Dollar pressured as traders prepare for crucial FOMC meeting

Market Overview

It is all about the Fed today. The FOMC announces its rates decision and gives guidance on the future path of interest rates (via its dot plots) at 1900GMT. This is then followed by a press conference by Fed chair Jerome Powell at 1930GMT. Expectations of a hike have slipped a shade towards a probability of 70% (according to Fed Funds futures) but it would be a massive shock if the Fed chose not to hike tonight. The arguments for it to be on hold are certainly there (a massive deflationary fall on commodities in recent weeks for one). However the committee has guided solidly for this hike and a step back would be a real surprise, aside from the credibility angle after President Trump’s unconventional urging for the FOMC to hold off. There has been a real shift in markets in recent weeks as fears over the impact of a global economic slowdown have taken hold. The US cannot be immune in this and the cracks are showing. Domestically the wobbles are coming too. Housing indicators have taken a turn for the worse (very much a market linked to higher interest rates), whilst inflation expectations have been significantly pared back. This has pulled Treasury yields lower and equity markets sharply weaker. So the other factor to consider on the FOMC decision tonight will be on forward guidance into 2019. Currently there are three hikes pencilled in on the dots. The market is pricing for less than one. So this wide disconnect has created a situation where the market does not really know what the Fed will do tonight. With the Wall Street Journal suggesting the Fed could hold off all together, but other expectations for still two or three hikes in 2019, the lack of consensus means we can expect a wild ride tonight.

Wall Street closed mixed with mild gains on the Dow but the S&P 500 was almost dead flat at 2546. S&P futures are showing a rebound of +0.5% today, but this has not helped Asian markets which have been weaker (Nikkei -0.6%, Shanghai Composite -1.0%). European markets subsequently look rather mixed in early moves today. Forex markets show the corrective drift on the dollar is into its third day ahead of tonight’s FOMC decision, with the euro showing mild outperformance. In commodities, there is a continued tick higher on gold and silver, whilst oil has rebounded a shade after renewed selling pressure yesterday.

Aside from the FOMC announcement (at 19000GMT) and Powell’s press conference (at 1930GMT) there are also other tier one data points to watch out for on the economic calendar today. UK CPI inflation is at 0930GMT with headline CPI expected to slip to +2.3% (from +2.4%) whilst core CPI is expected to drop back a touch to +1.8% (from +1.9% in October). Also watch out for the PPI Input Prices which are expected to drop to +4.6% (from +10.0% last month). The US current account deficit for Q3 is at 1330GMT and is expected to deteriorate sharply to -$124.3bn (from -$101.5bn in Q2). US Existing Home Sales for November are expected to dip by -0.6% to 5.20m units (from a growth of 1.4% to 5.22m last month). The EIA oil inventories have shown a recent couple of oil drawdowns in the past couple of weeks and are expected to show crude oil stocks dropping by a further -2.5m barrels (-1.2m barrels last week). Distillates are expected to build by +0.8m barrels (-1.5m last week) and gasoline stocks expected to build by +1.5m (+2.1m last week).

