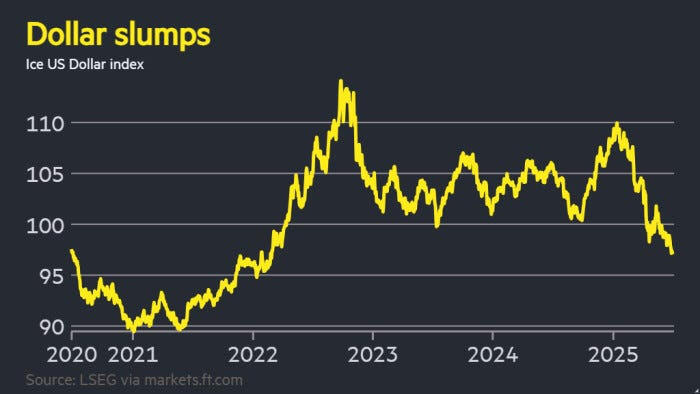

Dollar dethroned? Greenback posts worst H1 since 1973 as markets reprice America

We all saw this one coming—maybe not the velocity, but certainly the direction. The dollar just clocked its worst first-half since the Nixon shock, crumbling more than 10% year-to-date. What began as a slow leak has turned into a full-blown repricing of America’s macro credibility, with the greenback falling off its pedestal faster than you can say “reciprocal tariffs.”

The Dollar Index has now shed nearly 11% in six months, a collapse that echoes the kind of systemic macro reset markets haven’t seen in decades. This isn’t some garden-variety FX wobble—it’s a structural unwind. Trump’s tariff timebombs, fiscal bazookas, and the creeping perception of Fed capture have all coalesced into one ugly truth: the dollar is no longer the safe-haven default, at least not for now.

This wasn’t supposed to happen. The consensus playbook had the dollar strengthening as Trump’s protectionist blitz torched everyone else’s economies. But instead of Europe or Asia cracking first, it’s the U.S. that’s lost the narrative. Growth risks have migrated stateside, and rate-cut expectations have exploded, dragging yields lower and scaring off global capital.

The irony? U.S. equities are ripping—record highs for the S&P and Nasdaq—but in FX-adjusted terms, they’re lagging badly. Foreign investors are getting clipped on currency even as stocks climb the wall of worry. No surprise then that global allocators—from reserve managers to pensions—are dialing down their dollar exposure and dusting off their FX hedging playbooks. The US dollar safe-haven is no longer a free ride.

Treasuries, once the default bunker, are now being met with side-eye. The coming $3.2 trillion in added debt from Trump’s tax plan is too big to ignore. With debt supply surging and demand stalling, even a hint of policy uncertainty sends investors running—not toward dollars, but into Bunds and bullion.

The euro, written off in January as a dead man walking, has surged 13%—above 1.17—proving once again that FX markets don’t care about theory, they trade flows. As U.S. inflation expectations cool and five rate cuts get priced into the forward curve, the greenback has lost its yield advantage. And without that, what’s left?

Even gold—stoic and quiet—is quietly flashing warning signs. Central banks are still stacking metal like it’s 2008 all over again, not because they think the system will implode, but because they no longer trust the dollar as a one-way hedge.

Some call it “crowded,” and maybe it is. The dollar short trade is thick with positioning. But crowded doesn’t mean wrong—it just means the exit is narrow if the tape turns. For now, this looks less like a dip and more like a regime shift. The dollar isn’t dead, but the narrative that it’s unshakeable has cracked wide open.

The message from the market is simple: if America’s going to throw around fiscal firepower and weaponize trade policy at will, don’t expect the world to keep financing it with both hands. We’ve crossed from faith-based FX to flow-based reality—and the greenback is no longer wearing the crown.

Month-end muscle memory meets macro intervention – Eyes on Taipei

The much-studied, much-traded month-end effect still works—on average, not every month, of course. It's worked since I was slinging spot like a madman back in 2005 when this was already a well-worn trade, and yet here we are, two decades later, still talking about it in FX circles. Efficient market theorists can keep clutching their Fama textbooks—flow still rules the tape.

The setup this month is textbook. With U.S. equities ripping +5–6% in June, foreign holders are staring at bloated mark-to-markets. If you’re long a billion SPX and short a billion USD as your hedge, and that equity’s now worth $1.06 billion, guess what? You’re $60M USD overhedged—and month-end means you need to sell dollars to get back in line. That’s your classic rebalancing trigger. The usual foreign fund suspects hedge monthly, not dynamically. Hence, the flows are chunky and often ill-timed, which can result in a significant amount of dollars hitting the tape into and after the Fix.

EUR/USD buying (USD selling) into and out of the London 16:00 WMR Fix was a one-way street

-638869204321876005.jpg)

Typically, London flows initiates the process at the "WM/Reuters" fix, and New York usually fades the bounce ( in either direction) into the end of the day. That’s why I’m up before the soi dogs bark in Bangkok on month-end mornings. But this time? Crickets, no EURUSD fade to speak of. June's playing it cagey—maybe waiting for ISM and payrolls, maybe waiting to see who blinks first.

Month-end muscle memory meets macro intervention – Eyes on Taipei

That brings us to Taiwan, where things are getting loud. The TWD has been the stealth sniper of Asian FX—up over 10% YTD and triggering alarms in Taipei. But now we’re seeing real cracks: a late-session 2% dump, the biggest single-day drop since 2001.

-638869204767780499.jpg)

That kind of move doesn’t just happen—state banks were spotted lifting USD as if it were an intervention drill. Whether you call it the invisible hand or just policy pragmatism, it’s clear the central bank doesn’t want a runaway currency killing exports or blowing holes in insurer balance sheets stuffed with USD-denominated assets.

This may be the first clear canary in the regional FX coal mine. Central banks aren’t going to sit back while the dollar falls off a cliff and their local exporters get smoked.

So don’t get lulled by the quiet. Asia may be the big dollar seller in June , but the real story could be who steps in to cap the upside in local FX.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.