Dollar relatively stable as focus turns to the Fed

Market Overview

The US mid-term elections have given markets broadly what had been expected and the moves on the dollar and Treasury yields in response have broadly reflected this. A Democrat controlled House of Representatives and the Republicans holding the Senate. Aside from a little volatility there has been little to shift the trends of markets moving into the elections. Treasury yields are tracking higher and the trend of dollar correction is still in place, although relatively stable this morning. Democrats taking the House will crimp Trump’s policy ambitions and keep him in check. Yields are higher but perhaps they will be less aggressively higher (with potential for a curve flattening) as perhaps future tax stimulus plans may be restricted. However, equity markets have taken the ball and run with it, in a significant risk on reaction as perhaps some of Trump’s more belligerent policies both at home and abroad may be tamed. Focus now turns to today’s Fed meeting, which is likely to be a relatively tame affair. With recent growth and PMI data still showing the US economy strongly placed, there is little to shift the Fed’s tightening stance. A meeting without a press conference is historically uneventful and aside from perhaps a mild hawkish tweak expect little from the FOMC statement. Overnight we also had the China trade balance which at +$34.0bn was a shade lower than expected (+$35.0bn exp, +$31.7bn last), but data also suggests a rush to trade ahead of the most stringent tariffs, with exports +15.6% (+11.0% exp, +14.5% last) and imports +21.4% (+14.0% exp, +14.3% last).

Wall Street soared over 2% higher with the Dow (+2.1%) and S&P 500 +2.1% at 2813. Futures are just giving some of this back today at -0.2% currently, but Asian markets have been broadly positive (Nikkei +1.8%, Shanghai Composite -0.3%). European futures are pointing to a continuation of yesterday’s rally in early moves today. In forex, there is a degree of consolidation felt across the majors, with a sense that the dollar is just pulling back on some of the marginal losses that were seen yesterday. The New Zealand dollar has consolidated early today after the RBNZ shifted to a more neutral stance on monetary policy at its meeting yesterday. For commodities, gold and silver are continuing to slip a shade lower in early moves today, whilst oil is a touch higher but nothing yet to point towards any sustainable recovery.

Traders will be focusing on the Fed tonight, but this afternoon there will be the Weekly Jobless Claims at 1330GMT to consider first. There is currently no signs of claims starting to increase again, with 214,000 expected (the same as last week). The FOMC monetary policy statement is at 1900GMT and is expected to show the Fed continuing to pause every other meeting and hold the Fed Funds rate range at 2.00% to 2.25%. This is not a meeting with a press conference or updated projections so as tradition shows with this Fed tightening only at press conference meetings, as per usual there is no change expected. The FOMC statement could give a nod to the continued economic expansion that the US economy is showing, whilst but with core PCE at 2% for the past four months there is little need to do too much to change things.

