Economic consequences of OPEC supply cut extension

The Organisation of Petroleum Exporting Countries (OPEC) is expected to prolong its 1.5 billion barrels per day (bpd) deal until the end of 2018 from currently agreed March of 2018. The move is widely expected and therefore should be of no surprise for the market players. The economic consequences of oil supply cut extension are directly linked with oil producers but are less likely to dramatically affect the behavior of consumers or the actions of central banks.

What is expected from OPEC meeting?

OPEC and its allies hammered by a prolonged period of low oil prices have decided to cut oil production by 1.8 million bpd back in January this year. With the worldwide average demand of nearly 96 million barrels of oil and liquid fuels per day, the OPEC daily supply cut equals to about 1.9% of global daily oil demand, according to estimates from the International Energy Association.

The strategy of cutting the oil supply worked and since then the oil prices are much higher. Higher oil prices were affected not only by organized oil supply cut but also by the fact that other non-OPEC countries like Russia joined the strategy. Originally the deal within OPEC was to cut the oil supply until March 2018. It is now widely expected that 173rd OPEC meeting in Vienna will prolong the oil supply cut until the end of 2018.

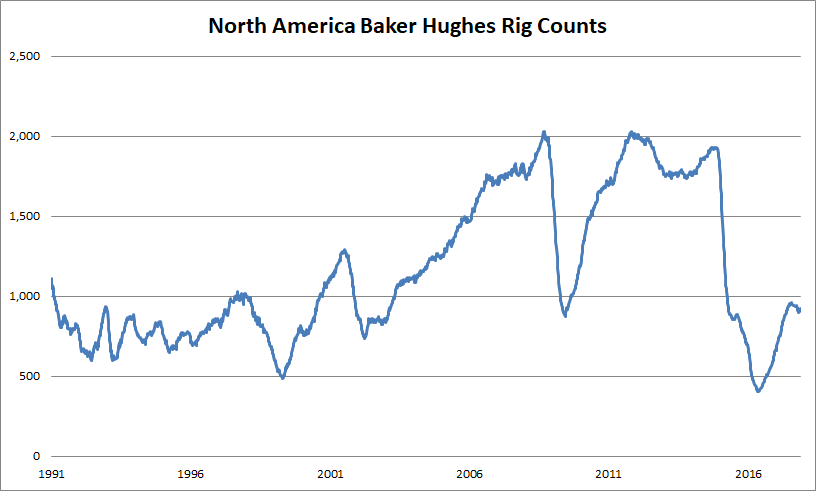

There is a dark side to lifting oil prices using supply cut strategy. Higher prices have encouraged greater output among US producers. According to Baker Hughes rig counts report monitoring the US and Canadian drilling activity on weekly basis, the number of rigs rose to 1138 in North America only in the week ending November 22. The US rig counts rose to 923 as of November 22 this year, representing an annual increase of more than 50% and reflecting current oil price surge.

Higher oil prices and inflation

A combination of the OPEC and non-OPEC supply-side cuts has natural constraints and political issues in countries like Libya while "normal" pipeline problems have also helped lift prices elsewhere.

North sea standard Brent rose some 8% this year alone, but compared to late June oil price lows, it is up almost 45%. Light sweet crude rose 20% this year and is up 40% since the mid-year low.

Both measures are expected to feed through into headline CPI measures in months to come, but the extent of oil price “passing through” to inflation is rather unclear.

According to a research paper from the US Federal Reserve Bank of St. Louis, In 2014, the United States used about 6.95 billion barrels of oil at an average price of $93 per barrel. United States used about $648 billion dollars’ worth of oil in 2014, which was about 3.8% of US GDP.

Researchers at Fed also measured the link between the oil prices and inflation and their conclusions indicate the traditional link between oil prices and inflation is becoming muted in a modern economy.

“Fifty percent reduction in oil prices would cumulatively reduce expected CPI inflation by 27 basis points per year, or about 2.7 percentage points, over a horizon of 10 years” St. Louis Fed research paper claims.

One thing is sure, with higher oil prices, inflation will eventually pick up, but even then still can be disregarded by central bankers as a phenomenon out of reach for a monetary policy.

Author

Mario Blascak, PhD

Independent Analyst

Dr. Mário Blaščák worked in professional finance and banking for 15 years before moving to journalism. While working for Austrian and German banks, he specialized in covering markets and macroeconomics.