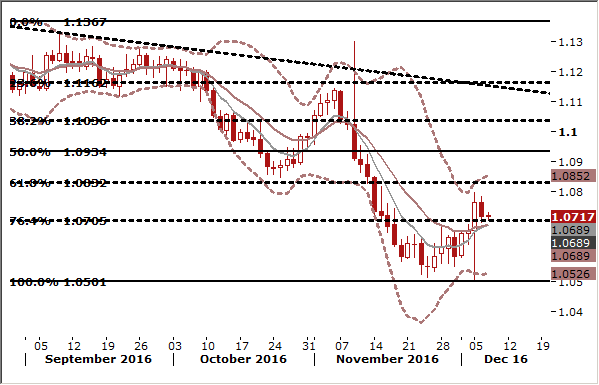

EUR/USD: Tapering cues from ECB may fuel huge EUR gains

-

U.S. Commerce Department said on Tuesday new orders for manufactured goods rose 2.7% after an upwardly revised 0.6% gain in September. That was the largest increase since June 2015 and marked four straight months of gains.

-

The Commerce Department also said orders for non-defense capital goods excluding aircraft, seen as a measure of business confidence and spending plans, rose 0.2 % instead of the 0.4% increase reported last month. Shipments of these so-called core capital goods, which are used to calculate business equipment spending in GDP report, fell 0.1% in October instead of the previously reported 0.2% rise. We do not think that this release will significantly adjust expectations for fourth-quarter GDP growth. The latest GDPNow from the Atlanta Fed puts the contribution to fourth-quarter growth from business fixed investment in equipment at 0.36-percentage point.

-

The report added to factory surveys in suggesting an upturn in manufacturing. However, the progress is likely to be limited by renewed dollar strength in the wake of Donald Trump's victory. The dollar's surge against the currencies of the United States' main trading partners between June 2014 and January 2016 helped to undercut manufacturing activity. With the dollar rally having appeared to fade for much of the year, some of the drag had eased.

-

The USD recovered slightly on Tuesday, but investors are cautious ahead of the European Central Bank meeting on Thursday. The ECB is widely expected to announce an extension to its quantitative easing programme, but there is uncertainty over whether the size of the monthly asset purchases will be kept steady or scaled back, and over whether a formal signal on the eventual end of the asset-purchase programme will be sent. If the ECB does say it will start to scale back its asset purchases the EUR would be likely to rebound strongly against the USD.

-

Technical analysis supports the EUR/USD with bull hammer on December 5 and monthly RSI biased up. We keep our long position unchanged.

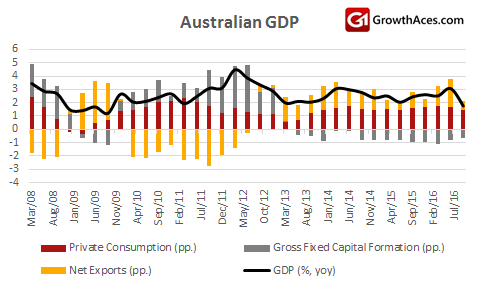

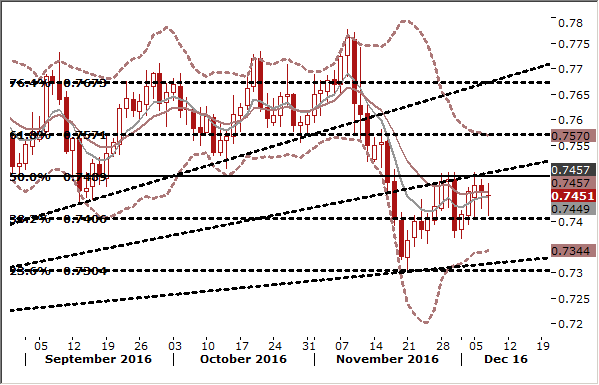

AUD/USD: Weak Australian GDP reading is one-off and good opportunity to buy AUD

-

The Australian economy unexpectedly shrank 0.5% in the third quarter of 2016, compared to an upwardly revised 0.6% growth in the June quarter. It was the first contraction since the March quarter 2011 and the fastest fall since the December quarter 2008, dragged down by investment and net trade. Through the year, the economy grew by 1.8%, slowing sharply from a 3.3% expansion in the June quarter. It was the weakest growth yoy since the first quarter 2013.