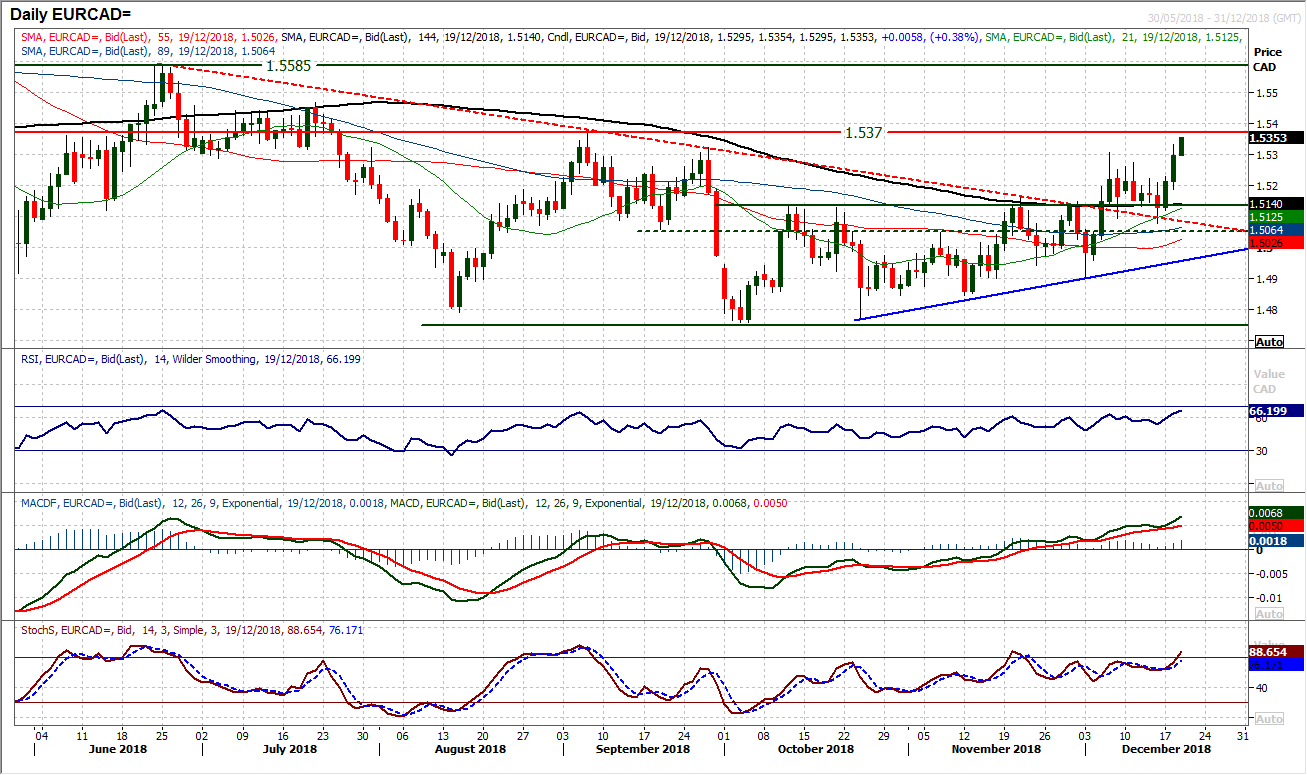

Chart of the Day – EUR/CAD

The improvement in EUR/CAD has comes broadly as the Loonie has continued to weaken (oil price decline related) and this has meant that the medium term technical outlook has really picked up in the past week. The breakout above 1.5135 has since become a basis of support and the near term buy-zone 1.5050/1.5135 is seen as an opportunity now on a near to medium term basis. A couple of bullish candles early this week are now finding upside traction in the recovery. This comes with the price trading above a clutch of moving averages which are all beginning to turn higher in bullish sequence and yesterday’s bull candle was the highest close since late September. This move is reflected in bullishly configured momentum indicators which also have upside potential to suggest that intraday weakness is a chance to buy now. The September high at 1.5370 is now under scrutiny, which would be an extremely important medium to longer term rest for the bulls. Above opens 1.5465 and 1.5580.