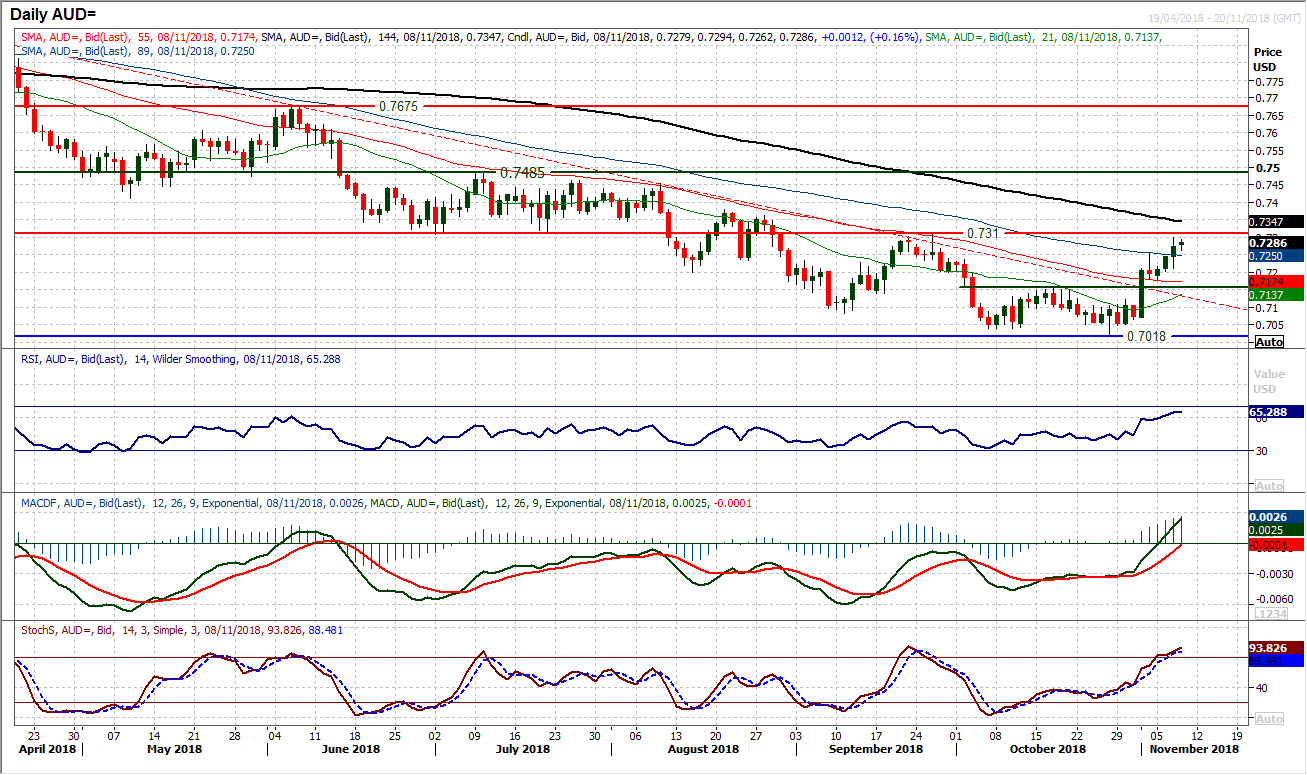

There has been an interesting turnaround in fortune for the Aussie dollar in the past week. The recovery which has broken the long standing nine month downtrend is now testing its next key level. The recovery above $0.7160 completed a small base pattern which implied a test of $0.7300, a target which was hit yesterday. However this now means a far more important level is being threatened with the medium term pivot at $0.7310. This was the old support of June and July which became the key resistance for the September rally. A close above this key resistance would be a decisive shift in the medium term outlook and turn a near term rally into something far more sustainable. The momentum indicators are leading the market higher, with the RSI having failed repeatedly in the 50/55 region throughout the summer, but the RSI has strengthened above 60 with this run. The MACD and Stochastics are also increasingly bullishly configured. The market has been buying into weakness since the strong bull candle last week, with yesterday’s higher low at $0.7210 initial support, whilst the neckline at $0.7160 is also a source of underlying demand. A decisive break above $0.7310 opens $0.7380 and then the key July high of $0.7485.