-

Gross fixed capital formation dropped by 2.7%, subtracting 0.7 percentage points from growth. Private investment fell 0.8% and public investment decreased 10.4%.

-

Exports of goods and services went up 0.3% while imports of goods and services grew at a faster 1.3%. Net exports detracted 0.2 percentage points from GDP growth. The change in total inventories was an increase of AUD 1,053 million in seasonally adjusted terms compared to a rise of AUD 435 million in the last quarter, contributing 0.1 percentage points to GDP.

-

In the September quarter, final consumption expenditure grew by 0.3%. Household spending rose 0.4% and government expenditure shrank 0.2%.

-

The Reserve Bank of Australia conceded growth would slow when it held rates this week, but also predicted an eventual pick up. The RBA's own index of commodity prices jumped 10% in November alone, and when measured by spot prices was 61% higher on the same month last year. That should boost export earnings and company profits and help cushion the tax take from record-low growth in wages. Consumer demand is also showing signs of life, with retail sales boasting a third month of solid growth in October, while tourism is booming.

-

In the opinion of our economists today’s weak GDP reading is a one-off. We think that factors which dragged down growth were reversed in the current quarter. We believe t that the RBA monetary easing cycle is over and remain constructive on the AUD/USD in the long term.

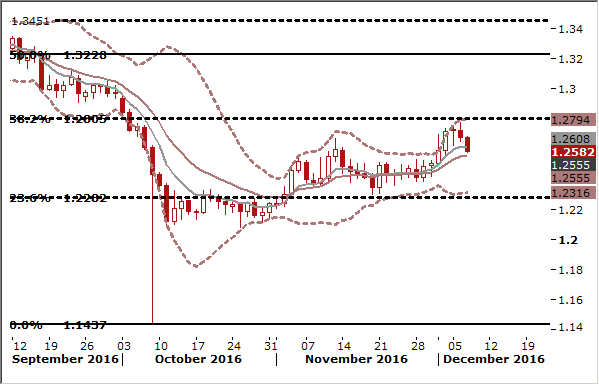

GBP/USD in a corrective phase, but continuation of shallow bull trend is still likely

-

British industrial output fell 1.3% mom in October after a 0.4% decline in September. The monthly decline was the sharpest since September 2012, and contributed to a 1.1% fall on the year, the steepest since August 2013.

-

Oil production was 10.8% down on the month, due to the total shutdown of the major Buzzard oil field. It was the biggest fall since September 2012, when the Buzzard oilfield also suffered production difficulties. Today’s weak industrial output reading is a one-off as oil production is likely to bounce back once the North Sea field completes routine maintenance.

-

Short-term picture shown by British manufacturing sector surveys is mixed. A survey of factory purchasing managers last week showed that activity slowed in November as manufacturers grappled with costlier raw materials after the fall in sterling. The Confederation of British Industry also reported inflation pressures, but said output was expected to pick up at the fastest rate in nearly two years on the back of stronger orders. The CBI said its monthly industrial orders balance improved to -3 in November, its highest level since June, and up sharply from -17 in October.

-

The GBP/USD was hurt by much worse than expected UK October industrial output data. The GBP/USD broke below 7-day exponential moving average and our short-term position hit the stop-loss. We think that recent falls does not necessarily mean the beginning of bearish trend. We will consider another long position when the corrective phase is over.

Author

Growth Aces Research Team

Growth Aces

GrowthAces.com is an independent macroeconomic consultancy. They offer you daily forex analysis with forex signals for traders.