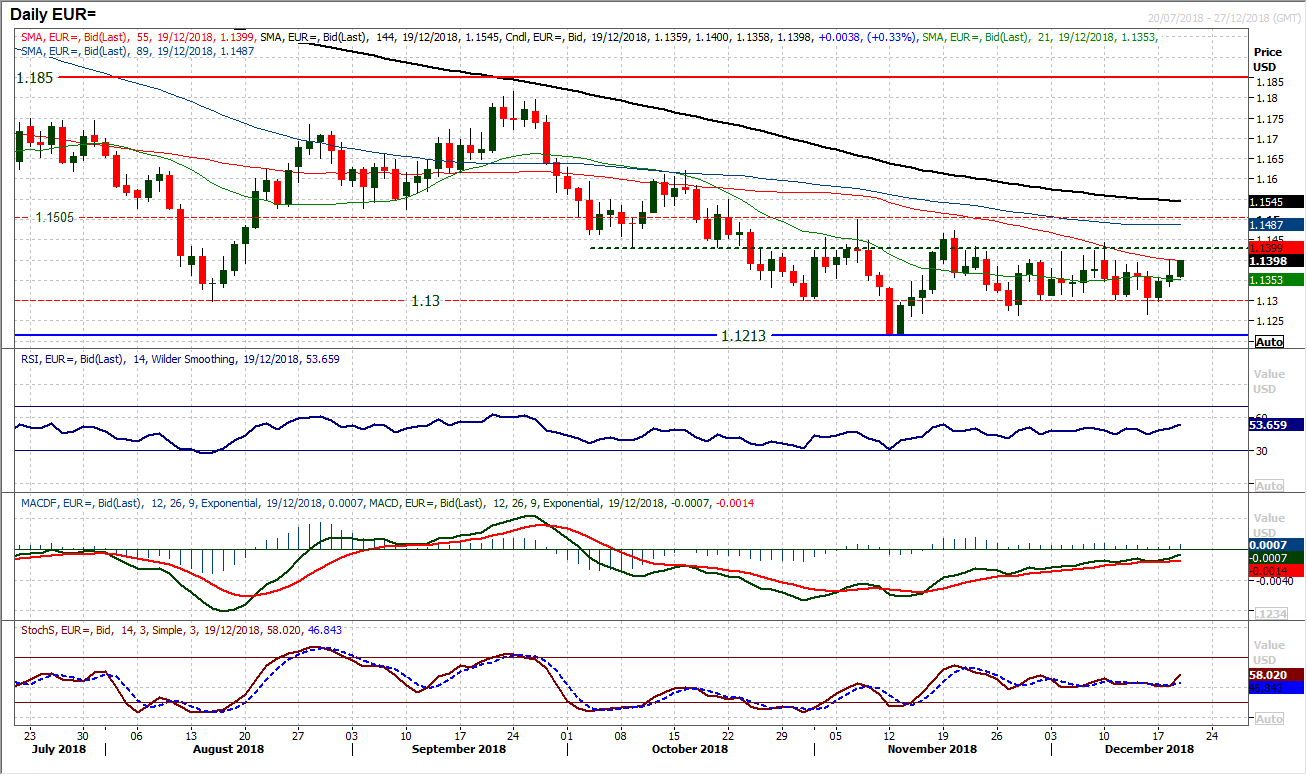

EUR/USD has become increasingly rangebound in recent weeks, but this mood of consolidation is likely to come to an end tonight with the Fed. The support band $1.1265/$1.1300 has been a floor but each time the market even sniffs $1.1400 in recent weeks traders seem to have a collective nosebleed. A close above $1.1445 would be needed to find traction for a potential sustainable rally. There is a mild improvement in momentum coming into the Fed with the RSI ticking above 50. Watch for a close above the mid-50s for a positive medium term breakout. Above $1.1445 opens a test of $1.1500 as the next lower high, with $1.1620 subsequent resistance. A hawkish Fed would be dollar positive and drive a break of support at $1.1265 to open $1.1215.

