Donald Trump is the Dollar-devaluer in Chief

Outlook:

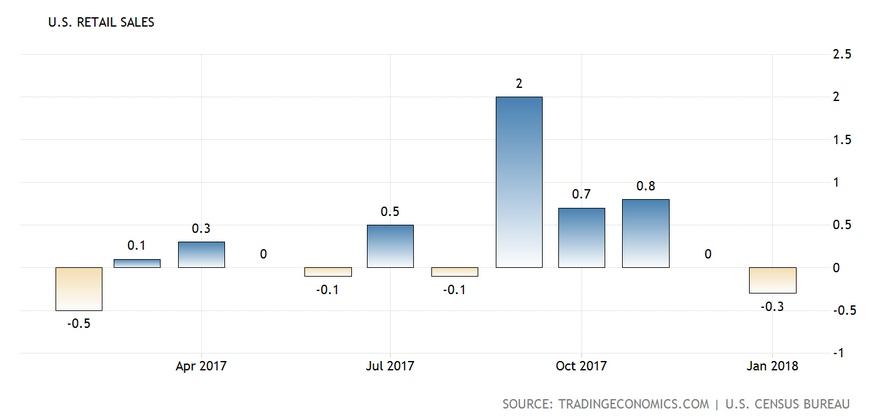

Today the data plate serves up retail sales and PPI. Again we should note that PPI does not feed CPI in the US (as it does in some countries), so will probably be ignored. Retail sales are another matter. Retail sales reflect confidence in the economy as well as households' per-ception of their own financial condition. Now that the tax cuts are delivering tiny gains in paychecks, you might think the ever-materialistic American public went shopping. But probably not. The tradingec-onomics.com forecast is for Q1 to show a gain of only 2.9% y/y, from -0.3% in Jan, which was up 3.6% y/y. Last fall we saw a surge in retail sales, but Dec was flat and Jan was negative.

Political risk jumped up and punched us in the face yesterday, again. It's starting to feel that every time we see sensible reasons to go long the dollar, however briefly, the White House delivers a punch. Trump is not smart enough to be doing it on purpose but making the market leery of buying dollars suits his purposes.

In contrast, with likely self-awareness, Mr. Draghi commented that while the ECB is more confident that inflation will meet the target, risks remain. "But we still need to see further evidence that inflation dynamics are moving in the right direction. So monetary policy will remain patient, persistent and pru-dent." Draghi was speaking is a conference of the ECB with its "watchers." This doesn't withdraw the policy meeting statement omitting threats of higher QE, but reduces the hawkish tone somewhat.

Draghi also said labor market reforms are starting to bear fruit. Unlike Trump, Draghi knows the effect of his comments. Like Coeure the other day, his comments are a mild form of jawboning.

We have political risk coming at us from multiple directions. Was Tillerson's strong support of the UK in calling the poisoning a Russian attack the straw that broke the camel's back? We are still reeling from the firing last week of economic advisor Gary Cohn, not to mention all the other departures that add up to an unprecedented number in the history of the presidency. Then there is the prospect of the meeting with North Korea, something Tillerson's staff say he was looking forward to leading. Therein lies the rub—Trump can't bear any others around him seeking to lead. In fact, Tillerson's trip was an apology circuit for Trump having called African countries "shitholes" a few weeks ago. Trump never apologizes, either.

The US is not the only one. Across the pond, the EU issued a revised draft treaty yesterday and it's a punch in the UK face. According to Bloomberg, "The European Union failed to water down proposals for the Irish border that Theresa May said no prime minister could ever accept in the first revision of the draft Brexit treaty." The EU insists on "keeping" N. Ireland while at the same time inserting an "entire section on ‘good faith.'" This seems to apply to the UK declining to enforce the agreement going forward. The EU made some concessions to the UK, too. New EU laws will consider the effect on the UK, the UK can attend some foreign policy meetings, and the UK will be invited to opt in on some justice and security matters.

But the new draft specifically excludes any concessions for The City. The EU "will protect its financial stability and its regulatory and supervisory autonomy." The EU stance is rude and threatens a show-down at the OK Corral. This, on top of the Russia poisoning story.

So, political risk from N. Korea, Japan (high-level corruption yet to be beaten back), Italy, the EU vs. the UK, the UK at NATO, the US vs. China on trade, and of course Washington, DC. A tidbit is that the Dem in a Pennsylvania election seems to have won with only a few hundred votes despite the Plubs spending more than $10 million for its candidate and even sending Trump, Trump Junior and Dense to rally the troops. This gives the Dems some hopes for the midterm elections coming in November. If the Plubs start feeling desperate, expect more political risk from disruptions.

Where does this leave us? Bewildered. Remember that when in doubt, head for the cross-rates. Euro/pound, maybe. The AUD against anything. This, however, is weak and wimpy advice. We don't see a good reason for the dollar to be slumpy except maybe the wide gulf growing wider between the hard data and the sentiment, plus the orange one-man dollar negative. The hard data points to a decelerating economy and no inflation to speak of, but of course we have yet to see the effects of the tax cuts and the tariffs. We advise sitting it out on the sidelines until this soup clears up.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat