EURO suffers as Eurozone yields rise

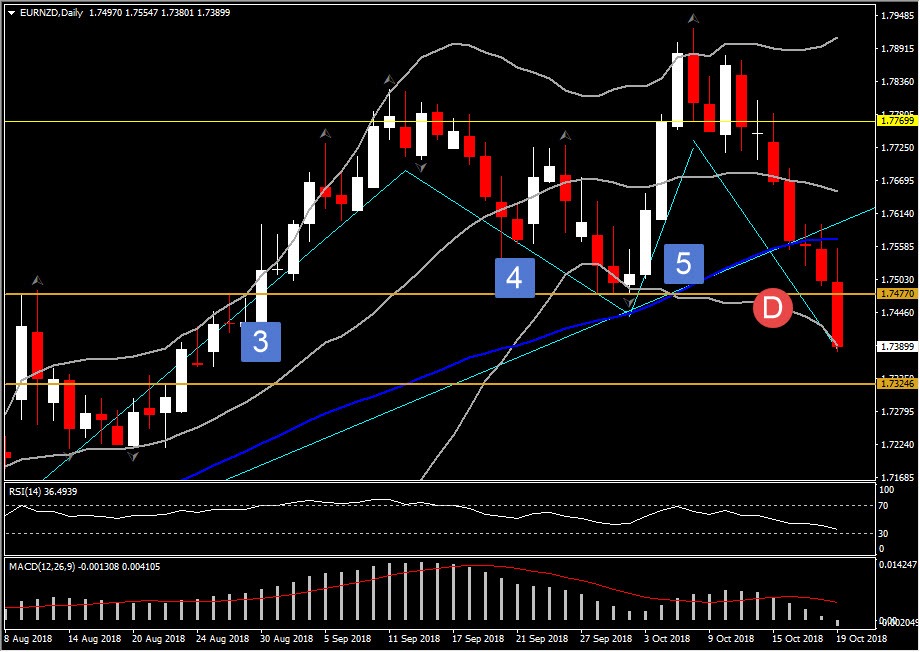

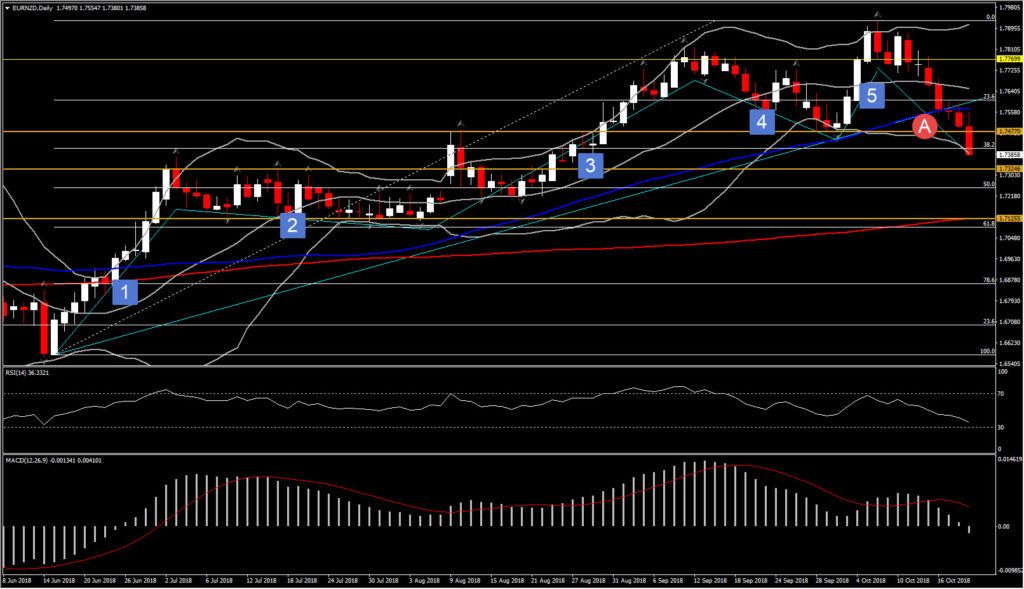

EURNZD, Daily

Italy continues to weigh on Euro, as being one of the main factors of weakness this week. While the Dollar is benefiting from the Fed’s tightening course, the Euro side of the coin is plagued by signs of flagging economic momentum and rising yields in the Eurozone periphery.

