DAX takes rally continues on optimism over China

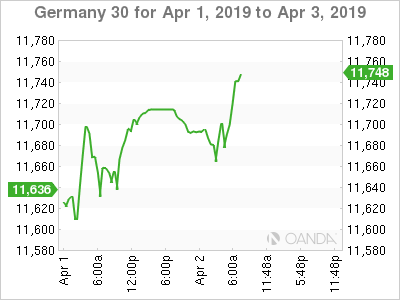

The DAX has posted more gains on Tuesday, after starting the week with excellent gains. Currently, the DAX is at 11,733, up 0.45% on the day. Currently, the DAX is trading at 11.652, up 1.1% on the day. It’s a quiet day on the release front, with just one event. Eurozone PPI dipped to 0.1%, shy of the estimate of 0.2%. On Wednesday, Germany and the eurozone release services PMIs, and the eurozone will also post retail sales.

The DAX soared on Monday, posting its best daily gains since mid-February. The index jumped 1.35%, despite a weak German manufacturing PMI. French and German markets ignored the soft German data, focusing on Chinese data instead. The Chinese Caixin Manufacturing PMI didn’t sparkle, but improved to 50.8 and easily beat the estimate of 50.1 points. Investors cheered as the indicator climbed to an 8-month high, after posting three successive releases indicating contraction. The Chinese economy has been hit hard by the trade war with the U.S., and a piece of good news sparked strong gains on the equity markets.

Investors have become used to lukewarm data out of the eurozone and Germany, but are also discovering that the mighty U.S. economy is showing signs of slowing down. Retail sales, the primary gauge of consumer spending, looked dismal in March. The indicator declined by 0.2%, shy of the estimate of +0.3%. Core retail sales declined by 0.4%, a sharp drop from the 0.9% gain a month earlier. Both indicators posted a second decline in three months, which is bound to raise concerns about the strength of the economy. Growth for the first quarter could be as low as 0.8% annualized, compared to 2.2% in the third quarter.

Economic Calendar

Tuesday (April 2)

- 5:00 Eurozone PPI. Estimate 0.2%. Actual 0.1%

Wednesday (April 3)

-

3:55 German Final Services PMI. Estimate 54.9

-

4:00 Eurozone Final Services PMI. Estimate 52.7

-

5:00 Eurozone Retail Sales. Estimate 0.2%

Author

Kenny Fisher

MarketPulse

A highly experienced financial market analyst with a focus on fundamental analysis, Kenneth Fisher’s daily commentary covers a broad range of markets including forex, equities and commodities.