EUR/USD Weekly Forecast: US Dollar weakness to continue on trade war woes

- China announced retaliatory tariffs of 125%, spurring risk aversion at the end of the week.

- The European Central Bank will announce its decision on monetary policy next Thursday.

- The EUR/USD pair jumped to multi-year highs, more gains are likely in the upcoming days.

The EUR/USD pair jumped to 1.1473 on Friday, its highest since February 2022, amid escalating tensions between the United States (US) and China, triggering a US Dollar (USD) sell-off.

It’s all about the trade war

US President Donald Trump unleashed the wildest trade war in decades. On April 2, the so-called “Liberation Day,” the US President unveiled massive reciprocal tariffs on over 180 countries, hitting its major trading partners the most. A week later, Trump announced a 90-day pause on all the reciprocal tariffs that went into effect on April 9, with the exception of those on China, just leaving a universal 10% rate.

Additionally, “Based on the lack of respect that China has shown to the World’s Markets, I am hereby raising the Tariff charged to China by the United States of America to 125%, effective immediately,” Trump said through Truth Social.

As a response, China announced retaliatory levies will increase from the previous 84% to 125% on Friday, leading to a massive USD sell-off that pushed EUR/USD towards the mentioned multi-month high.

On a positive note, the European Union (EU) also announced a pause on retaliatory tariffs.

Ursula von der Leyen, President of the EU Commission, confirmed they will hold countermeasures of 25% on €21 billion of US goods for three months to give negotiations a chance. “If negotiations are not satisfactory, our countermeasures will kick in,” she added.

The market’s sentiment seesawed around trade war headlines, improving on Wednesday with the pause announcement but souring back right afterwards. Stock markets fell ahead of the weekly close, as market players fear a recession is coming in the US and extending to other major economies due to widespread trade taxes. Fears include higher price pressures, which could eventually lead to interest rate hikes.

Yet the USD also fell as concerns about a US recession overshadowed the Greenback’s safe-haven condition.

The 90-day pause period will likely be all about frenetic negotiations between the US and trading counterparts to find a way to reduce levies and reach more suitable trade agreements. Nevertheless, tensions between Washington and Beijing are meant to escalate and keep investors on their toes.

Meanwhile, widespread levies will also affect inflation levels in the US and beyond, and may force major central banks into rethinking their monetary policies.

European Central Bank in the spotlight

Macroeconomic data has lost relevance in terms of the market’s impact, overshadowed on a daily basis by Trump’s announcements and headlines related to retaliatory measures from major economies.

Still, it's worth mentioning the US release of the March Consumer Price Index, which declined to 2.4% on a yearly basis from 2.8% in February, also beating the market expectation of 2.6%. The core reading, excluding volatile food and energy prices, rose 2.8% in the same period, easing from the 3.1% posted in February, while below the 3% anticipated. On a monthly basis, the CPI declined 0.1%, while the core CPI rose 0.1%.

The Producer Price Index (PPI) in the same period also eased more than anticipated, resulting at 2.7% YoY, while declining 0.4% in the month.

Also, the Federal Open Market Committee (FOMC) released the Minutes of the March Federal Reserve’s (Fed) meeting on Wednesday. The document showed policymakers are utterly cautious, given tariffs-related uncertainty. Officials also noted that economic growth remains solid and the labour market is strong. Regarding inflation, policymakers noted it remains “somewhat elevated”

Regarding future rate cuts, “Participants assessed that the Committee was well-positioned to wait for more clarity on the outlook for inflation and economic activity,” the minutes showed, reaffirming the wait-and-see stance presented by Chair Jerome Powell.

Some officials warned that inflationary pressures could prove more persistent, especially if tariff increases are broader or stickier than expected. Others noted that restrictive immigration policies might ease housing-related inflation by dampening demand.

The EU indicated that Sentix Investor Confidence plunged in April to -19.5 from the -2.9 posted in March. The EU also reported that Retail Sales were up a modest 0.3% in February, missing expectations of 0.5%.

In the upcoming days, the US will publish March Retail Sales, while Fed’s Chair Powell is due to speak about the economic outlook at the Economic Club of Chicago on Wednesday and may provide fresh clues on the Fed’s future monetary policy decisions.

On April 17, the European Central Bank (ECB) will announce its decision on monetary policy. The ECB is widely anticipated to trim interest rates by 25 basis points (bps) each, with the focus turning to the accompanying statement and President Christine Lagarde’s press conference. Speculative interest will try to assess officials’ concerns regarding an inflation resurgence amid the ongoing trade war. Should the ECB suggest a pause in rate cuts, the Euro (EUR) could fall, yet given broad USD weakness, buyers may surge on dips. The opposite scenario is also valid, with the ECB retaining the loosening bias and boosting the shared currency.

Policymakers will likely refrain from giving too explicit guidance within such an uncertain political and fiscal environment.

The week will be a shorter one, given the Easter Holidays. Most markets will be closed on Good Friday, while the US bond market is due to an early close on Thursday, although Wall Street will stick to regular hours.