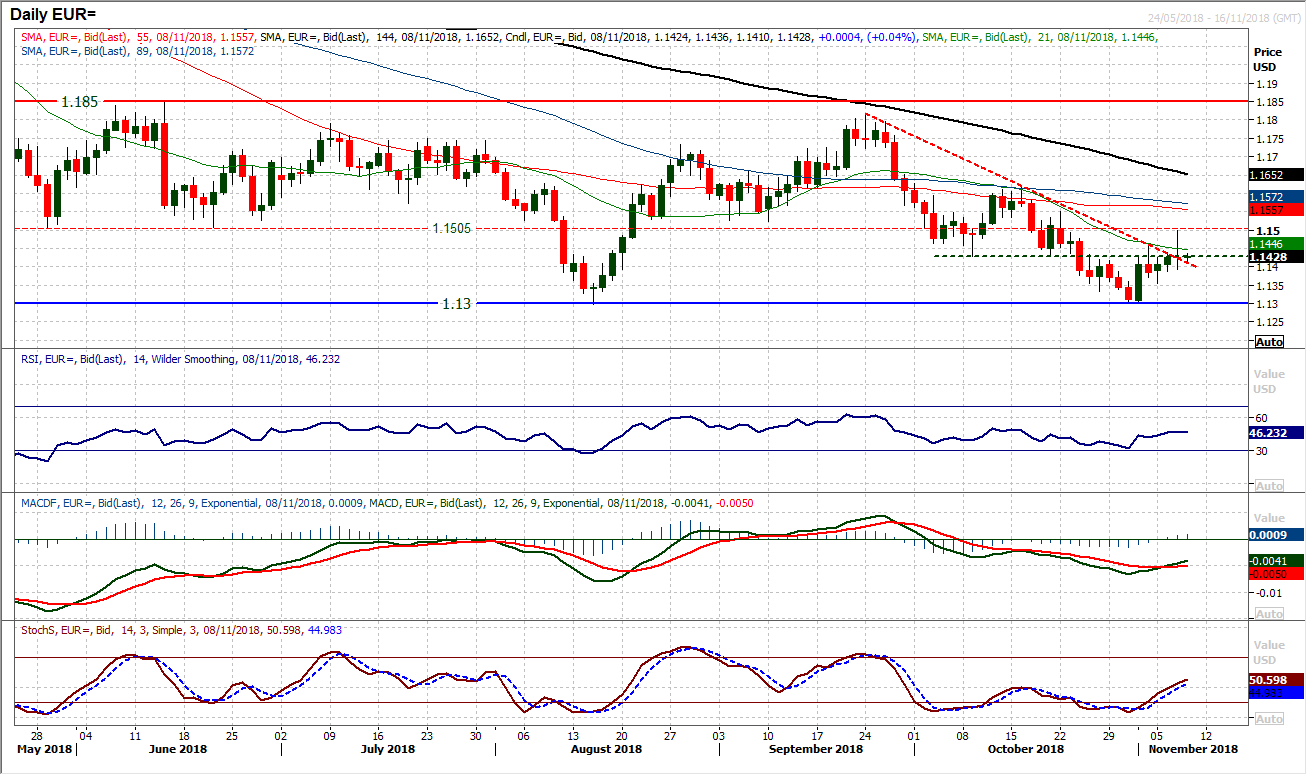

The mid-term results have seemingly done little (so far) to impact on the outlook for the major pairs and the (all but) doji candlestick on EUR/USD reflects this. A doji denotes uncertainty and this is fairly apt for a chart that may have broken through a six week downtrend, but also closed 75 pips off the day high and failed under a medium term pivot at $1.1500. Today’s early consolidation does little to provide us with any further answers either. With this in mind, the euro is trading once more around the near term pivot at $1.1430 again this morning. The hourly chart shows a market in near term neutral configuration too. Whilst the support at $1.1390 remains intact, the bulls will be confident of a continued strategy to buy into weakness but a failure of $1.1355 would change all this now. A close above $1.1500 is needed to suggest the bulls have traction.

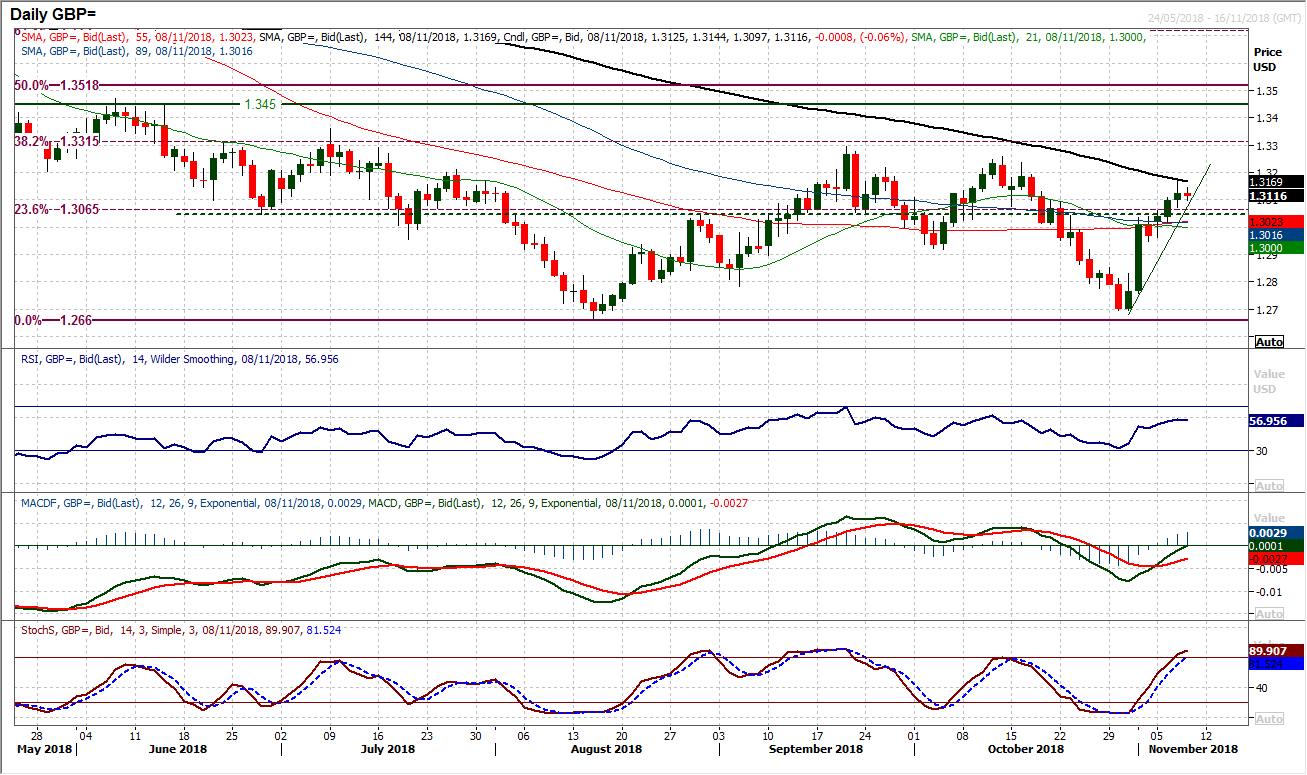

Sterling has rallied well over the past but the magnitude of the bull candles and positive sessions is just beginning to reduce as the impetus from the rally threatens to slow. The market is positively configured within a medium term consolidation range now. The range above $1.2660 has been capped around $1.3300/$1.3400 over recent months and trading above $1.3000 retains a positive bias. There is a mid range pivot as a basis too around $1.3050/$1.3060. Momentum is ticking higher but the market is breaching a mini one week uptrend this morning even though there is a marginal gain in early moves. The initial resistance is $1.3235/$1.3260. The hourly chart needs to be watched as an early warning sign, with the momentum indicators still positively configured but if the hourly RSI starts to drop below 45 and the MACD lines fail below neutral this could be a trigger for a correction. Initial support at $1.3090.

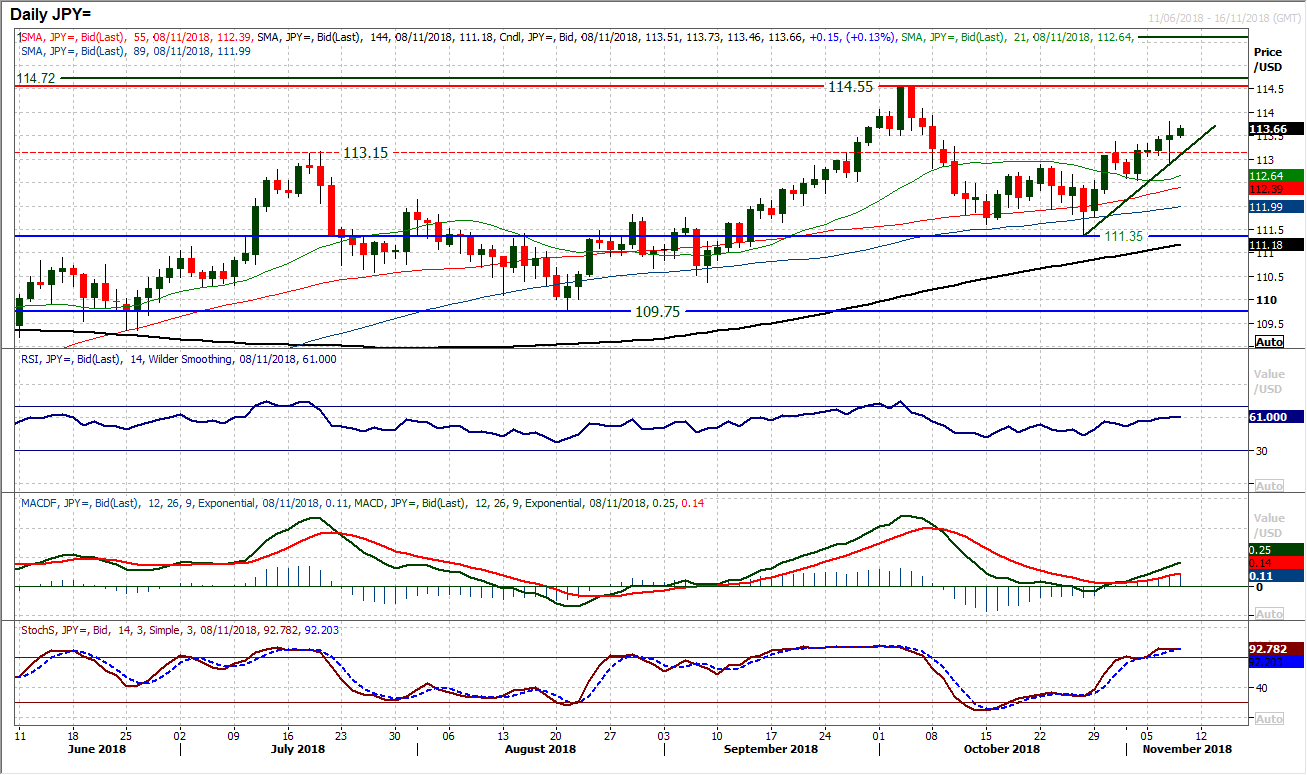

Initial volatility around Dollar/Yen on Wednesday in the wake of the mid-terms has not translated to any meaningful dollar weakness. A choppy session closed higher on the day and this drift higher this morning has continued. The bias continues to be buying Dollar/Yen into weakness. A breach of the resistance from yesterday’s high at 113.80 would be a positive signal, and would certainly open up 114.55 again. Also trading clear of the old 113.15/113.40 resistance band further develops a positive outlook. The support at 112.60 is also taking on added importance as a higher low. Momentum indicators continue to swing higher, with the MACD lines now finding traction.

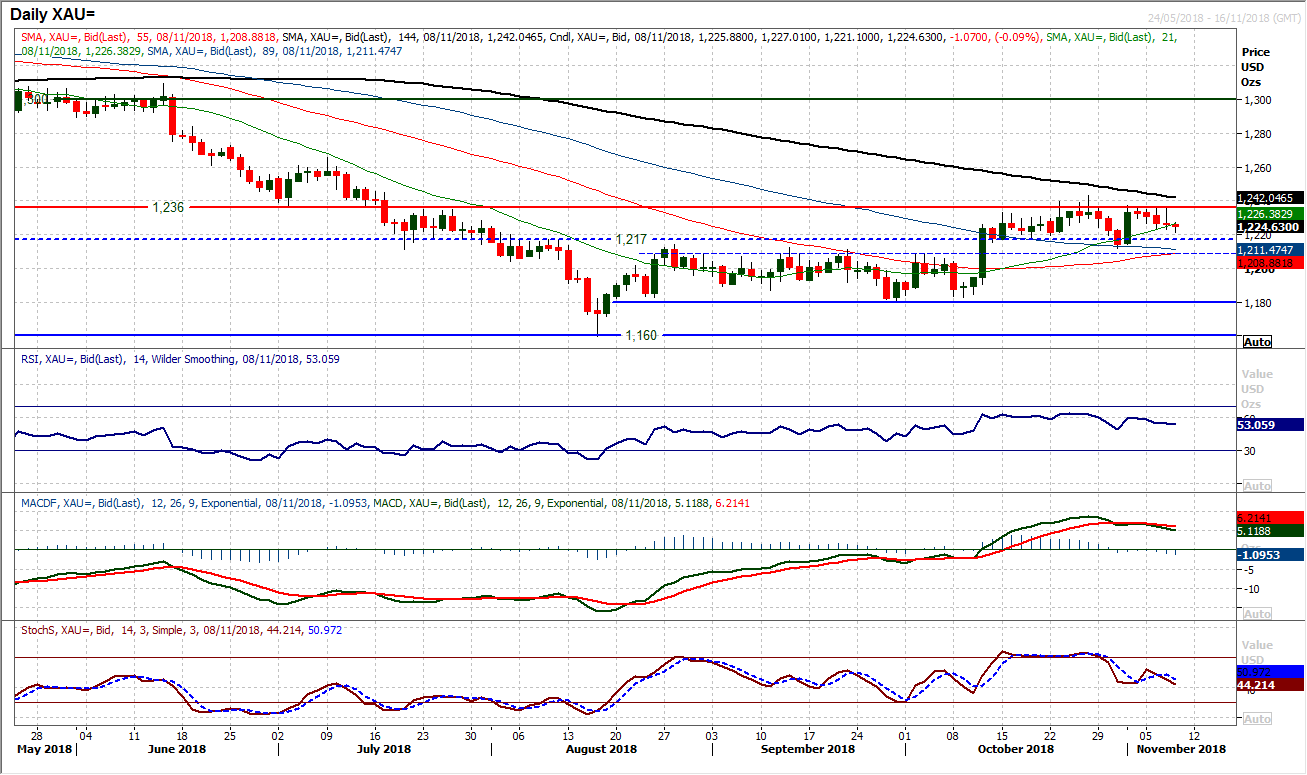

Gold

The dollar negative but risk positive takeaway from the mid-terms results has done little to change the consolidation on gold. What is really interesting though is that for the fourth consecutive session the key medium to longer term pivot at $1236 was the basis of resistance yesterday to cap a range. The market may have slipped away on a closing basis but the pressure on $1236 has continued. However, although there is still a positive medium term configuration which continues to point towards a likely upside break of the range, with the closing losses through this week, the momentum indicators are gradually beginning to slip back, especially the MACD lines. Despite this, any weakness back towards the near to medium term support area $1208/$1217 should be seen as a chance to buy. A close above $1236 opens $1266, whilst a move above $1243 would confirm. A close below $1208 would abort the positive outlook, with a failure below $1200 being negative now.