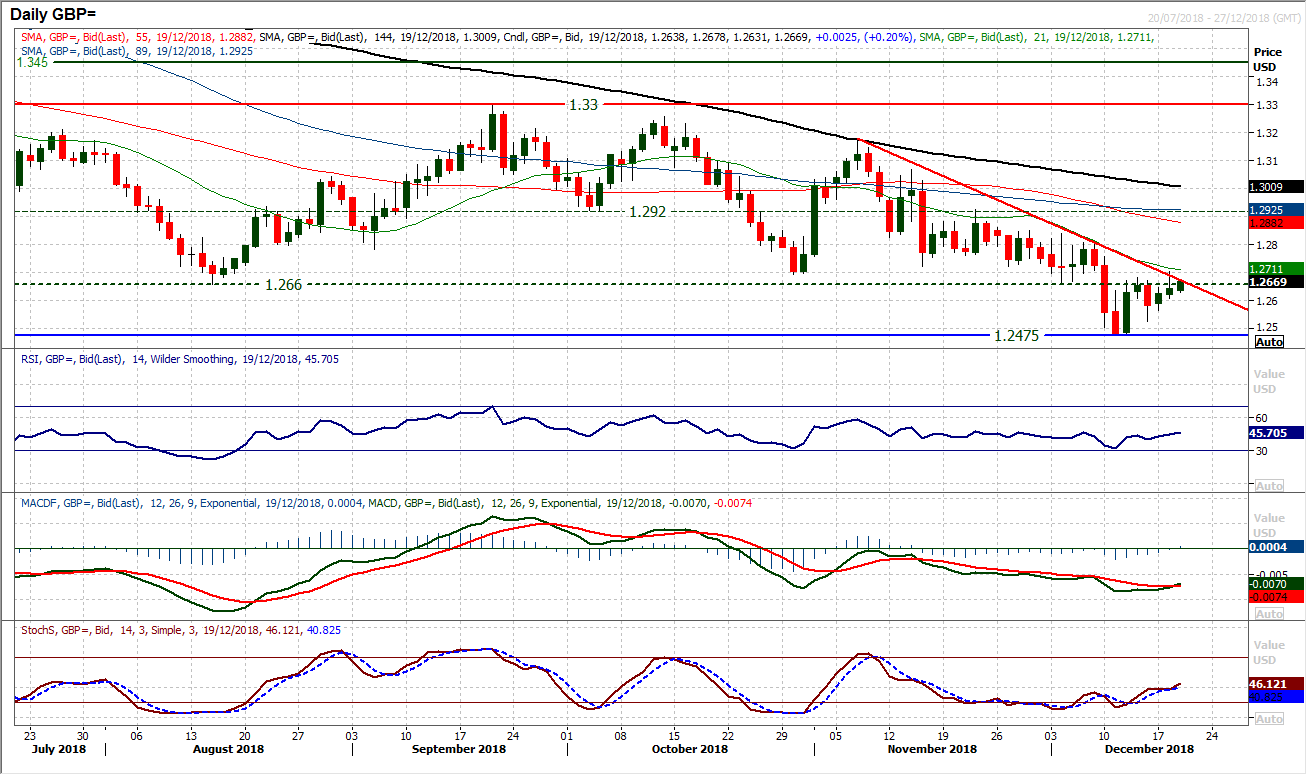

Cable is at a crucial point on the technicals as well as a potential pivot point with the Fed on fundamentals. The key breakdown below $1.2660 has subsequently become a basis of resistance and the market seems to be now testing the confluence of three technical barriers to gains. This pivot at $1.2660, along with the resistance of the now six week downtrend (at $1.2675) and the falling 21 day moving average at $1.2710. A closing break above all these technical barriers would be a positive move. Looking at momentum there is an interesting tick higher too, with the Stochastics leading the way. A bull cross on MACD and RSI above 50 would complete the set. It would open for a test of $1.2800/$1.2850 resistance. Support is initially in for a higher low at $1.2525.

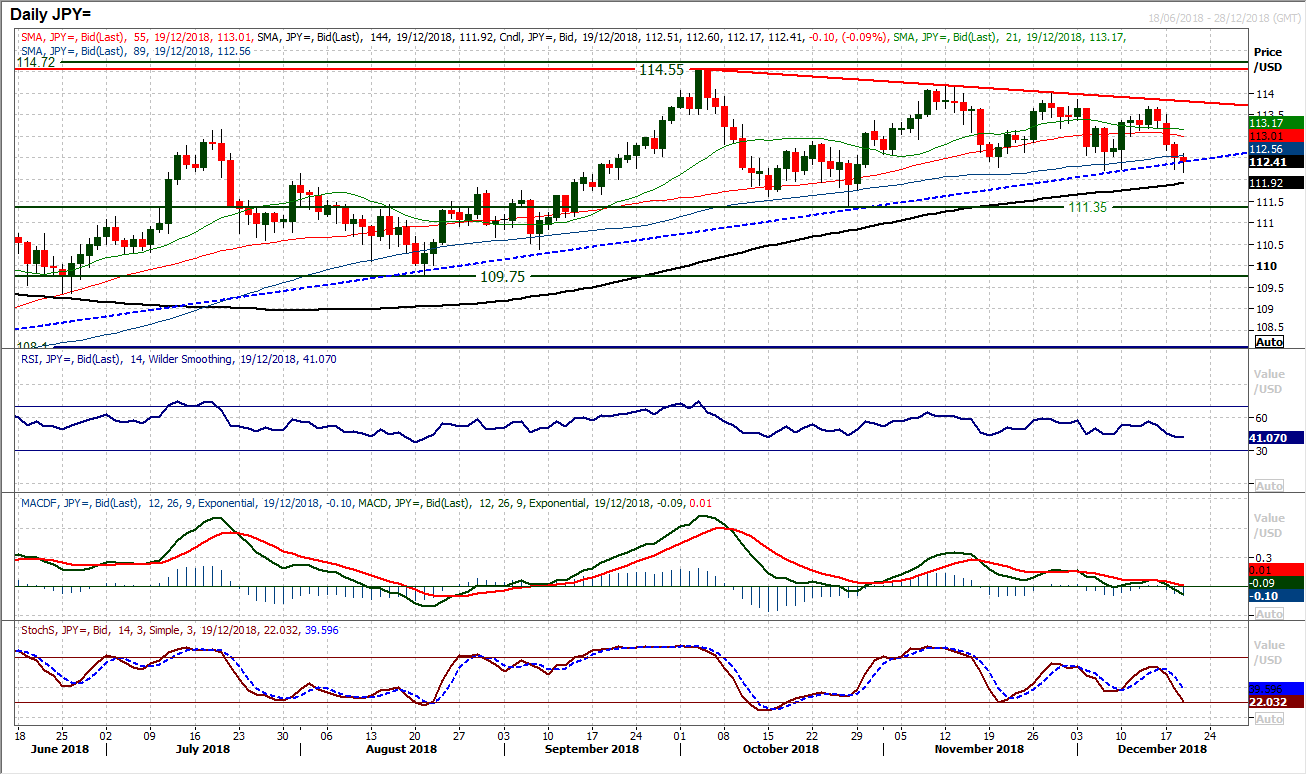

Moving into the Fed, the dollar is under pressure. The six month uptrend has been breached intraday today as has the support at 112.20. Given the importance of tonight’s FOMC decision, the close at the end of the session could be crucial for the medium term outlook. A close under 112.20 opens 111.35 and the momentum indicators are increasingly deteriorating to call for further corrective move. Closing below the six month uptrend would also be negative. The hourly chart shows resistance initially at 112.60 and 113.00.