EUR/USD technical outlook

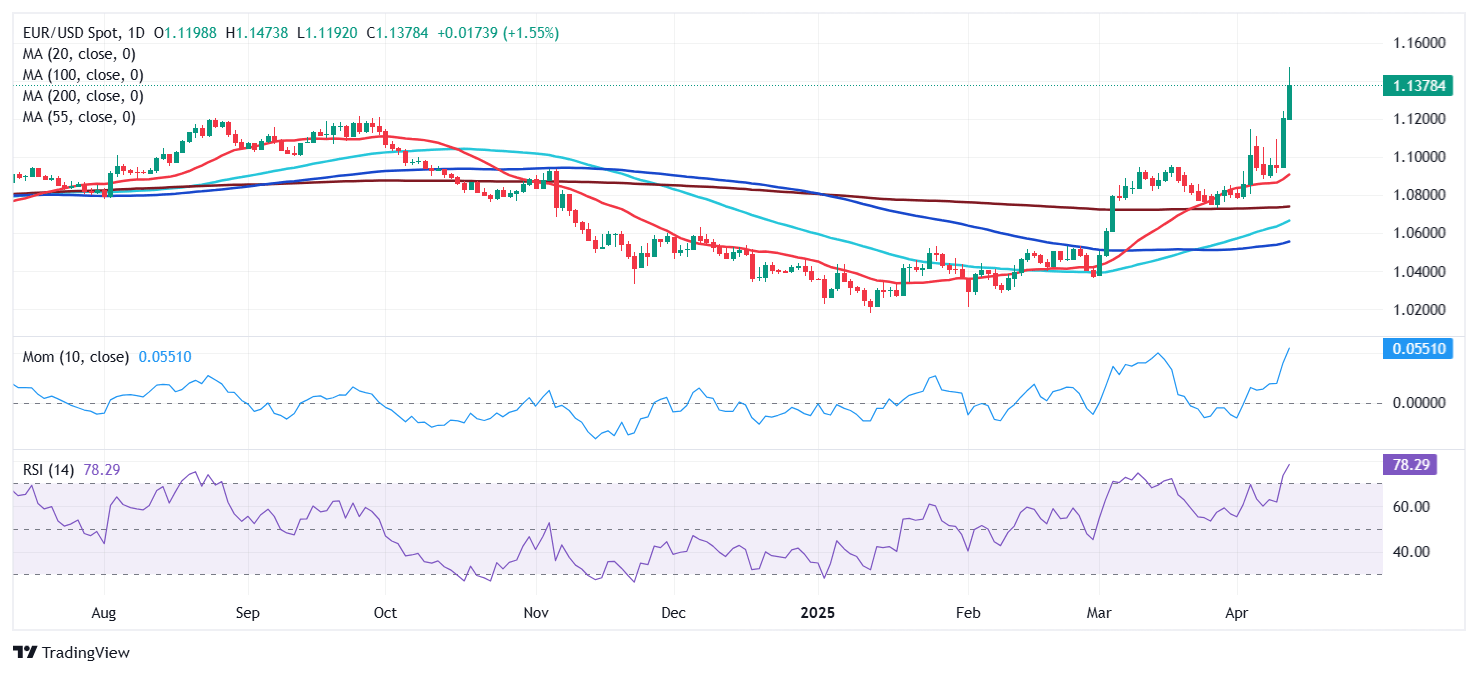

The EUR/USD pair trades around 1.1360 ahead of the close, and the weekly chart shows a solid bullish momentum as technical indicators head north almost vertically. Indicators are currently within overbought levels, yet no signs of upward exhaustion or a potential reversal are underway. At the same time, the pair trades over 400 pips above its 200 Simple Moving Average (SMA), which develops above a flat 100 SMA. The 20 SMA, in the meantime, aims sharply higher, far below the longer ones.

The daily chart indicates extreme overbought conditions, yet few signs of a potential corrective decline. EUR/USD also develops far above all its moving averages, yet with the 20 SMA accelerating north at around 1.0910, while well above directionless 100 and 200 SMAs. The Momentum indicator, in the meantime, advances within extreme readings, while the Relative Strength Index (RSI) indicator is barely losing its upward strength at around 76.

Overall, higher highs are in the docket, particularly if EUR/USD overcomes the 1.1470 area, in which case, the rally may continue towards the 1.1540/60 region. Further advances expose the 1.1600 mark. A slide could find buyers around the former 2025 high in the 1.1240 region, while the next relevant support area stands at 1.1160.

US-China Trade War FAQs

Generally speaking, a trade war is an economic conflict between two or more countries due to extreme protectionism on one end. It implies the creation of trade barriers, such as tariffs, which result in counter-barriers, escalating import costs, and hence the cost of living.

An economic conflict between the United States (US) and China began early in 2018, when President Donald Trump set trade barriers on China, claiming unfair commercial practices and intellectual property theft from the Asian giant. China took retaliatory action, imposing tariffs on multiple US goods, such as automobiles and soybeans. Tensions escalated until the two countries signed the US-China Phase One trade deal in January 2020. The agreement required structural reforms and other changes to China’s economic and trade regime and pretended to restore stability and trust between the two nations. However, the Coronavirus pandemic took the focus out of the conflict. Yet, it is worth mentioning that President Joe Biden, who took office after Trump, kept tariffs in place and even added some additional levies.

The return of Donald Trump to the White House as the 47th US President has sparked a fresh wave of tensions between the two countries. During the 2024 election campaign, Trump pledged to impose 60% tariffs on China once he returned to office, which he did on January 20, 2025. With Trump back, the US-China trade war is meant to resume where it was left, with tit-for-tat policies affecting the global economic landscape amid disruptions in global supply chains, resulting in a reduction in spending, particularly investment, and directly feeding into the Consumer Price Index inflation.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Valeria Bednarik

FXStreet

Valeria Bednarik was born and lives in Buenos Aires, Argentina. Her passion for math and numbers pushed her into studying economics in her younger years.