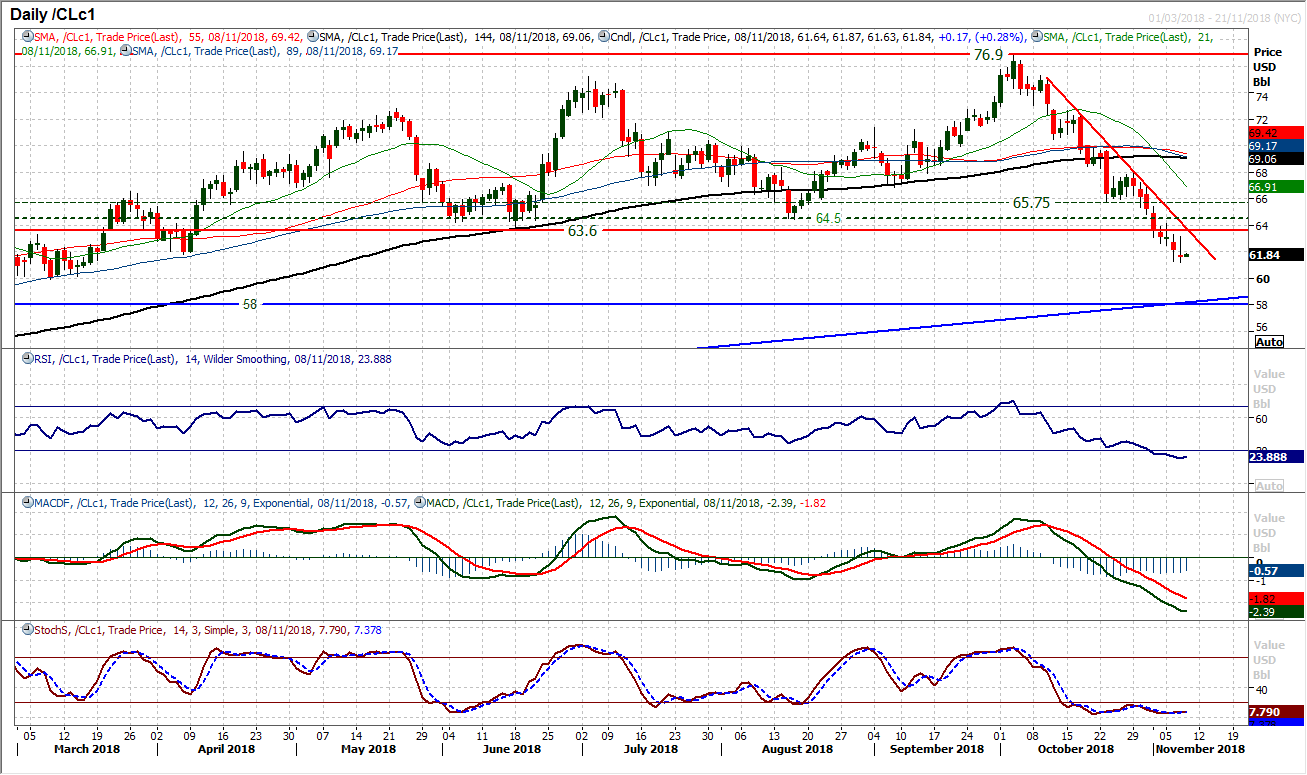

WTI Oil

The EIA inventories continue to show surprisingly large crude builds (for seven weeks in a row now) which suggests downside pressure remains on oi. Having closed consistently below $63.60 throughout this week, the daily ranges are now entirely below this old support which is now a basis of resistance. Furthermore, breaching $61.80 has opened a test of $60.00 now, whilst the next key reaction low under this support and psychological level is at $58.00 The downside pressure within the now four week downtrend continues, with rallies failing at lower levels and the trendline a basis of resistance now at $63.75. Momentum is increasingly negative with the RSI now more stretched than at any time since the multi-year lows of January 2016. Whilst this suggests that near term momentum remains negative, it also suggests that a technical rally is increasingly possible. The overhead supply $63.60/$64.50 will be key resistance for a recovery.