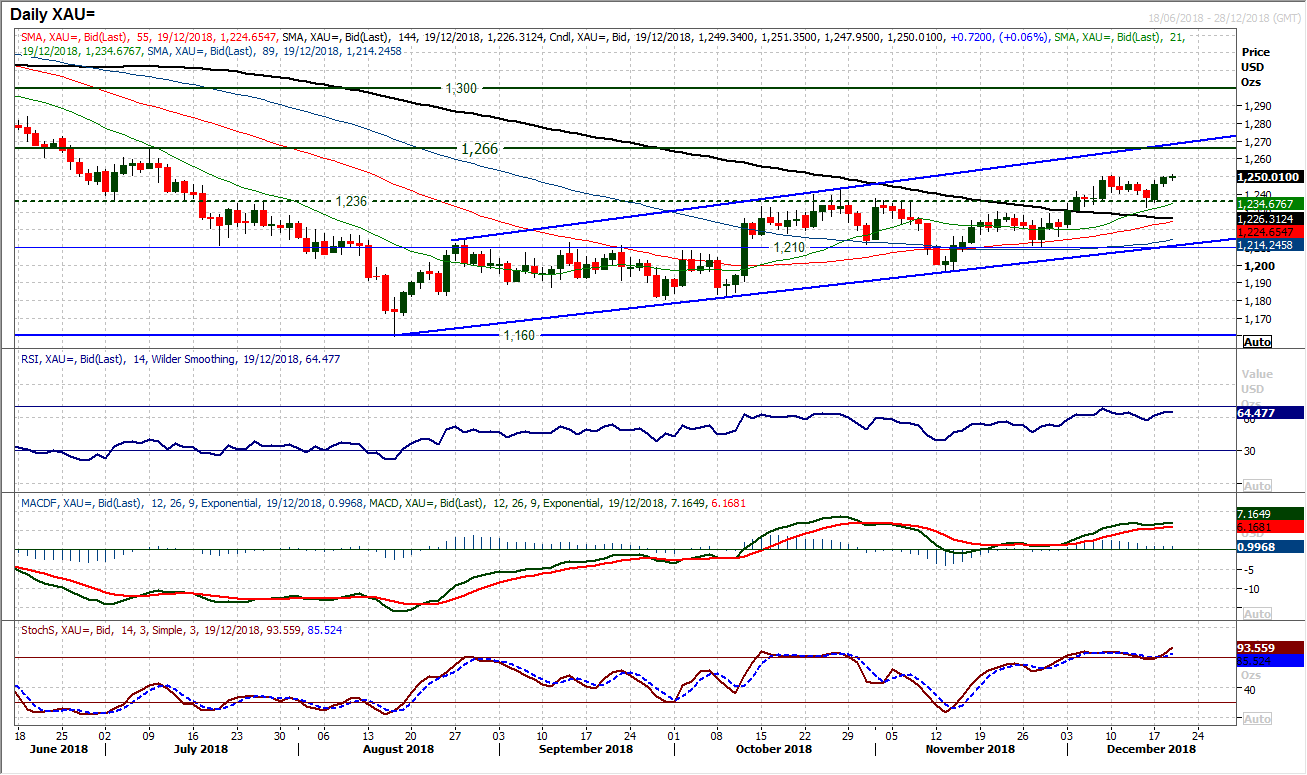

Gold

The renewed positive intent that has taken hold this week has come as the long term pivot at $1236 has become a good basis of support again. However, in order to kick on again, the bulls now need to find traction above $1250 which is a level that restricted the bulls earlier in December. An intraday move above $1250 has threatened already today, but a closing breakout would be needed to open $1266 which is the next resistance from July whilst continuing the bull trend channel (the top of which is currently around $1268). This would also put a key higher low in place at $1232 as support. Momentum indicators are positively configured and suggest that weakness is a chance to buy still on gold and further gains are likely to be seen in due course.

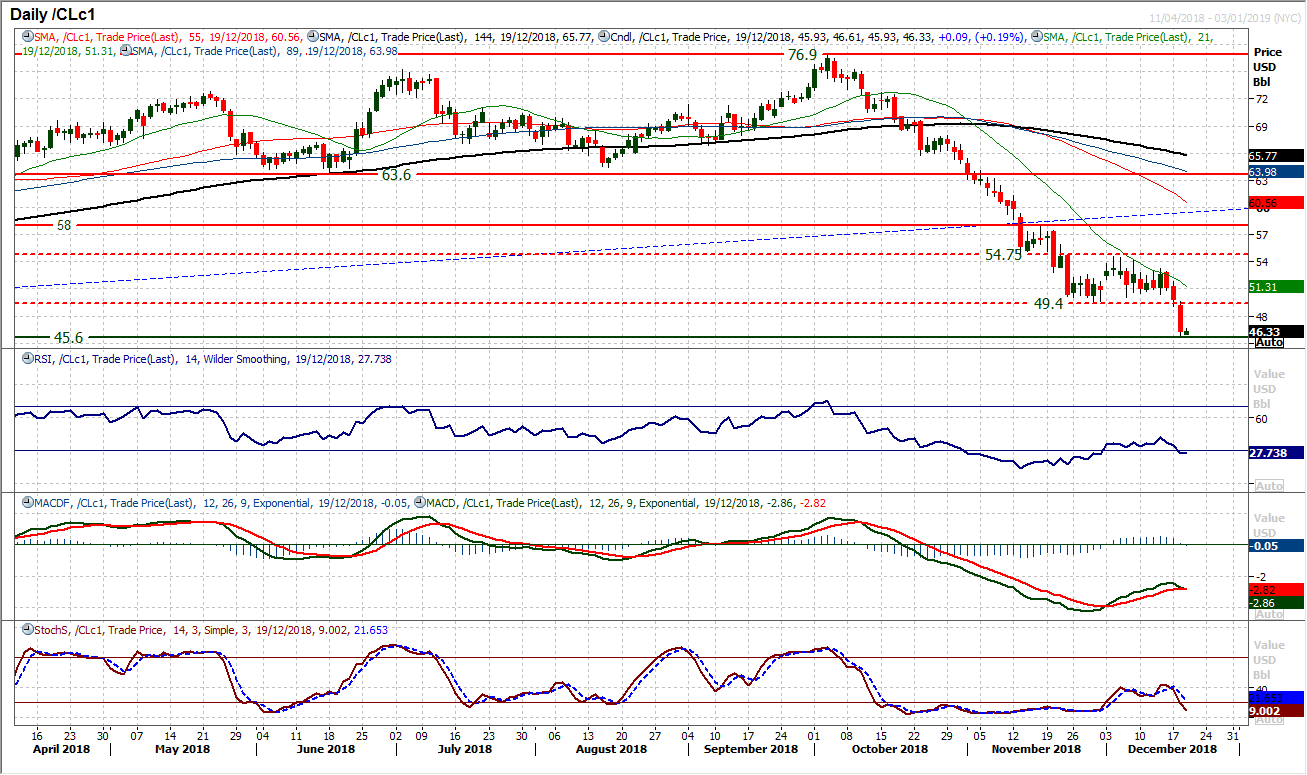

WTI Oil

The decisive break below the November low at $49.40 is a significant concern for the bulls and opens renewed selling pressure now. With three decisive bear candles in a row, the deterioration comes with the confirmation on momentum as the Stochastics cross lower and if the RSI falls back below 30 as well it would be a significantly negative development. The old support at $49.40 is now a basis of resistance as a range breakdown implies a downside target of around $44.50. There is now a near term “sell zone” in the old range support between $49.40/$50.50. Initial resistance is at $47.85.

