Equities fall – Trump pressing to up their offer for another round of stimulus

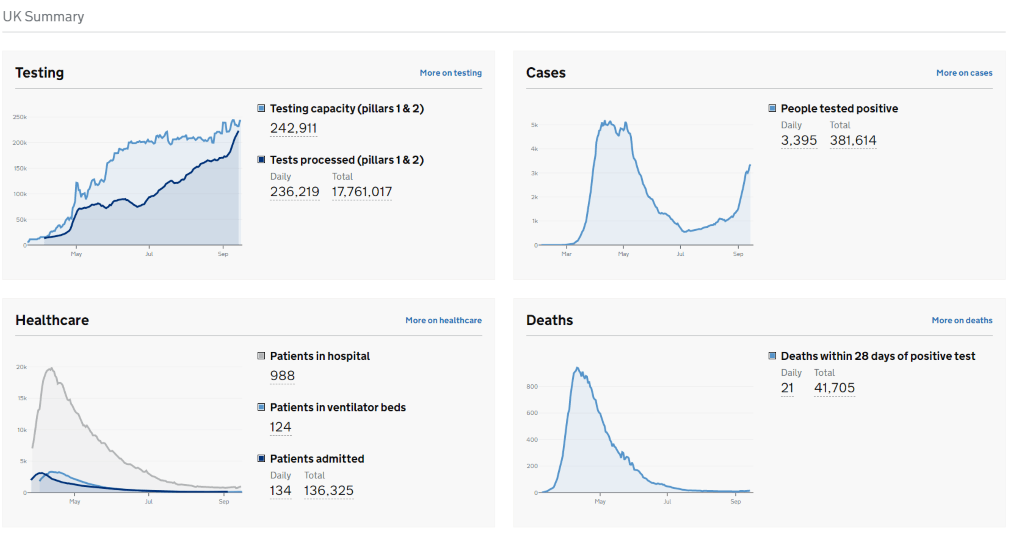

Boris Johnson says a national lockdown would be disastrous, but his scientific advisers are proposing a two-week lock-up in October. A new risk-averse religion with devotees kneeling to the great NHS deity has been born. The question is whether the government decides to ‘follow the science' or not. Cases are certainly up, but the number of tests being carried out daily is exponentially higher than it was in March and April. The worry, of course, is that there is a lag of a couple of weeks and the rise in cases we have seen translates into a spike in hospital admissions in a fortnight.

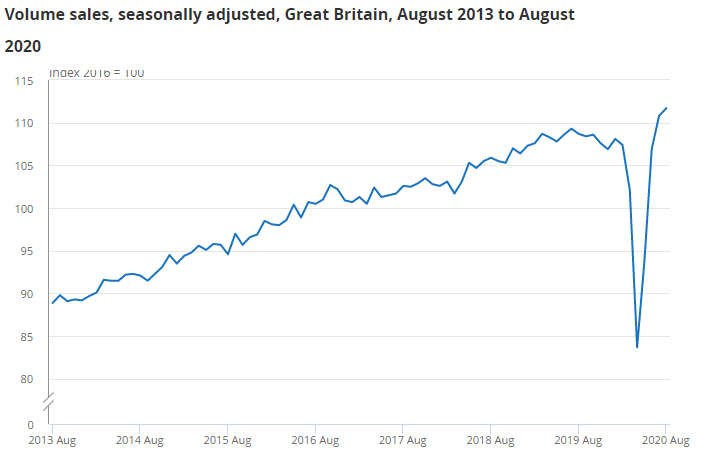

British shoppers are a robust lot. UK retail sales rose 0.8% and are now 4% ahead of February's pre-pandemic levels. When you can't do things like go on holiday you can buy stuff, like DIY materials. Home improvement spending drove sales of household goods to rise by 9.9%. We will see just how this translates into companies when Kingfisher reports half-year results next week. Consumer spending is a big driver of the economy, but unfortunately a V-shaped recovery in retail sales is only part of the picture and we are yet to see what happens as the furlough scheme ends and real permanent unemployment rises.

Equity markets fell, with chatter about a vaccine more conservative and hopes of any delivery in volume really focused on next year and not by the end of October, despite what Donald Trump says. What we might have by the end of October is some really compelling results from clinical trials, which might be enough for markets. Donald Trump is pressing House Republicans to up their offer for another round of stimulus. European stocks were broadly lower on Friday, with the FTSE 100 again looking around the 6,000 level. The S&P 500 down almost one per cent and again testing its 50-day line. The Nasdaq dropped over 1% to close under its 50-day moving average. Snowflake fell, with the stock declining 10% after the frenzied first day of trade led to some profit-taking. Tesla was down 4% ahead, but remains up this week ahead of the Battery Day event next Tuesday.

Jobless claims in the US improved slightly, the picture remains troubled and one of a slower recovery. Initial claims fell marginally to 860,000, but this is still very high. Unemployment remains high at 8.6%, albeit this was a drop from 9.3% the previous week. The total number of people claiming benefits in all programs for the week ending August 29 was 29,768,326, an increase of 98,456 from the previous week.

Yesterday, the Bank of England kept rates on hold at 0.1% and the stock of asset purchases at £745bn, but it looks like on the cusp of delivering further accommodation. The Bank ‘stands ready' to do more, it said, adding that will not tighten monetary policy until there is ‘clear evidence' of achieving its 2% inflation target in a sustainable way. With the current QE ammo due to run out by the end of the year, the Bank looks likely to expand the asset purchase programme by around £100bn in November. There were also overt references to the Bank actively considering negative rates, which hit sterling and sank gilt yields and saw money markets pricing in negative rates this year.

Cable recovered some ground after the BoE-inspired drop as the dollar reversed course, with GBPUSD rising back to its 50-day SMA at 1.30. DXY hit resistance at the 50-day and the longer-term downtrend reasserted itself, although for now the dollar remains in a non-trending sideways pattern. We await to see whether this is the bottom or a pause (bear flag) before the next leg lower.

Oil prices climbed again after the OPEC+ meeting revealed Saudi Arabia's determination to keep the alliance together and conforming with the production cuts. WTI (Oct) rose above $41, the highest in two weeks. There were words of warning for traders from Prince Abdulaziz bin Salman, the Saudi energy minister, who said anyone gambling on the market would be ‘ouching like hell', in reference to a question over whether OPEC+ would taper cuts in December. OPEC+ won't say whether it will take further action to boost prices, but as mentioned yesterday, this will depend on the price, which largely will be a factor of sentiment based around demand.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.