a forex and equities trader having been involved in trading since late 2009. John makes use of a mix of technical and fundamental analysis and inter-market relationships.