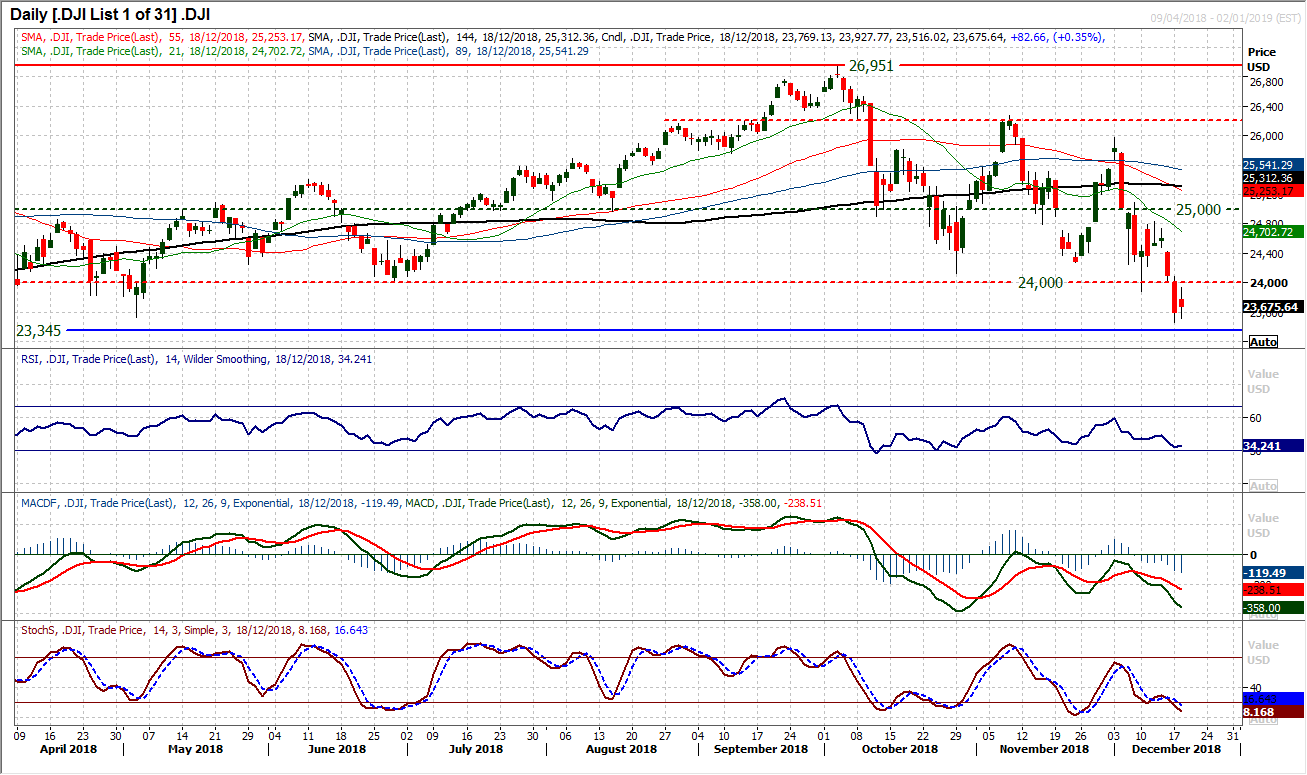

Dow Jones Industrial Average

After the recent selling pressure, yesterday’s session was a holding move. A consolidation effectively, with a mixed candle (closing higher on the day but with a mild negative candle). The support of 23,345 held intact but unless the market can rebound above 24,000 quickly the bears will remain in decisive control. Momentum indicators are negatively configured and show that rallies are a chance to sell. The prospect of the Fed tonight means that there is a potential for significant volatility to continue tonight, but a close above 24,000 would be near term positive for a rally, but under 23,345 would be deeply bearish.

Author

Richard Perry

Independent Analyst