Eurozone flash PMIs see further deterioration in the economic activity

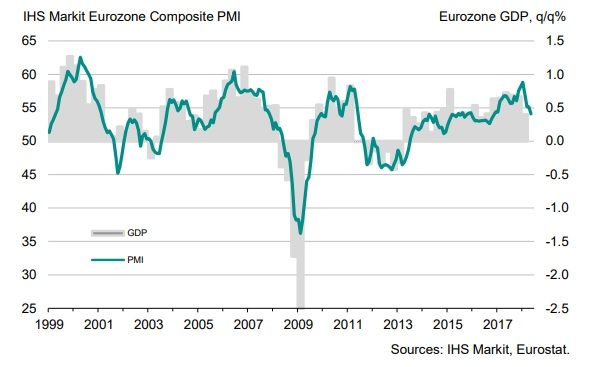

- Flash Eurozone composite PMI fell to an 18-month low of 54.1 in May, down from 55.1 in April.

- The manufacturing PMI in Germany fell to the lowest level in 15 months of 56.8 in May compared with 58.1 in April while services decelerated to a 20-month low of 52.1 in May compared with 53.0 in April.

- With the economic activity slowing down and inflation well below the ECB target, the asset purchasing program is likely to be prolonged until the end of this year.

The economic activity in the Eurozone decelerated further in May with manufacturing PMI falling to the lowest level in last 15 month at 55.5 in May, compared to 56.2 in April and the services PMI falling to a 16-month low of 53.9 in May, down from 54.7 in April. The deceleration in the Eurozone was affected mainly by development in Germany as manufacturing activity in France actually increased in May.

While deceleration at the beginning of this year was affected by adverse weather conditions, earlier Easter, and strikes in some countries, deceleration in May was affected by the unusually high number of public holidays.

“Furthermore, despite the headline PMI dropping to an 18-month low, the survey remains at a level consistent with the eurozone economy growing at a reasonably solid rate of just over 0.4% in the second quarter,” Chris Williamson, Chief Business Economist at IHS/Markit wrote in the PMI report for the Eurozone.

Even with the disappointing reading of May PMI, job creation in the Eurozone remains robust and optimism about the business outlook remains above its long-term average.

Still, the economic activity in the Eurozone remains well off the cyclical high from the turn of this year with the number of external factors including fear of trade wars and rising oil prices weighing on the sentiment for the Eurozone businesses.

Should the deceleration in May be confirmed by the final reading at the beginning of June, the ECB is likely to remain even more hesitant to end its asset purchasing program in September with the most likely scenario of the reduced asset purchasing being prolonged until the end of this year.

The composite PMI for Eurozone

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.