Debt ceiling deal and market breadth: What's next for forex?

Debt ceiling tentative agreement optimism continued into Memorial Day, and S&P 500 opened the Globex session with a bullish gap, which the sellers (unsuccessfully) attempted to close, and the true battle of today is going to be waged in the 4,235 – 4,245 area.

In short, if there is going to be any sell the announcement news, it has to happen early in the regular session, otherwise the very narrow breadth and extremely selective ES upswing feeding off AI, Big Tech, communications and consumer discretionaries, is to continue.

Quoting from Sunday‘s extensive analysis:

(…) If anything, the market has become ever more concentrated, with NVDA earnings guidance reflection taking valuations to ridiculous 188. That‘s the AI side of the market, on fire and leading. The only other sectors doing well apart from tech with semis segment, are communications and consumer discretionaries – effect strong enough to overpower badly lagging industrials, materials, financials (chiefly banking), retail, smallcaps and defensives (utilities and staples), which brought about yet another daily bullish call before the opening bell Friday..

Debt ceiling deal hype is another factor going in for the bulls as any sell the news reaction seems to me postponed by a couple of days at least if Yellen moved the new make or break date to Jun 05 (there is still almost $40bn in TGA). Friday saw much of the hope for a deal to be reached soon, priced in – and the tentative one announced this weekend, will likely invite a some sell the news reaction before the AI mania continues. The midnight May 31 vote on it is a downswing risk, but I‘m not looking for a stunner, and instead expect the deal to pass.

So, the only variable the market chose to override Friday, was somewhat hotter core PCE, which didn‘t result in more than a 30min dip. Jun 25bp hike is now the base case scenario, and the short end of the curve isn‘t budging in its bets on Fed pause then, and rate cuts going into 2024. Tech still doesn‘t mind the ever widening disconnect to rates, and apart from AI FOMO, a smaller portion of the explanation is that rates on the long end are approaching their peak, and with the onset of recession (most likely Jul-Aug-Sep), these would retreat to arround midpoint of their yearly range (3.50% for 10-y).

Unless a debt ceiling deal fails, the Fed wouldn‘t back off inflation fight and balance sheet shrinking, and with the Treasury back to issuing fresh debt when commercial bank lending to the private sector isn‘t exactly expanding (crowding out effect), new buyers incl. from abroad would have to step up to the plate – and any flight to safety would have of course negative implications for the stock market standing on increasingly fever legs at a time when LEIs keep still sharply decelerating (inevitable recession)...

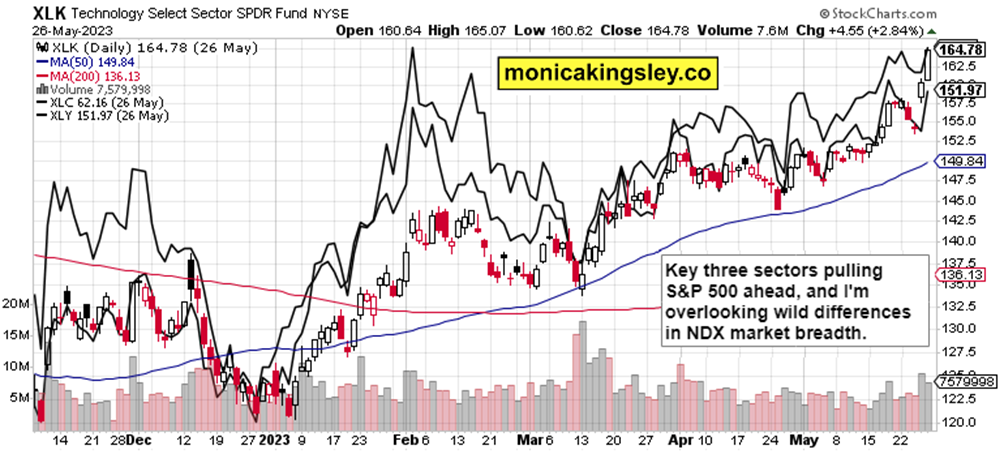

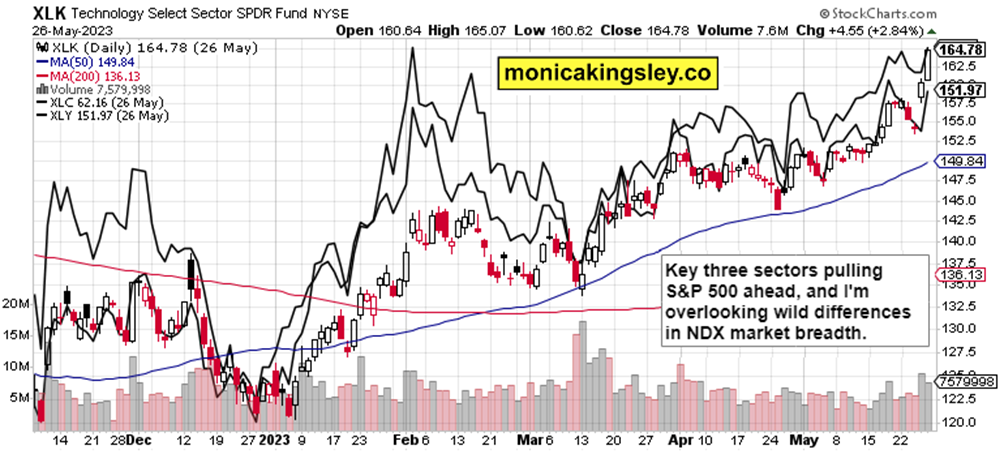

Let‘s contrast the leaders and laggards sectorally in the below two charts as an illustrative companion to the market breadth issues presented Sunday.

Keep enjoying the lively Twitter feed via keeping my tab open at all times (notifications on aren't enough) – combine with Telegram that always delivers my extra intraday calls (head off to Twitter to talk to me there), but getting the key daily analytics right into your mailbox is the bedrock.

So, make sure you‘re signed up for the free newsletter and make use of both Twitter and Telegram - benefit and find out why I'm the most blocked market analyst and trader on Twitter.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.