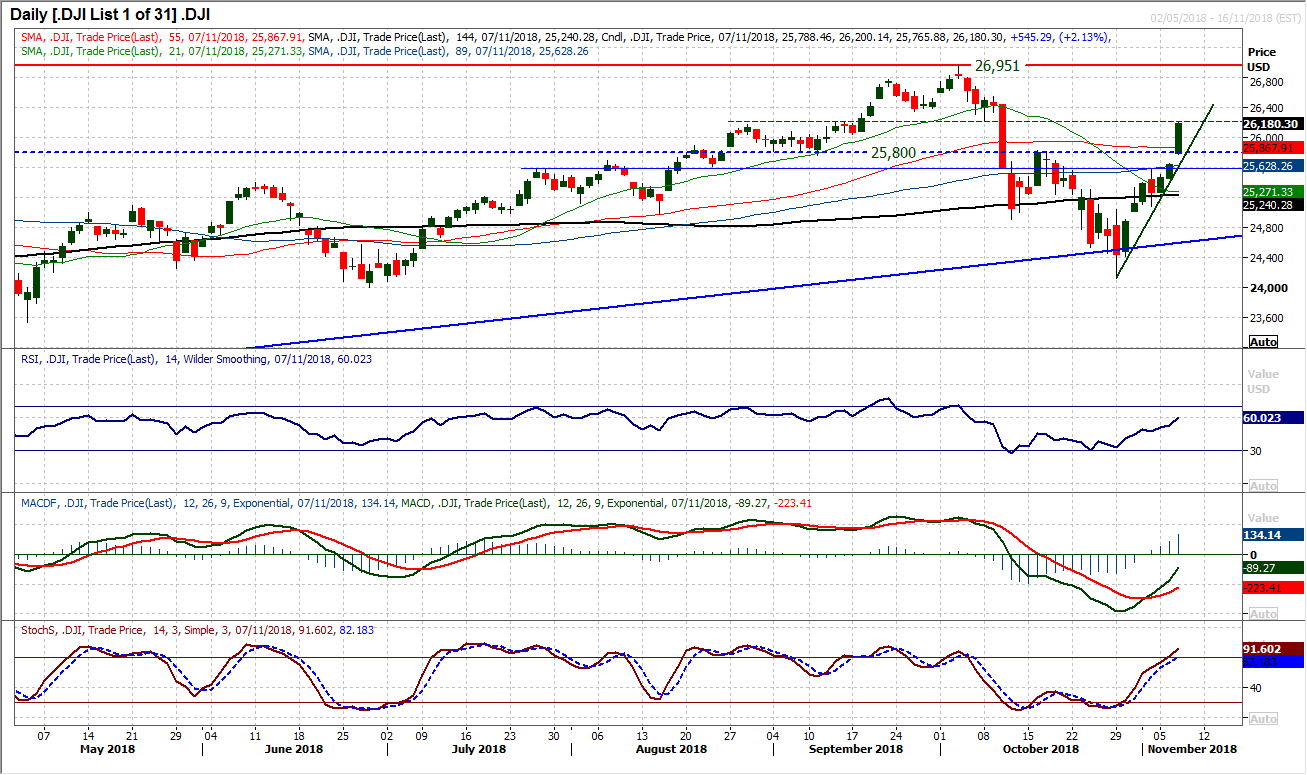

Dow Jones Industrial Average

Wall Street has taken the mid-term results as unambiguously positive, with a gain of over 2% on the day as a response. A huge bull candle with a breakout above resistance at 25,800 coupled with increasingly strong momentum. The 25,800 pivot now becomes supportive once more as the market now looks at the last really important barrier until a return to the highs again. The pivot around 26,220 is in the way of a pull back to the peak at 26,951. Momentum indicators are increasingly positively configured and suggest that corrections are a chance to buy. There is an upside gap open at 25,650 but the pivot at 25,800 is now a prime basis of support should some of the exuberance of yesterday’s session now begin to unwind a touch.

Author

Richard Perry

Independent Analyst