More precisely, Spain and Portugal seems to be dragged also into Italian asset slide today, as Portuguese, Spanish and Italian 10-year yields all rising by 7.0 bp or more so far today, which is a reflector of investor anxiety about the Eurozone. Meanwhile, the pressure on Italian assets continue to mount after the European Commission called Italy’s spending plans “excessive” in a letter to Rome, even before the formal assessment of the fiscal plan is being released.

Yesterday, ECB’s Draghi reportedly issued a stern warning at the EU summit and worryingly Spain and Portugal are now being dragged into the sell off. Spain’s banks yesterday got a blow from a court ruling that will mean additional costs and while Spanish and Portuguese yields continue to look low compared to the Italian 10-year, which is trading at 3.75%, the fact that they are up 7.6 bp and 7.0 bp respectively, while Italy’s 10-year gained 7.1 bp this morning will ring alarm bells in Frankfurt.

The German 10-year meanwhile has fallen back to 0.403%. The fact that Italy’s yield spread over Germany gets wider and hit highest level since 2013, exposes Euro further to the downside. Hence the jitters are unlikely to deter the ECB from phasing out QE by the end of the year, but events will make Draghi even more determined to stress that asset purchases are part of the ECB’s regular toolkit and could be revived if necessary.

From the data perspective, today did not provide any significant support to Euro. The Eurozone sa current account surplus widened to EUR 23.9 bln in August from EUR 19.5 bln in the previous month. The improvement was to a large extend due to a wider trade surplus, which will further add to Trump’s criticism of Germany’s export performance in particular. Indeed, the current account surplus widened to a whopping EUR 379 bln – or 3.3% of GDP in the 12 months to August this year, compared to EUR 330 bln – or 3% of GDP in the 12 months to August 2017.

EURUSD peaked at 1.1468 from a 10-day low at 1.1433, coming within 1 pip of the October-9 low, which is a 2-month nadir. However, the overall picture of EURUSD remains bearish as this is the 4th consecutive day the pair has clocked a lower low, and this week is set to be the 3 down week out of the last 4 weeks, with the Euro breaking out of what had been a broadly sideways chop that had been persisting for a month.

The biggest gainer though against Euro so far today is Kiwi, as EURNZD is down by nearly 0.62%. The Euro weakness in combination with Kiwi outperformance, aided by strong Inflation data, helped the pair to move lower, below a key Support level at September’s low, at 1.7477. The facts that the pair moves bearishly for the 7th consecutive day, below the 50-day SMA after crossing on Wednesday below the positive trendline set since June 14, turns the medium-term outlook from neutral to bearish.

From the technical side momentum indicators confirm the strong bearish bias for the pair. The daily RSI is sloping negatively below the 50 zone, while MACD oscillator turned negative with signal line above neutral zone but looking to to the downside. Meanwhile, the pair seems to form an Elliot Wave 5-3 formation, as it satisfied all the guidelines of Elliot Wave Principle. Therefore a close today below the 1.7477 which is September’s low but also it coincides with Wave 4 low, could imply to the continuation of the decline for EURNZD. Next immediate Support holds at July’s resistance, at 1.7325, which also coincides with the mid of 38.2% and 50.0% Fib. level since June’s rally. Further decline could drive the pair at 200-day SMA, at 1.7125.

Hence today’s close price would be crucial for pair’s future performance. Based on Elliot Wave theory, a correction to the upside could be seen at the future, however in order to claim that outlook has turned into a positive one, we must see a movement above the mid of October’s drift.

Current Resistance levels are set at 1.7570 (50-day SMA), 1.7600 and 1.7650 (20-day SMA & 50% retracement as of today).

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in